MiCA in 2026: What Stablecoin Issuers Still Get Wrong About Reserve Reporting

MiCA reserve reporting isn't a monthly disclosure task. It's where stablecoin issuers find out whether their control stack actually works — or just looks clean on a website.

Reserve reporting under MiCA is not a finance afterthought. In May 2026, it is an operating-system test. If an issuer cannot reconcile tokens in circulation, reserve composition, custody, liquidity, audit evidence, and redemption flows into one coherent record, the reporting problem is not the spreadsheet. It is the control stack behind it.

What do stablecoin issuers still get wrong about reserve reporting under MiCA? They treat reserve reporting as a periodic disclosure task instead of a continuous control problem. Under MiCA, reserve evidence has to stay aligned with token issuance, custody, liquidity, redemption rights, and public disclosures. The issuer that reports clean numbers without clean underlying operations is still exposed.

For many teams, "reserve reporting" sounds narrower than it really is.

It sounds like:

- a monthly disclosure page

- an attestation pack

- a treasury reconciliation

- a legal requirement owned by finance

In practice, MiCA makes reserve reporting much broader.

For asset-referenced tokens, Article 30 requires issuers to disclose on their website the amount of tokens in circulation and the value and composition of the reserve of assets, updated at least monthly. The same article also requires publication of the audit report summary and the full unredacted audit report as soon as possible. Article 36 requires issuers to maintain a reserve of assets at all times and to manage it so that risk coverage and redemption liquidity both hold. Article 37 adds custody, segregation, and access requirements that have to work operationally, not just on paper.

For significant e-money tokens, MiCA also pulls reserve governance much closer to the prudential core. Article 58 applies the reserve, custody, and investment rules in Articles 36 to 38 and requires independent audits every six months after significance classification.

So the real issue in 2026 is not whether teams know a report is due.

It is whether the report is the visible output of a control system that can survive scrutiny.

First, fix the timeline

Many stablecoin teams still talk about MiCA as if it is an approaching event.

That is outdated.

The relevant dates are:

- 30 June 2024: MiCA started applying to asset-referenced tokens and e-money tokens

- 30 December 2024: the broader MiCA framework started applying

- 17 April 2026: ESMA stated that the MiCA transitional period ends across the EU on 1 July 2026

- 1 July 2026: the EU-wide end point for transitional periods under MiCA

That last date matters most for CASPs and market infrastructure transitions, but it also changes the climate around issuers. By mid-2026, supervisors, partners, and counterparties are no longer evaluating whether a stablecoin operator is "getting ready." They are evaluating whether the operating model is already coherent.

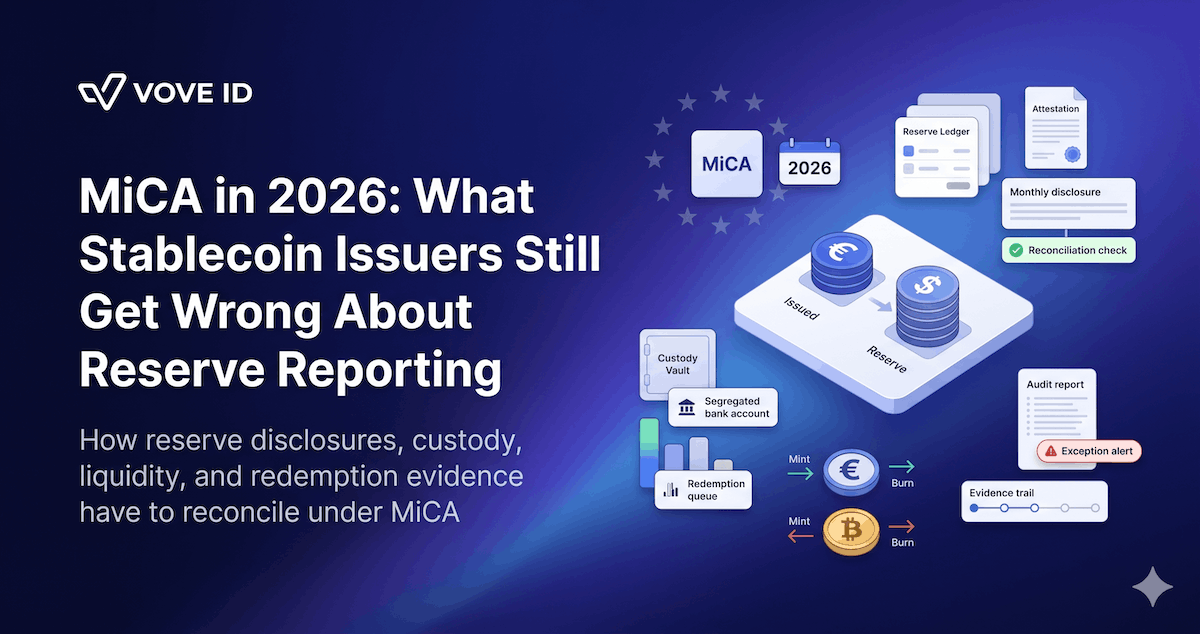

What reserve reporting actually includes under MiCA

Reserve reporting is not only a disclosure line item.

It is the point where several MiCA obligations have to reconcile:

- token supply in circulation

- reserve valuation

- reserve composition

- legal and operational segregation

- custody arrangements

- liquidity management

- redemption execution

- independent audit output

- public disclosure timing

When one of those layers is weak, the reporting issue appears fast.

1. Circulation and reserve data have to match continuously

This is the first hidden failure.

Teams often assume that if treasury knows the reserve balance and product knows token supply, reporting can be assembled later. That assumption breaks under MiCA.

Reserve reporting only works if the issuer can show, on an ongoing basis:

- how many tokens are in circulation

- which assets back them

- how those assets are valued

- where those assets are held

- what changed after issuance, redemption, or transfer activity

The failure mode is simple. Mint and burn logic lives in one system. Treasury records live in another. Custody evidence sits with one or more external institutions. Redemption events are tracked elsewhere. The monthly website disclosure becomes a manual stitching exercise.

That is exactly the wrong architecture.

2. Monthly disclosure is not the same thing as monthly understanding

For asset-referenced tokens, MiCA requires the website disclosure to be updated at least monthly. Some teams read that and infer a monthly operating rhythm.

That is too slow.

If an issuer only understands reserve composition once a month, the business is already behind.

Reserve reporting under MiCA needs near-continuous internal reconciliation even if the external disclosure cadence is monthly. Otherwise the public page becomes a lagging artifact that cannot absorb:

- rapid issuance changes

- concentrated redemptions

- changes in custodian exposure

- valuation swings

- liquidity stress

- reserve composition drift

3. Audit publication is not a substitute for reserve discipline

MiCA requires reserve-related audit visibility, but the audit is not the control.

It is evidence about the control.

Stablecoin teams often get this backwards. They prepare hard for the audit package, then underinvest in the workflows that make the audit package credible:

- reserve data lineage

- custody confirmations

- wallet-to-ledger reconciliation

- valuation methodology

- exception handling

- ownership of unresolved breaks

That approach creates a reporting function that looks polished right up to the point where a regulator or partner asks for the operational explanation behind one number.

The five reserve reporting mistakes stablecoin issuers still make

1. Treating reserve reporting like a treasury-only job

Treasury matters, but treasury does not own the full reserve story.

Reserve reporting depends on:

- product controls around minting and burning

- compliance controls around onboarding and monitoring

- finance controls around valuation and reconciliation

- legal controls around segregation and rights of holders

- operations controls around redemptions and incidents

If one team owns the report but no team owns the cross-functional workflow, the issuer has a governance gap.

2. Reporting composition without reporting liquidity reality

MiCA's reserve rules are not only about what sits in the reserve. They are also about whether the reserve can support redemption rights.

That means teams should not stop at asset labels like:

- cash

- deposits

- short-duration instruments

- highly liquid instruments

They should also understand:

- maturity profile

- concentration by custodian

- concentration by asset type

- same-day and five-day liquidity position

- whether operational access matches legal entitlement

A reserve can look conservative in a slide deck and still behave badly under redemption pressure.

3. Leaving custody evidence too far from the reporting layer

Article 37 is operationally stricter than many teams assume.

It requires custody policies and arrangements that keep assets unencumbered, avoid concentration risk, and preserve prompt access for redemption. It also requires reserve assets to be held in custody no later than five working days after issuance by a qualified custodian, depending on asset type.

The reporting implication is straightforward:

if the issuer cannot pull timely evidence from custodians into its reserve reporting flow, then the reserve page is describing an assumption, not a controlled fact.

4. Underestimating redemption evidence

Reserve reporting is inseparable from redemption logic.

MiCA gives holders of asset-referenced tokens a permanent right of redemption. That means issuers should be able to explain:

- how redemption requests are received

- how valuation is determined

- how settlement happens

- how reserve balances decrease accordingly

- how liquidity is managed during stress

Many teams can explain the policy. Fewer can demonstrate the full event trail from holder request to reserve movement to updated disclosure.

5. Publishing neat summaries while exception management stays manual

The clean reserve report is not the hard part.

The hard part is showing what happened when something did not reconcile:

- a custody statement arrived late

- a redemption queue spiked

- an internal ledger and an external wallet diverged

- an asset classification had to be corrected

- a concentration threshold was approached

That exception layer is where supervisors learn whether the issuer operates a real control system or just a periodic reporting ceremony.

A realistic reserve reporting failure in 2026

Imagine an EU stablecoin issuer that publishes its monthly reserve composition on time.

On paper, everything looks fine:

- reserve value covers tokens in circulation

- custody is outsourced to reputable institutions

- the disclosure page is live

- the audit report is posted

Then the competent authority asks a narrower question:

"Show the path from wallet-level issuance and redemption activity to the reserve balances disclosed for the same period, including breaks, overrides, and late adjustments."

This is where many issuers fail.

Not because the reserve is missing.

Because the record is fragmented:

- token events are recorded in blockchain tooling

- reserve balances are held in treasury systems

- redemption operations are logged in support or payments tooling

- custody evidence arrives in separate files

- audit support is built ad hoc for the reporting period

The report exists. The control narrative does not.

That is the reserve reporting problem MiCA exposes.

What a strong MiCA reserve reporting stack looks like

The right operating model is boring in the best possible way.

It should allow the issuer to move from token activity to reserve evidence without heroic manual effort.

That is what teams should be building toward now.

How VOVE ID fits the problem

VOVE ID is not the reserve custodian. It is the compliance and operational infrastructure that helps stablecoin teams keep the reserve story tied to the holder and transaction story around it.

That matters because reserve reporting becomes much easier to defend when the issuer can connect:

- onboarding records

- risk tiers

- holder activity

- redemption flows

- sanctions and monitoring events

- case history

into one auditable operating context.

Reserve reporting fails fastest when reserve evidence lives in one world and holder operations live in another. VOVE ID helps close that gap by making onboarding, risk, and monitoring data usable inside the broader supervisory record.

A practical checklist for stablecoin issuers

If you issue or plan to issue stablecoin products into Europe, ask these questions now:

- Can we reconcile tokens in circulation to reserve balances without manual stitching?

- Do we update internal reserve positions more frequently than the external disclosure cadence?

- Can we evidence legal and operational segregation of reserve assets?

- Can we show how redemption events affected the reserve for a specific period?

- Are custody records structured enough to support supervisory review?

- Do we have a documented exception process for reserve mismatches and late adjustments?

- If a supervisor asks for the path behind one disclosed number, can we produce it quickly?

If the answer to several of those is no, the reserve reporting issue is not the wording on the website. It is the workflow underneath it.

Conclusion

MiCA reserve reporting in 2026 is not about making the monthly page look cleaner.

It is about proving that reserve composition, custody, liquidity, audits, and redemption rights are all supported by one operating model. Article 30 forces recurring disclosure. Articles 36 and 37 force reserve and custody discipline. For significant e-money tokens, Article 58 raises the supervisory pressure further.

The issuer that still treats reporting as a periodic finance output is missing the point.

Under MiCA, reserve reporting is where the business proves that its stablecoin is operationally governed, not just legally described.

Need a compliance and monitoring layer that supports MiCA-ready stablecoin operations end to end?

FAQ

1. Does MiCA require monthly reserve disclosures?

For asset-referenced tokens, yes. Article 30 requires issuers to disclose on their website the amount in circulation and the value and composition of the reserve, updated at least monthly.

2. Is reserve reporting only a treasury task?

No. It depends on product, custody, finance, legal, compliance, and redemption operations all staying aligned.

3. What is the most common reserve reporting failure?

Treating the disclosure as the control. The real failure is usually weak reconciliation between token activity, custody evidence, and reserve valuation.

4. Why does redemption matter so much to reserve reporting?

Because MiCA ties reserve design directly to the holder's redemption rights. If the issuer cannot show how reserve assets support redemption in practice, the reporting layer is incomplete.