P2P Lending Platforms: Why Investor KYC Is the Failure Point

Why source-of-funds evidence and case reconstruction for retail investors, not borrower onboarding, is where P2P lending platforms usually fail an audit.

VOVE ID helps P2P lending platforms run investor-side KYC with the same discipline they already apply to borrowers, especially when EU scrutiny treats retail lenders as protected clients rather than passive capital.

Direct answer: P2P platforms usually think borrower onboarding is the regulated surface. In practice, investor KYC, source-of-funds evidence, and audit reconstruction are where regulators find the first serious gap.

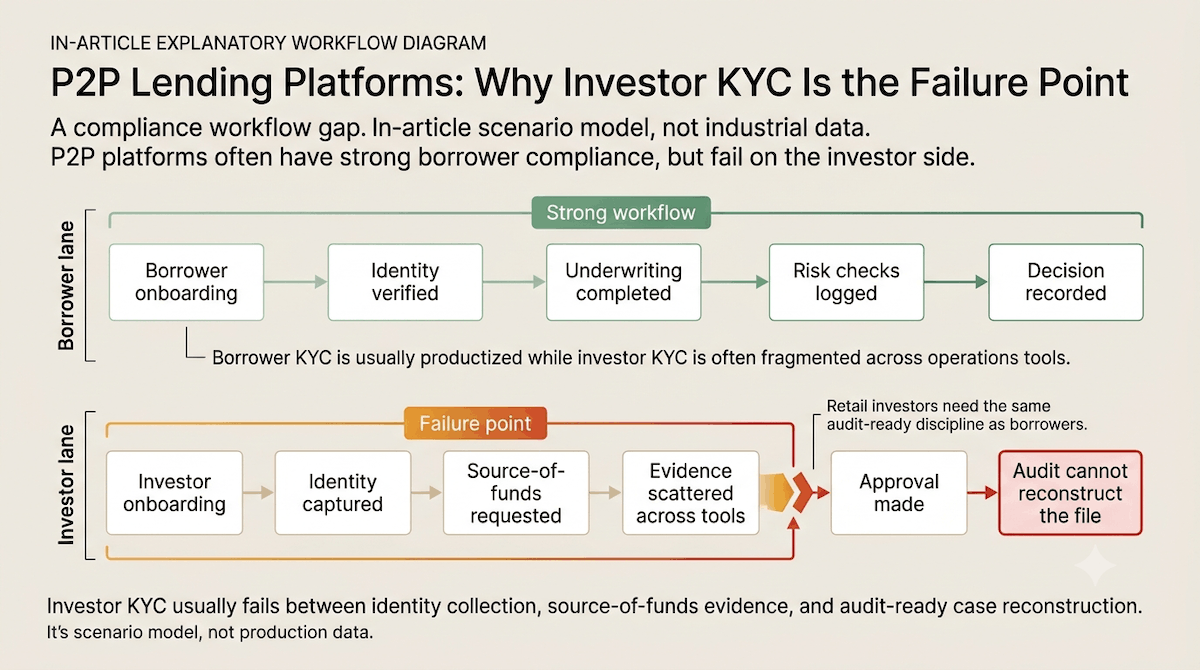

P2P lending teams rarely ignore compliance. They build controls around borrower onboarding, underwriting, collections, and fraud. That is where the visible operational risk sits, so that is where most of the process maturity goes.

The problem is that many platforms still treat the investor side as a lighter workflow. The investor is already bringing capital, often already known to the platform, and sometimes classified internally as sophisticated enough to need less friction. That assumption breaks down quickly in an audit. Once retail investors are part of the model, the platform has to prove who funded the account, what source-of-funds evidence was collected, how risk escalations were handled, and whether the file can be reconstructed months later.

P2P Investor KYC Under The New EU Regime

Across the EU, investor protection expectations have moved in one direction: more traceability, more suitability discipline, and less tolerance for informal onboarding logic. A P2P platform may think of itself as matching lenders and borrowers, but a regulator will still examine whether retail investors were onboarded, documented, and reviewed with appropriate rigor.

That changes the operational question. The platform is no longer just asking whether a borrower can be identified before receiving funds. It also has to ask whether each investor can be treated as a fully documented retail client whose identity, residency, sanctions exposure, and source of funds can all be defended later.

For many teams, this is the first structural mismatch:

- Borrower KYC is productized and measured.

- Investor KYC is partially manual and inconsistently documented.

- Source-of-funds requests depend on the reviewer rather than a policy path.

- Audit reconstruction depends on scattered notes instead of a complete file.

That is why investor KYC becomes the failure point. The issue is not that the rules are unknowable. The issue is that the operating model was built around the wrong primary risk surface.

For a full breakdown of identity verification requirements, see our KYC Requirements Explained 2026.

Source Of Funds For Retail Lenders

Source-of-funds is where investor onboarding stops being a simple identity task. A passport, residence permit, or selfie may establish who the investor is. It does not explain where investable funds came from, whether the evidence was proportionate to the risk, or whether the platform can prove that it asked the right follow-up questions.

For retail lenders, the file usually needs to show more than basic identity. Depending on ticket size, geography, risk triggers, and business model, the platform may need to capture:

- occupation or business activity

- salary or income evidence

- bank statement context

- explanation for transferred funds

- links between funding account, identity, and declared residence

- escalation notes when the initial explanation is weak

The operational trap is inconsistency. One reviewer accepts a payroll statement. Another asks for six months of bank history. A third reviewer records the decision only in internal chat. The platform may feel compliant in the moment, but the file does not hold together when someone asks for a clean reconstruction.

For a full breakdown of sanctions screening and PEP obligations, see our AML Requirements Explained 2026.

A Realistic P2P Failure: When An Investor's SoF Cannot Be Reconstructed

Consider a Czech P2P platform preparing for an audit. Borrower files look healthy. The underwriting trail is documented, transaction logic is visible, and delinquency procedures are easy to explain.

The investor sample tells a different story.

The audit review finds that 22% of investors have no complete source-of-funds trail. The platform did collect some evidence in many cases, but the information sits in different places:

- one PDF in a CRM attachment

- a funding explanation pasted into reviewer notes

- a sanctions result stored in another tool

- an approval decision without the rationale behind it

The platform's internal defense is familiar: these were not high-risk business customers, and many of them were returning investors. That argument usually fails because the regulator is testing whether the platform can prove a coherent onboarding standard for retail participants, not whether the operations team had good intentions.

This is also where investor classification becomes dangerous. If the platform informally treated parts of its lender base as business clients without collecting the evidence that supports that treatment, it has created a documentation gap and a policy gap at the same time.

The core issue is not missing one more document. It is that the platform cannot reconstruct the decision path:

- Who was the investor?

- What funds were used?

- What evidence supported that explanation?

- What risk signals appeared?

- Who approved the file and under which rule?

If those answers live in separate systems, the platform will struggle to defend the file even when the underlying customer may be legitimate.

How VOVE ID Treats P2P Investors As The Retail Clients They Are

VOVE ID helps teams bring investor onboarding into the same controlled workflow they already expect on the borrower side. That matters because investor KYC cannot depend on memory, reviewer style, or exception handling in a spreadsheet.

In practice, that means:

- identity capture that supports cross-border retail onboarding

- sanctions and PEP screening linked to the same case record

- source-of-funds evidence gathered as part of the workflow, not as an afterthought

- configurable escalation paths when declared activity and funding pattern do not align

- a reconstructable case file that explains how the approval happened

For P2P platforms, the gain is operational before it is cosmetic. The team no longer has to argue that investor onboarding was "handled somewhere else." The file itself shows the standard. That is what reduces audit stress.

It also makes policy clearer internally. Borrowers and investors do not need identical workflows, but they do need equally defensible ones. Once that principle is accepted, the platform can stop over-investing in one half of the compliance problem while under-documenting the other.

Operational Checklist

- Investor: Capture verified identity, residency, sanctions checks, and a source-of-funds trail proportionate to risk.

- Borrower: Keep underwriting, onboarding, and monitoring logic documented separately so investor evidence is not mixed into borrower files.

- Audit: Ensure every investor approval can be reconstructed from one consistent case trail with escalation rationale included.

Q&A

Why is investor KYC harder than borrower KYC on some P2P platforms?

Because borrower onboarding is usually designed as a product workflow, while investor onboarding is often treated as a lighter operations process. Audits expose that difference quickly.

Is source-of-funds always required for every investor?

The level of evidence should be risk-based, but platforms still need a consistent policy for when source-of-funds checks apply, what proof is acceptable, and how decisions are documented.

Can returning investors go through a lighter process?

Sometimes parts of the process can be streamlined, but only if the platform can still show that the investor file remains current, risk-based, and fully reconstructable.

Conclusion

P2P lending compliance breaks down when investor onboarding is treated as secondary to borrower onboarding. The borrower may be the visible credit risk, but the investor is often the easier audit failure. Platforms that build investor KYC, source-of-funds handling, and file reconstruction into one consistent workflow are in a much stronger position when scrutiny arrives.

Want to see how VOVE ID covers P2P investor KYC end-to-end?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.