Why SME Marketplace KYB Stalls — and What Actually Fixes It

Most SME marketplace KYB queues don't grow because the rules are hard. They grow because one business arrives as three partial records the stack can't join.

B2B and B2C marketplaces that onboard SMEs as sellers or suppliers run into the same operational problem: a meaningful share of applications sits in review longer than it should. The easy businesses pass. The clearly problematic ones fail. The rest wait.

VOVE ID helps marketplace compliance teams resolve that middle bucket faster — by joining entity, control, and operating records into one decision-ready file instead of leaving reviewers to reconcile them manually.

This guide covers the structural reasons SME KYB stalls, what EU law actually requires when onboarding legal entities, and how to build a workflow that handles ordinary real-world messiness without routing everything into manual review. For the underlying KYB framework and CDD requirements, see our KYB Requirements Explained 2026: Complete Fintech Compliance Framework Used by Regulated Institutions.

Why a large share of SME onboardings stall

The "stalled middle" is not a legal threshold. It is an operating symptom.

Many SME marketplace teams see the same pattern: easy businesses pass quickly, clearly bad businesses fail quickly, and a substantial middle portion gets stuck because the records don't reconcile cleanly. That middle bucket is where revenue waits.

The marketplace may already have the company name, the registration number, the director's ID, a bank account, and a website — and still not have a decision-ready file.

The reason is that KYB under the EU AML framework is not just "find the company in a register."

Article 13 of Directive (EU) 2015/849 says customer due diligence includes identifying the customer and verifying identity from reliable and independent sources, identifying the beneficial owner and taking reasonable measures to verify that identity, understanding the purpose and intended nature of the relationship, and conducting ongoing monitoring. That is already more than one record.

Article 30 adds another important constraint for marketplaces onboarding legal entities. Member States require corporate entities to hold adequate, accurate, and current beneficial-ownership information, and central registers are meant to provide timely access. But Article 30(8) also specifies that obliged entities should not rely exclusively on the central register to fulfill CDD.

That one provision explains a lot of marketplace friction. The register matters. It is not enough on its own.

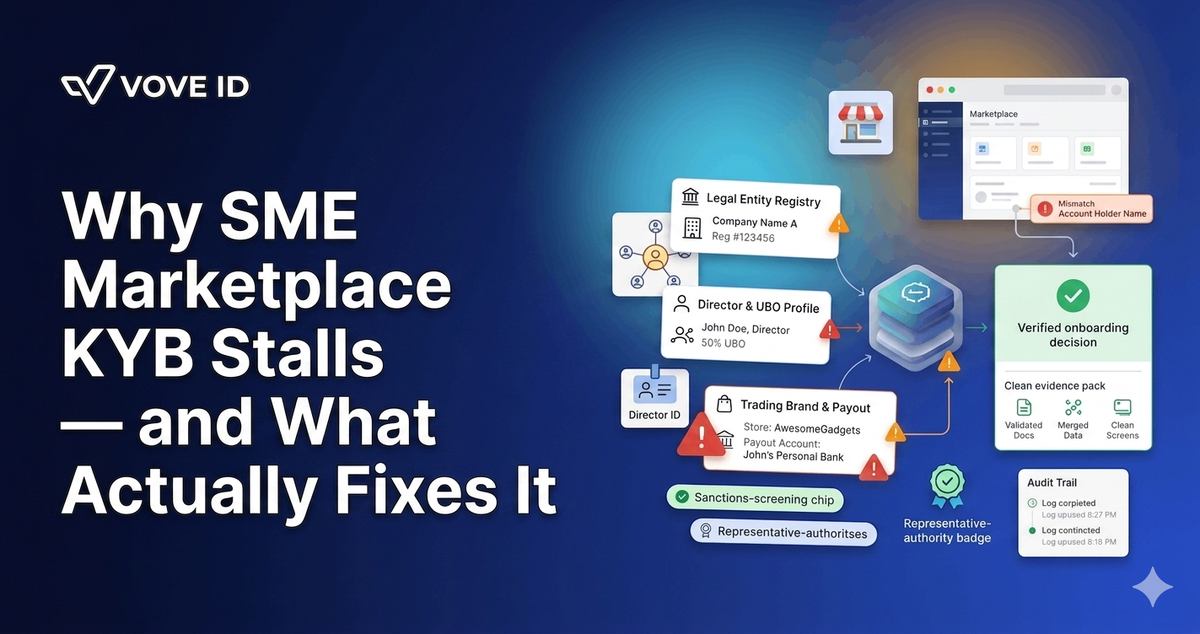

The three records inside one SME

The fastest way to understand stalled SME onboarding is to stop treating one SME as one thing. It usually arrives as three things at once.

1. The legal-entity record

This is the company as the registry sees it: legal name, registration number, status, directors or legal representatives, registered address, and sometimes shareholders or filing history.

This layer answers a real question: does this company exist as a legal person in the way the applicant claims? It is foundational, but it is not the whole picture.

2. The control record

This is the human layer behind the company: directors, authorised signatories, founders, beneficial owners, anyone acting on behalf of the entity.

This is where many marketplace stacks slow down. The named director may not be the day-to-day operator. The beneficial owner may sit above the immediate entity. The representative uploading documents may be legitimate but not visible in the first source the reviewer checked. At that point the marketplace has a CDD problem, not a user-experience problem.

3. The operating-business record

This is the business as it behaves commercially: the brand name customers recognise, the bank account receiving payouts, the website or store domain, the warehouse or operating address, the product category and transaction pattern.

This record often diverges from the legal record without indicating fraud. A perfectly legitimate SME may trade under a brand that does not match the corporate name. A director may temporarily receive funds in a different operational setup. A holding company may own the entity while another name appears on storefronts and invoices.

The issue is not that those patterns are automatically suspicious. The issue is that the stack has to be able to explain them.

When the bank account, the registry, and the director disagree

Consider a representative EU B2B marketplace scenario. The registry record looks valid — the company is active and a director is listed. But the payout account name belongs to the director personally, not the company. The website uses a trading name that does not match the legal entity. The person who completed onboarding is not the listed director; they say they are the operations lead with authority to act.

None of this proves misconduct. None of it is ignorable either.

The onboarding stalls for predictable reasons: the reviewer cannot confirm whether the payout setup is acceptable, the representative's authority is unclear, the operating brand needs to be connected to the legal entity, and the control layer may still need a beneficial-ownership explanation.

A marketplace that handles this case badly usually does one of four things:

- asks for additional documents without explaining what mismatch triggered the request

- routes the case into manual review with no structured next step

- clears the case on incomplete logic because commercial pressure is high

- rejects a legitimate SME because the stack cannot reconcile ordinary real-world complexity

All four outcomes are expensive. The first two cost conversion and reviewer time. The third costs compliance quality. The fourth costs revenue and marketplace supply.

Why SME marketplace KYB is structurally harder than ordinary business onboarding

A marketplace is not just opening accounts. It is creating a repeatable seller or supplier funnel where speed matters commercially. That changes the KYB standard in practice.

The team does not need only a correct decision. It needs a correct decision at scale, with an explanation that survives later review.

That is harder because marketplaces routinely onboard SMEs with incomplete back-office processes, mixed personal and business payment habits, trading names that obscure the legal entity, ownership structures that are simple in reality but messy in documents, and cross-border suppliers whose registry, payout, and operating footprints sit in different countries.

The European register landscape adds another layer. Business register services vary from one Member State to another, which means one entity-resolution workflow will encounter different field depth, different retrieval paths, and different documentation expectations across the EU.

So when marketplace teams say "our SME onboarding stalled," the more precise translation is usually: the stack found the company, but it could not turn the company into a defensible commercial relationship fast enough.

How to join the three records into one onboarding decision

The answer is not more documents by default. It is better record resolution.

For SME marketplaces, VOVE ID helps by turning the legal, control, and operating layers into one joined case file — so the reviewer sees the full picture rather than three separate records that may or may not agree.

That means anchoring the legal entity first before collecting evidence around it, attaching directors, signatories, and beneficial owners to the entity record with clear source visibility, tying the bank account, storefront name, website, and operating behaviour back to the entity so the reviewer can see whether a mismatch is explainable or genuinely anomalous, routing only cases with real unresolved disagreement into human review, and preserving a single audit trail that explains why the case passed, failed, or escalated.

That last part matters as much as the decision itself. The reason the case resolved stays in the file — for regulators, banking partners, internal QA, and future monitoring reviews.

For a full breakdown of AML/CFT obligations that apply to marketplace onboarding workflows, including CDD, ongoing monitoring, and record-keeping requirements, see our AML Requirements Explained 2026: Compliance Operating System for Regulated Financial Institutions.

Practical checklist for SME marketplace KYB

Entity

Confirm the legal entity before collecting miscellaneous evidence around it. Keep legal-entity verification separate from operating-brand interpretation.

Control layer

Verify who is authorised to act and who ultimately controls the entity. Director identity and beneficial ownership are not the same question — treat them separately.

Operating record

Tie the payout account, storefront, website, and trading name back to the legal entity. Escalate only when the disagreement cannot be explained with structured evidence.

Audit trail

Document the reason the case resolved, not just the outcome. A passed file with no recorded rationale is a liability at the next regulatory review.

The real bottleneck is the record model

Most SME marketplaces do not have a small-business problem. They have a record-model problem.

Onboarding was built around the idea that one business produces one clean answer. In practice, one business often produces three partial answers that only become useful when the system joins them correctly.

The queue is not a sign that the market is impossible. It is a sign that the KYB stack is reading SMEs as simpler than they are.

FAQ

Why do SME marketplace onboardings stall so often during KYB?

Because one SME rarely arrives as one clean record. The marketplace has to reconcile the legal entity, the people who control it, and the operating business details — payout account, trading name, website — before the file is decision-ready. When those three layers disagree, the queue grows.

Is a company registry lookup enough for marketplace KYB?

No. A registry lookup confirms the entity exists, but it does not answer who controls the business, who is authorised to act, how the operating brand maps to the legal entity, or whether the payout setup is appropriate. Article 30(8) of Directive (EU) 2015/849 says exactly this.

What are the most common mismatches that slow SME onboarding?

Payout accounts that don't match the legal entity name, trading brands that differ from the corporate name, representatives who aren't the listed director, and beneficial-ownership questions that need an explanation are the four most common.

What should a good SME marketplace KYB workflow do?

Anchor the legal entity first, map directors and beneficial owners clearly with source attribution, reconcile the operating brand and payout setup against the entity, route only genuine disagreements into human review, and record why each case resolved the way it did.

SME marketplace onboarding queues grow when the stack treats three records as one problem it can't solve. VOVE ID helps compliance teams join those records into one decision — so the middle third clears instead of waiting.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.