Defaulted Loans and the AML Trail: What Collections Teams Often Miss

A default looks like a credit event. Sometimes it's the first visible trace of a laundering or fraud network.

VOVE ID helps lenders read default as an AML signal in markets where the same borrower defaults across three lenders. On paper default is a credit fact. In practice it is sometimes a fraud pattern.

The short answer

Collections teams usually inherit the loan only after origination has failed, but that does not make the file irrelevant to AML. A default can expose mismatched income claims, circular repayment behavior, mule-account usage, repeated device patterns, and linked identities across lenders. If collections sits outside the AML loop, the lender learns too late that a "bad borrower" was actually part of a larger laundering or first-party fraud pattern.

Why default belongs in the AML trail

Most lending stacks split the borrower lifecycle into neat departments: onboarding owns KYC, underwriting owns risk, and collections owns recovery. Regulators do not read the file that way. They care whether the institution can explain what it knew, when it knew it, and what signals were ignored once the customer relationship turned abnormal.

Default is one of those abnormal moments. A missed payment by itself is not suspicious. A borrower who defaults shortly after disbursement, routes funds through newly opened accounts, and appears in multiple internal files is a different matter. Once that pattern emerges, collections is no longer dealing with a pure credit event. It is handling evidence that should feed the AML and fraud narrative of the customer.

For embedded lenders and digital lenders in Europe, this matters because default data often sits in an operations tool that compliance never sees. The lender writes off the exposure, but no one asks whether the repayment behavior contradicts the original source-of-funds story, the declared employment data, or the wider monitoring picture.

For a full breakdown of transaction monitoring obligations, see our AML Requirements Explained 2026.

What collections teams can actually see that AML often cannot

Collections agents usually see the most operationally honest version of the borrower. They hear the reasons for missed payments. They see which channels still work, which bank account the borrower wants to use now, and whether the story keeps changing. That is useful AML context when it is captured in a structured way instead of living only in notes and call outcomes.

The strongest signals tend to be simple:

- A borrower who defaults across related products or entities in a short period

- Repayment attempts coming from third-party accounts with no clear relationship to the borrower

- Contact details, devices, or IP patterns that overlap with earlier write-offs

- Income or business explanations that collapse under collections outreach

- Sudden requests to change payout or repayment rails after disbursement

A realistic collections failure: when serial default ladders up to laundering

Imagine a Czech lender that writes off a 1,500 EUR consumer loan after a fast default. The case is treated as an ordinary recovery matter. A month later, a second borrower defaults with a similar pattern: same employer category, same repayment bank, same device family, same cash-out timing. Then a third file appears through a sister brand. Each file is reviewed in isolation, so each one looks like thin-margin bad debt.

Only later does the pattern become visible. The initial income evidence was weak in all three cases. The funds were disbursed quickly and fragmented across accounts. Repayment attempts came from third parties. The borrowers had just enough legitimate data to pass onboarding, but the post-disbursement behavior pointed to coordinated abuse.

That is the failure collections teams often inherit. The credit stack asks, "Can we recover?" The AML question should be, "What network does this file now belong to?" If the lender cannot reconstruct that trail, it loses both money and explainability.

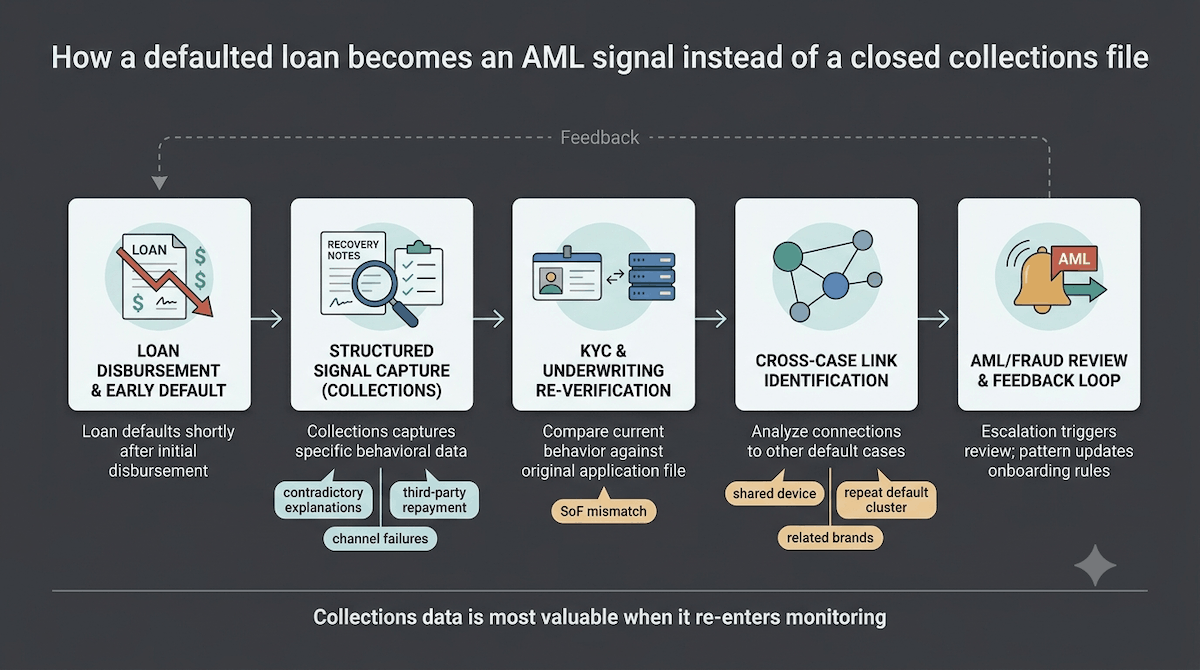

How VOVE ID connects collections to monitoring

VOVE ID treats default as an event that should enrich the customer risk picture, not close the file. The useful operating model has four parts.

1. Default events become structured signals

A default should not enter the system as a generic status change only. It should carry timing, amount, repayment behavior, linked account details, contact-channel outcomes, and any contradiction between the original onboarding story and later borrower behavior.

2. The signal is matched against the existing customer file

Once structured, the default event can be compared with KYC data, source-of-funds logic, document confidence, device intelligence, and previous risk decisions. This is where collections information becomes a compliance asset instead of a dead-end note.

3. Cross-case patterning is treated as part of AML monitoring

The real value comes when defaults are not assessed one by one. If multiple loans connect through shared repayment accounts, reused devices, employer patterns, or synthetic identity markers, the lender should escalate the cluster rather than chasing each balance separately.

4. Monitoring feeds back into onboarding and underwriting

If collections discovers that a certain profile consistently defaults in a suspicious way, that pattern should tune onboarding reviews, risk controls, and future monitoring rules. Otherwise the organization keeps relearning the same lesson at full cost.

Collections-to-AML checklist

- Default: Capture why the account defaulted and how quickly the story changed after disbursement.

- Pattern: Check for links across devices, repayment accounts, contact data, and sister brands.

- Escalation: Route suspicious default clusters into AML or fraud review before writing them off as ordinary bad debt.

Q&A

Is every default an AML issue?

No. Most defaults are still ordinary credit outcomes. The point is that default is a moment worth evaluating for AML relevance, not a signal to ignore by default.

What is the most common operational mistake?

Keeping collections notes outside the compliance data model. Once the useful context lives only in call notes or spreadsheets, pattern detection becomes almost impossible.

Do smaller lenders need a complex intelligence team for this?

No. They need a structured way to capture post-disbursement signals and push them into monitoring, case review, and rule tuning.

Conclusion

Collections teams often see the clearest version of risk, but many lenders use that view only to pursue recovery. The better approach is to treat default as a possible AML signal, connect it to the borrower file, and look for repeatable patterns across the portfolio. That is how lenders stop writing off the same suspicious behavior as routine bad debt.

Want to see how VOVE ID reads default as the AML signal it can be? The pattern is usually visible across your own case files before it shows up in an audit.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.