Lending to Migrants and the Underbanked in Europe: Identity Without a Local ID

Why migrants and underbanked Europeans fail onboarding before risk assessment even starts, and how lenders widen identity acceptance without weakening KYC.

VOVE ID helps lenders serve migrants and underbanked borrowers across Europe by widening the identity stack beyond one national-ID assumption without lowering the quality of KYC or AML controls.

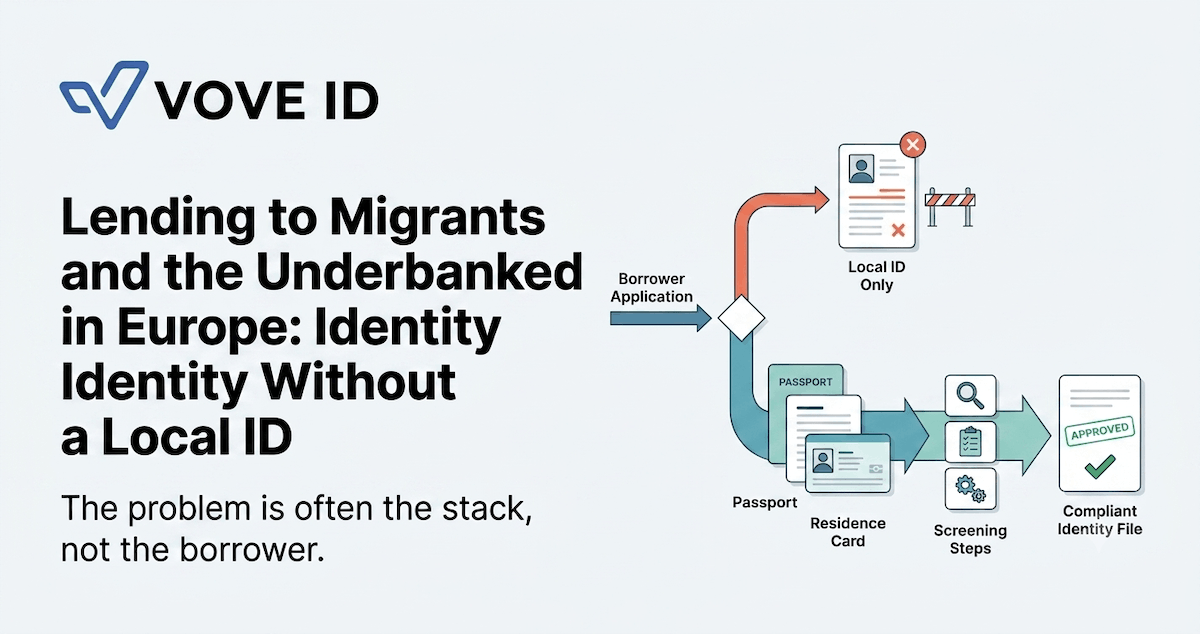

Direct answer: Many underbanked borrowers are rejected because a lender's onboarding stack only recognizes one local identity path. The compliance issue is usually not that the borrower is unknowable, but that the system cannot read legitimate documents and residency evidence already available.

Financial inclusion is often discussed as if it were mainly a credit-policy decision. In many lending businesses, the first exclusion actually happens earlier. The borrower reaches the onboarding flow, has stable residency, income, and a valid documentary trail, but the stack cannot interpret the identity evidence because it was built around a narrow local default.

That is why migrants and other underbanked groups are so often labeled difficult to verify. The person is not necessarily high risk. The workflow is simply too rigid.

Who Europe's Underbanked Actually Are

The underbanked in Europe are not one borrower profile. They include recent migrants, long-term residents without the most common local credential, cross-border workers, gig-economy earners with irregular documentation patterns, and people whose official identity trail spans more than one country.

Many of them have strong signals:

- valid passports

- residence cards or permits

- employer records

- tax identifiers

- income history

- bank account activity

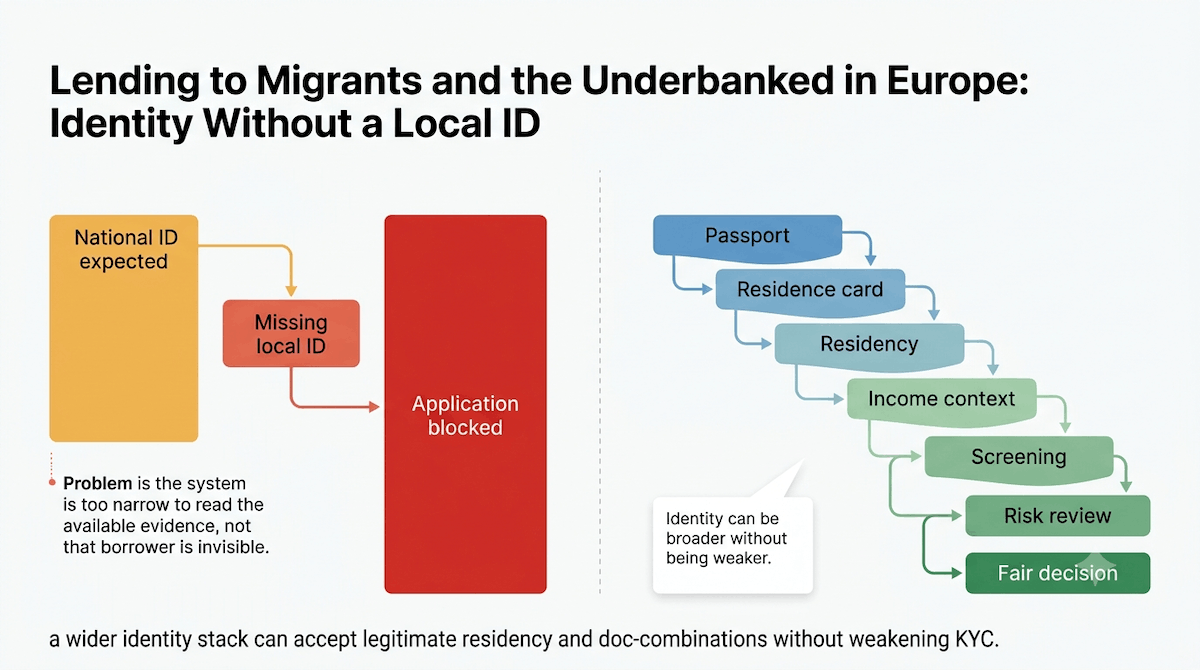

What they often lack is the exact identifier the lending stack expects at the first decision point. When that identifier becomes mandatory in practice, exclusion stops being a risk-based policy choice and becomes an accidental product design choice.

For lenders, that distinction matters. A policy can be defended. An arbitrary technical bottleneck is harder to justify.

For a full breakdown of identity verification requirements, see our KYC Requirements Explained 2026.

Identity Options Beyond The National ID Card

The most common onboarding failure is treating one national credential as if it were the only trustworthy way to establish identity. In reality, a robust lending stack can combine multiple document and data paths while still remaining compliant.

Depending on market and risk profile, that may include:

- passport plus residence permit

- national ID plus address confirmation

- residence card plus payroll evidence

- cross-checks against local or regional databases

- sanctions, PEP, and fraud screening attached to the same case

The goal is not to weaken the file by accepting anything. The goal is to read legitimate combinations of identity and residency evidence that already exist for real borrowers.

When the stack cannot do that, operations teams start improvising. Manual overrides increase. Support queues grow. Approval logic becomes inconsistent. Borrowers who should be reviewable are rejected at the first gate because the product cannot parse their profile.

A Realistic Financial Inclusion Failure: When A Long-Term Resident Is Rejected Over A Missing PESEL

Take a Polish lender serving salary earners and consumer borrowers. A Ukrainian long-term resident applies with a residence card, verifiable employment, and a strong salary profile. The application should be reviewable on its merits.

Instead, the lender's workflow expects a PESEL-centered path at the earliest identity step. Because that number is missing from the expected format, the borrower is treated as incomplete before risk assessment even begins.

This is not a regulatory necessity. It is a stack assumption.

The lender now faces three bad options:

- reject the borrower automatically

- create a manual exception path that does not scale

- override the issue without building a proper evidence trail

None of those is attractive. The first blocks addressable demand. The second slows operations. The third creates audit weakness.

The better approach is to model identity in layers:

- Core identity proof

- Right-to-reside evidence

- Income or activity context

- Sanctions and risk screening

- Decision logic tied to the actual file

Once the workflow is structured that way, the absence of one local ID is no longer interpreted as absence of identity itself.

How VOVE ID Broadens Identity Without Weakening The File

VOVE ID helps lenders widen acceptance of legitimate identity combinations while keeping the case trail structured, reviewable, and risk-based. The aim is not softer compliance. It is better parsing of real European borrower profiles.

That means the lender can support flows such as:

- passport plus residence permit for migrants and long-term residents

- multiple document types matched in one onboarding case

- local and regional screening layered onto the same workflow

- exception handling that still records rationale and evidence

- consistent treatment of identity, residency, and risk in one file

This matters commercially because more borrowers reach a fair decision. It matters operationally because support teams do not need to rebuild the case manually. And it matters from a compliance standpoint because the final file explains why the borrower was accepted, declined, or escalated.

Underbanked lending only becomes dangerous when inclusion is implemented as guesswork. If the workflow is built to recognize valid documents, residency proof, and risk context together, inclusion can be systematic rather than improvised.

Operational Checklist

- Identity: Accept more than one legitimate document path when the borrower can be reliably identified.

- Residency: Capture right-to-reside evidence and tie it directly to the case instead of handling it off-platform.

- Risk: Run sanctions, fraud, and review logic on the expanded identity set, not on a narrow single-ID assumption.

Q&A

Does accepting borrowers without a local national ID weaken KYC?

No. KYC weakens when teams accept unclear evidence. Expanding to valid multi-document identity paths can strengthen KYC because it creates a fuller and more realistic borrower file.

Why do underbanked borrowers get rejected even when they have stable income?

Because many onboarding systems fail before affordability or risk checks begin. The stack cannot interpret the identity and residency documents the borrower has, so the application is blocked too early.

Is this mainly a policy problem or a product problem?

Often it is a product and workflow problem first. Teams may already be willing to serve these borrowers, but their onboarding stack cannot support compliant identity combinations at scale.

Conclusion

Lending to migrants and underbanked Europeans does not require weaker compliance. It requires a better identity model. When lenders stop treating one local credential as the only acceptable entry point, they can expand access while preserving clear KYC, residency, and risk controls.

Want to see how VOVE ID helps lenders serve underbanked Europeans without weakening KYC?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.