B2B Embedded Finance: How KYB Becomes Your Bottleneck

Embedded finance distributes fast. KYB still verifies slowly. Here's what breaks when the two don't align — and how to close the gap.

Why does KYB become the bottleneck in B2B embedded finance?

Because the host platform can bring distribution, demand, and transaction volume all at once, but none of that removes the need to verify the SMEs behind the flow. As of 16 June 2026, the recurring failure is simple: the product is embedded, but the KYB stack is still built like a manual back-office queue.

Embedded finance creates a seductive story.

The platform has users. The payment flow is integrated. The onboarding entry point already exists inside the host product.

The part teams miss is that a host platform does not remove compliance work. It concentrates it.

The minute the platform opens access to accounts, payouts, cards, credit, or collections, the SME population behind that platform becomes the real throughput constraint.

This is where KYB stops being a secondary workflow and becomes the thing that decides whether the product can launch cleanly at all.

Why KYB is the embedded-finance bottleneck

The host platform usually solves one problem well: it already has distribution.

It may know how the SME uses the software, what sector it sits in, and how active it is commercially.

That context helps.

It does not answer the core KYB questions on its own.

The embedded-finance provider still needs to know:

- which legal entity is actually entering the relationship

- who controls that entity

- who is authorised to act for it

- whether the business fits the permitted risk appetite

- whether the bank account, platform profile, and corporate record point to the same real counterparty

This is why embedded finance hits a specific type of bottleneck.

The commercial funnel is already wide. The decision funnel is still narrow.

If the product can surface 1,000 SMEs in a week but can only resolve 150 of them cleanly without manual handling, the problem is no longer distribution. It is KYB throughput.

For a full breakdown of entity verification, beneficial ownership logic, and KYB workflow design, see our KYB Requirements Explained 2026.

Two-sided onboarding: the host and the SME

Many teams still design embedded finance as if onboarding happens in one direction.

It does not. The provider is effectively onboarding two things at once.

1. The host platform relationship

This is the infrastructure side.

The provider needs to understand what the platform does, what customer types it brings, what products are embedded, which countries are in scope, and where risk will concentrate once the feature is live.

2. The SME population behind the platform

This is the volume side.

The provider still needs a scalable way to verify each business that will open, collect, receive, borrow, or transact through the embedded product.

The host may be one partner. The actual KYB load may be thousands of downstream businesses.

The downstream SMEs still arrive with the usual real-world mess:

- trading names that differ from legal names

- representatives who are not the listed director

- bank accounts that need reconciliation

- missing registry fields

- beneficial-owner questions that appear only in edge cases

The platform sees an activation funnel.

The compliance team sees a queue.

A realistic embedded failure: when host SMEs flunk KYB at 40%

Imagine a vertical SaaS platform launching embedded payments for its SME base.

The product team expects a fast rollout.

The host already knows its merchants. The embedded-finance provider has a clean integration and a launch deadline.

Then the first KYB cohort arrives.

Forty percent fail the first pass.

Not because forty percent are bad businesses.

Because the data path is weak.

The company name in the platform profile does not match the registry spelling. The representative completing onboarding is the finance manager, not the listed director. The payout account belongs to a related operating entity. The SME trades under a brand that the registry does not show. Several sole-trader-like businesses are being pushed through an incorporated-company workflow.

Now the conversion curve starts to bend the wrong way.

The host platform gets frustrated because the product looked integrated but does not feel launch-ready. The provider gets dragged into manual review, and revenue activation slows down.

This is not a niche problem.

It is the standard failure mode when embedded-finance distribution outruns embedded-finance identity design.

Why the first-pass failure rate matters so much

In ordinary B2B onboarding, a bad queue is expensive. In embedded finance, it is contagious.

One weak KYB flow damages four things at once:

1. Activation

The host cannot convert its SME base at the pace it expected.

2. Trust

The host starts to doubt whether the provider really understands the segment it claims to serve.

3. Unit economics

Manual-review cost rises exactly where the product was supposed to scale with software leverage.

This means one thing. A bad embedded-finance KYB flow is not only a compliance issue. It is a go-to-market issue.

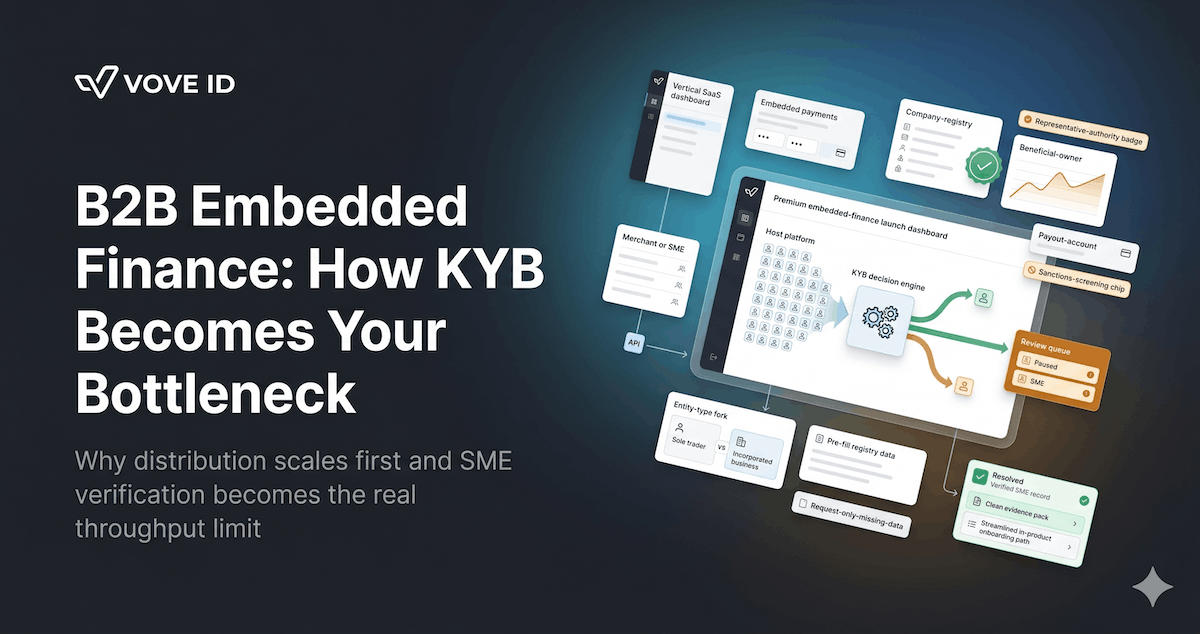

How VOVE ID streams KYB into the host platform's UX

The answer is not to push every SME into a full manual flow.

The answer is to move more of the entity-resolution work into the product path itself.

For embedded finance, that usually means:

1. Pre-fill what can be known early

If the registry can supply clean entity data, the user should not be retyping it from scratch.

2. Ask only for what is actually missing

A strong flow does not behave as if every SME is a blank file.

3. Fork the path at the right moment

Sole traders, incorporated SMEs, multi-entity sellers, and higher-risk businesses should not all travel through the same logic.

4. Keep the host experience intact

The product should finish inside the host platform wherever possible, instead of sending SMEs into a disconnected compliance side road.

This is where VOVE ID helps.

VOVE ID lets embedded-finance teams combine entity verification, representative checks, beneficial-owner logic, and structured evidence collection without turning every platform launch into a reviewer hiring plan.

Practical checklist

Host integration

- Define what the host platform already knows and what still needs regulated verification.

- Pre-fill entity fields from reliable sources before the SME starts typing.

- Keep the compliance journey inside the host UX wherever possible.

KYB

- Separate sole traders, incorporated SMEs, and multi-entity cases early.

- Reconcile legal entity, representative authority, and payout account before activation.

- Route only unresolved mismatches into manual review.

UX

- Ask for missing evidence, not generic evidence.

- Explain exactly why a case is paused when extra review is needed.

- Measure first-pass clearance, escalation rate, and manual-review depth as launch metrics.

Q&A

Why is KYB harder in embedded finance than in ordinary B2B onboarding?

Because the distribution side scales immediately through the host platform, while the compliance side still has to verify each downstream SME as a real legal and operational counterparty.

What usually causes high first-pass failure rates?

The main causes are entity-name mismatches, representative-authority gaps, payout-account inconsistencies, wrong workflow routing for entity type, and collecting too little structured data at the start of the flow.

What should teams optimise first?

They should optimise entity resolution, workflow routing, and evidence collection before trying to solve the queue with more manual reviewers.

Conclusion

Embedded finance does not usually stall because the product is not embedded enough. It stalls because the KYB layer still assumes slow, one-by-one onboarding while the host platform is delivering volume like a product channel.

The teams that scale cleanly are the ones that treat KYB as part of the product architecture from day one.

Want to see how VOVE ID keeps embedded-finance KYB inside the product path without losing control of the file?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.