AML

The New EU AML Authority (AMLA): What Startups Should Be Doing Now

AMLA won't supervise most startups directly in 2026. Their partners and regulators already expect its standard.

AML

AMLA won't supervise most startups directly in 2026. Their partners and regulators already expect its standard.

KYC

AMLR's KYB impact gets most of the attention. The retail customer file has its own gap to close.

crypto

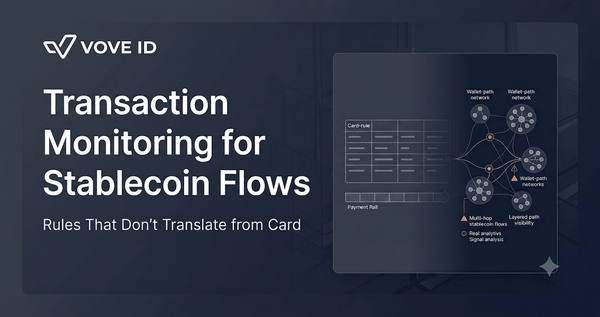

Card rules see the transaction. Stablecoin risk lives one layer deeper, in the wallet path behind it.

AML

A default looks like a credit event. Sometimes it's the first visible trace of a laundering or fraud network.

AML

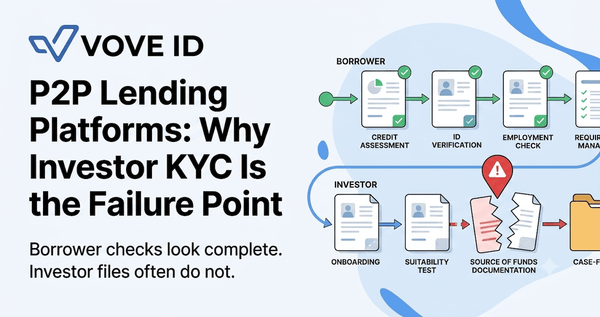

Why source-of-funds evidence and case reconstruction for retail investors, not borrower onboarding, is where P2P lending platforms usually fail an audit.

KYC

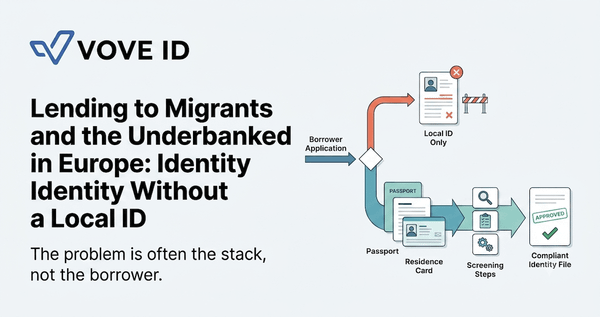

Why migrants and underbanked Europeans fail onboarding before risk assessment even starts, and how lenders widen identity acceptance without weakening KYC.

KYC

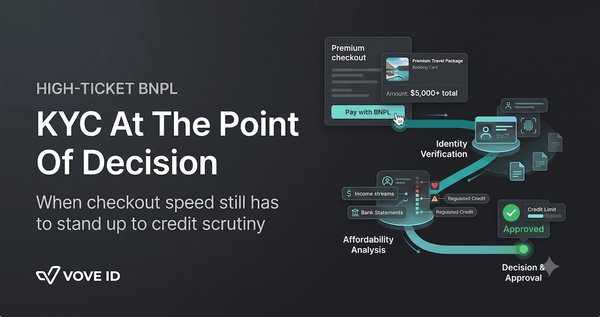

Why a fast BNPL approval on a large basket isn't the same as a defensible one, and what CCD2 requires once the ticket size shifts the risk.

KYB

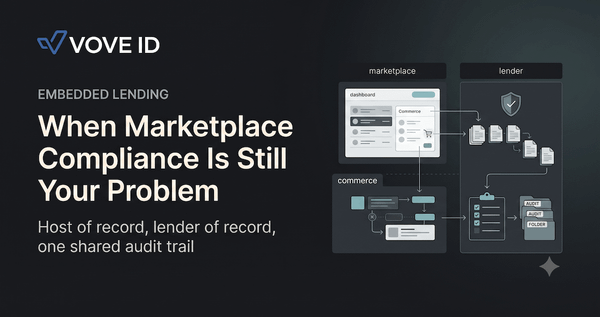

Why the host-of-record isn't the same as the compliance owner, and what marketplaces running embedded credit need to prove when the lender gets audited.

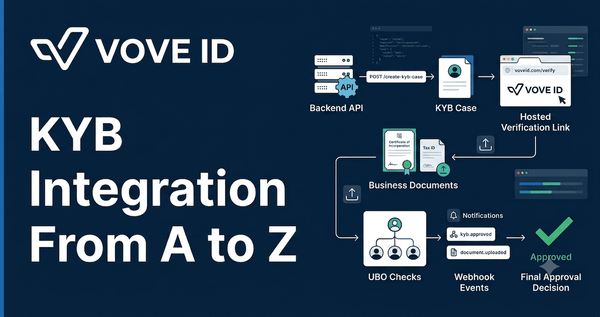

VOVE ID helps teams verify business customers without building an entire KYB operations workflow from scratch. The integration is simple at the API level: configure your credentials and KYB flow, create a KYB case from your backend, send the business a secure verification link, listen for webhooks, and retrieve the

AML

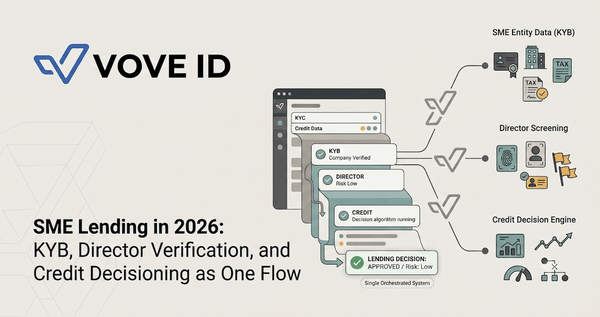

Why treating entity checks, director verification, and credit approval as a relay creates gaps that surface exactly when a regulator asks for evidence.

KYC

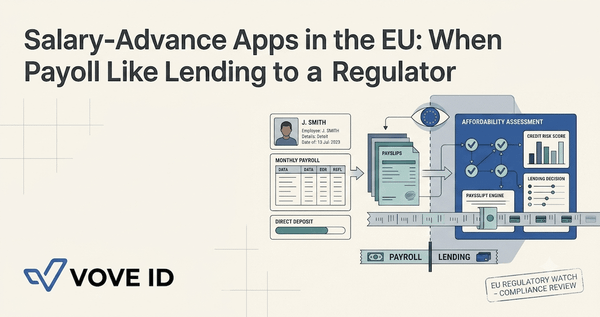

Why earned-wage access products can't rely on the payroll label alone, and what affordability, disclosure, and audit trails CCD2 actually requires.

AML

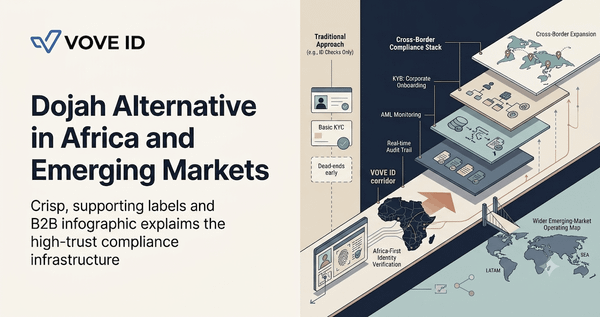

A practical comparison for teams asking whether Dojah still fits once onboarding grows into KYB, monitoring, and regulator-facing evidence.