The New EU AML Authority (AMLA): What Startups Should Be Doing Now

AMLA won't supervise most startups directly in 2026. Their partners and regulators already expect its standard.

VOVE ID helps fintech startups read AMLA in markets where the home NCA still leads and AMLA quietly sets the tone. On paper AMLA supervises specific institutions. In practice it shapes everything around them.

The short answer

Startups should not read AMLA as "relevant later if we get bigger." They should read it as a signal that governance, record quality, and supervisory responsiveness are being judged to a higher standard now. Even firms outside direct AMLA supervision can be pulled into AMLA-driven expectations through partner reviews, home regulators, and thematic requests.

Why AMLA matters before it supervises you directly

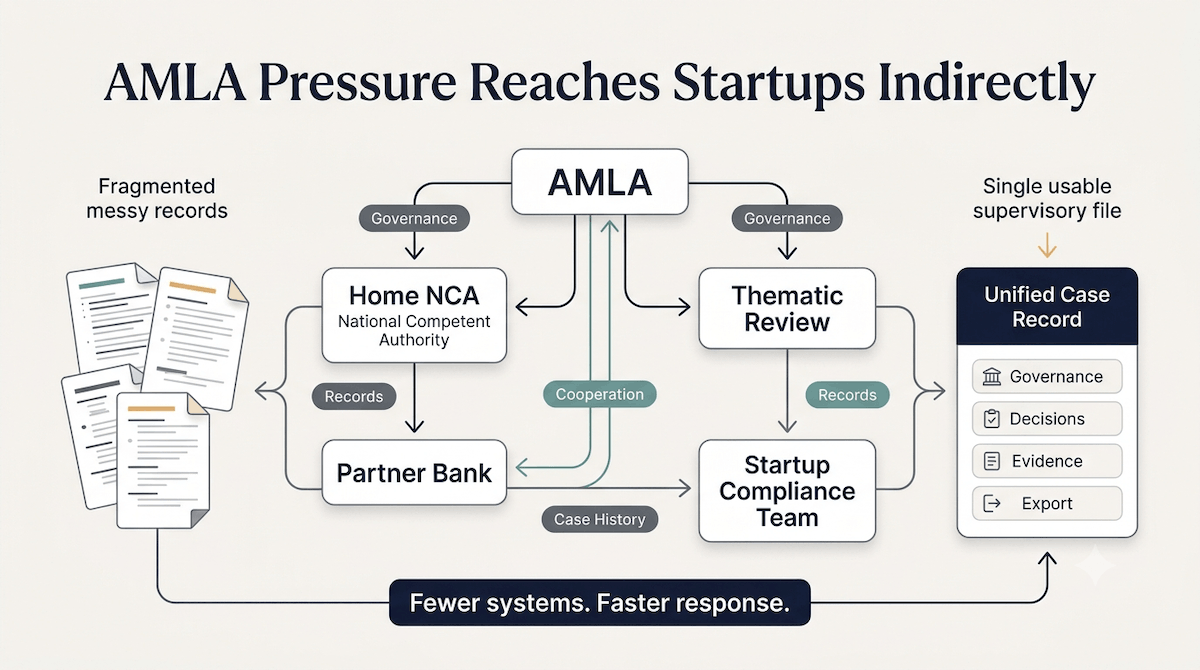

Many fintech teams assume AMLA is someone else's regulator. That is too narrow. Direct supervision may land on a defined set of institutions, but indirect pressure lands much wider. Once AMLA sets a stronger tone for cooperation, documentation, and cross-border AML execution, smaller firms feel it through every stakeholder asking harder questions.

A startup does not need to be on AMLA's direct list to face AMLA-shaped scrutiny. It only needs a partner bank, an investor, a home competent authority, or a cross-border operating model that now requires cleaner answers.

AMLA's direct and indirect supervision

Direct supervision gets the headlines. Indirect supervision changes day-to-day behavior. That is where early-stage firms should focus.

- Direct supervision tells the market what "good" increasingly looks like.

- Home regulators absorb that standard into reviews and thematic exercises.

- Banking and infrastructure partners mirror the same expectation in diligence.

- Cross-border startups lose room to say a fragmented internal process is normal for their size.

The result is that governance maturity becomes visible earlier than many founders expect.

For a full breakdown of AML program obligations, see our AML Requirements Explained 2026.

What AMLA-grade governance looks like for a 30-person fintech

AMLA-grade governance does not mean building a large compliance department overnight. It means being able to produce a coherent record quickly.

For a 30-person fintech, that usually comes down to a few operational basics:

- one place to see the full case history

- clear ownership of reviews and escalations

- consistent evidence across onboarding, screening, and monitoring

- fast exportable records when a supervisor or partner asks for them

This is where many startups are weaker than they realize. The work may be getting done, but the record sits across Slack threads, spreadsheets, vendor dashboards, and individual inboxes.

A realistic AMLA failure

Picture a Latvian fintech asked by its home regulator to respond to an AMLA-driven thematic review. The request is not theoretical. The team has three days to show governance, sample alert handling, and supporting records. Compliance owns part of the answer. Operations owns another. The monitoring vendor has the rest.

No single artifact is catastrophic. The failure is fragmentation. By the time the team assembles the package, it has spent most of its response window reconciling systems rather than proving control.

That is what indirect AMLA pressure looks like in practice.

How VOVE ID delivers AMLA-grade governance at startup size

VOVE ID helps smaller firms act organized before they have large internal teams. Instead of treating governance as a separate reporting exercise, the platform turns everyday compliance activity into a usable supervisory record.

That means:

- unified case records across workflows

- time-stamped decisions and reviewer attribution

- alert and escalation history tied to the customer or business record

- exportable evidence when a regulator, partner, or auditor asks for it

The value is speed under pressure. When a review arrives, the team does not need to reconstruct what happened. The record is already there.

AMLA readiness checklist

- Governance responsibilities are clearly assigned

- Records are unified enough to answer cross-functional reviews quickly

- Cooperation requests can be answered with one defensible case history

Common questions

If AMLA does not directly supervise us, can we wait?

That is risky. Indirect expectations often arrive before direct supervisory relevance, especially through local regulators and counterparties.

Does AMLA mainly affect large payment institutions?

The direct scope is narrower than the practical impact. Smaller firms still feel the standard through diligence and review demands.

What should a startup fix first?

Fix record fragmentation first. Teams usually know their policy story before they can prove their operational story.

Conclusion

AMLA changes the bar for credibility, not just for the firms it directly supervises, but for the ecosystem around them. Startups that prepare now will move faster when scrutiny comes, because governance will already exist as evidence instead of as a last-minute scramble.

Want to see how VOVE ID delivers AMLA-grade governance at startup size? A unified case record is usually a smaller lift than teams expect once the pieces are already being captured somewhere.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.