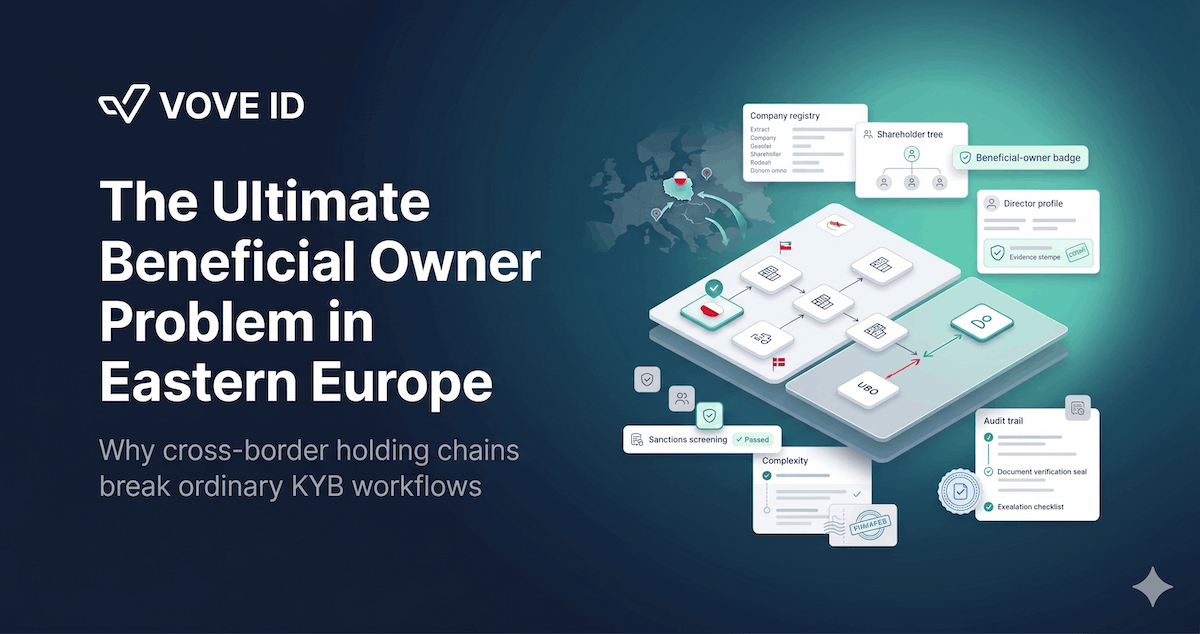

The Ultimate Beneficial Owner Problem in Eastern Europe

Eastern Europe's UBO problem isn't that companies are hard to find. It's that the local registry is usually just the first layer — and the real ownership story starts where that record ends.

Eastern Europe is one of the clearest places to see the gap between a "registered company" and a truly understood company. A local registry extract may confirm that an entity exists, but it often does not fully explain who ultimately owns it, who controls it through intermediate holdings, or which cross-border links matter most for compliance. In 2026, that is the real UBO problem.

What is the ultimate beneficial owner problem in Eastern Europe?

The UBO problem in Eastern Europe is that a domestic company record often does not give regulated businesses enough visibility into the real person behind a legal entity, especially when ownership crosses into holding companies in Cyprus, Malta, the UAE, or other jurisdictions. The operational challenge is not only identifying a company, but tracing control, documenting evidence across borders, and maintaining an audit trail that still makes sense when regulators or banking partners ask hard questions later.

When compliance teams say a UBO check is "done," they often mean one of two things:

- a local company registry returned a valid record

- a director or shareholder name was collected during onboarding

In Eastern Europe, that is rarely enough.

The real issue is not whether a company can be found. The issue is whether the ownership file explains the company well enough for a lender, payments provider, acquirer, or fintech platform to defend the relationship later.

That is where things break.

A Polish entity may look straightforward until the ownership chain runs into Cyprus. A Romanian SME may appear local until control sits with an offshore holdco. A Baltic structure may seem clean until the operating company, the parent, and the source-of-funds story stop matching neatly.

On paper, the entity exists.

In practice, the beneficial owner is still unresolved.

Why the UBO issue is sharper in Eastern Europe

Eastern Europe is not uniquely high-risk because the region is weak.

It is difficult because several realities collide at once:

- fast-moving fintech and SME ecosystems

- strong use of cross-border holding structures

- uneven public ownership data across jurisdictions

- frequent use of intermediaries, SPVs, and layered entities

- pressure from EU AML rules without uniform data access in practice

That combination creates a recurring compliance problem.

A local check may establish the immediate legal entity. But a regulated business still needs to answer harder questions:

- who ultimately owns this company?

- who controls it in practice?

- which people should be screened?

- where does the ownership chain leave the home jurisdiction?

- what evidence supports the conclusion?

Those questions matter most when onboarding:

- SME borrowers

- merchants

- B2B clients

- treasury counterparties

- platform sellers

- embedded-finance partners

The more these relationships affect money movement, credit exposure, or cross-border risk, the less acceptable a shallow answer becomes.

The registry record is only the first layer

The first mistake is confusing legal existence with beneficial ownership clarity.

A registry can be very useful for confirming:

- company name

- registration number

- incorporation status

- directors

- filing dates

- sometimes immediate shareholders

That is valuable, but it is not the end of the analysis.

The UBO question begins where the surface record ends.

If the direct shareholder is another company, the file is not finished. If the ownership chain crosses borders, the file is not finished. If voting control differs from economic ownership, the file is not finished.

In other words, the beneficial-owner problem is not caused by missing company records alone. It is caused by structures that outgrow what a single national source can explain.

Where ownership chains usually become difficult

There are several common patterns.

1. The domestic company owned by a foreign holdco

This is the classic Eastern Europe problem.

A local operating entity may be fully legitimate, but its shares are held by a Cyprus, Maltese, Dutch, or UAE company. The local file confirms the domestic company, but the true ownership trail now depends on another jurisdiction, another data source, and another evidence standard.

2. The founder story and the legal story do not match cleanly

A sales team may describe the business as founder-led. The registry may show a corporate shareholder. The board record may point to delegated directors. None of those facts necessarily indicate wrongdoing, but they do mean the compliance file has to explain control rather than assume it.

3. Nominee or administrative layers add noise

Some structures contain layers that are technically lawful but operationally unhelpful:

- nominee directors

- shelf entities

- intermediate holding companies with thin public disclosure

- administrative shareholders with little economic relevance

Those layers make it harder to determine who should actually be screened, approved, or escalated.

4. The ownership map changes faster than the KYB file

This is often missed.

Many teams eventually identify the right UBO, but the file decays because:

- a new shareholder enters

- a founder transfers control

- a financing round changes the cap table

- a restructuring moves ownership into another entity

The UBO file that was accurate at onboarding becomes incomplete months later.

Why this matters for regulated fintechs

The UBO issue is not only a documentation problem. It directly affects risk decisions.

If a fintech cannot confidently identify and evidence the real controlling person, it will struggle to make strong decisions on:

- sanctions exposure

- PEP screening

- source-of-funds questions

- EDD triggers

- transaction monitoring expectations

- credit decisions for business clients

That matters across several VOVE ID customer profiles.

For B2B fintech and KYB platforms

The problem is obvious: if the business customer's ownership chain is not understood, onboarding quality falls immediately.

For digital lenders

If the borrower is an SME, the credit decision is only as strong as the entity file. Weak UBO visibility means weaker fraud controls, weaker sanctions controls, and weaker portfolio confidence.

For payment providers and acquirers

The merchant file may look acceptable until scheme pressure, bank review, or suspicious activity forces a deeper look. If the UBO evidence is thin, the entire relationship becomes harder to defend.

A realistic Eastern Europe failure pattern

Imagine a Polish SME applying for a payment or lending product.

The local record looks clean. The directors are visible. The business activity appears ordinary.

Then the ownership trail shows that the shares are held by a Cypriot parent.

At that point, a shallow process often does one of three bad things:

- stops and asks the customer for unstructured PDFs by email

- assumes the parent entity is "good enough" and approves anyway

- sends the case into manual review with no clear next-step logic

That creates delays, inconsistency, and risk.

The customer experiences onboarding drag.

The operations team experiences document chaos.

The compliance team still does not get a confident answer.

That is the real UBO problem: the inability to turn a cross-border ownership chain into a clean, decision-ready record.

What a strong UBO workflow needs in 2026

Good UBO verification in Eastern Europe is not one lookup. It is a process.

1. Start with entity verification, but do not stop there

The first step is still basic company validation:

- confirm legal existence

- confirm registration status

- capture directors and core identifiers

- collect the entity's declared business purpose

But that should only be the opening layer.

2. Detect whether the ownership chain leaves the jurisdiction

This is where many teams lose time.

The workflow should quickly determine whether:

- the direct owner is another entity

- the ownership path crosses borders

- offshore or low-transparency layers are present

- additional evidence sources are required

If this branching logic is weak, analysts end up rediscovering the same patterns manually every time.

3. Trace control, not only shareholding labels

The best file answers a practical question:

Who ultimately controls this business?

That may involve:

- direct shareholding

- indirect shareholding

- board control

- veto rights

- founder control arrangements

- trust or nominee relationships

The point is to produce a defendable answer, not a stack of disconnected files.

4. Screen the right natural persons and linked entities

Once the real control perimeter is known, screening becomes more meaningful.

That means screening should reach:

- UBOs

- directors

- signatories where relevant

- parent entities

- other linked entities that materially affect the risk profile

5. Preserve evidence in a form that survives review

This is one of the most important pieces.

A good UBO conclusion should carry:

- the ownership logic

- the source of each conclusion

- the date the evidence was gathered

- the analyst or system decision trail

- the reason the case was approved, escalated, or declined

Without that, the team may still "know" the answer internally, but it cannot prove it later.

Why manual UBO work breaks at scale

Manual UBO resolution is usually tolerated while volumes are low.

Then it starts creating invisible costs:

- analysts spend hours stitching together ownership chains

- onboarding times become unpredictable

- commercial teams stop trusting compliance timelines

- refresh work gets skipped because new onboarding already consumes the queue

- evidence quality varies by reviewer

This becomes especially painful for:

- SME lending

- merchant acquiring

- B2B payments

- embedded finance

- treasury and high-value business onboarding

The company may think it has a UBO process.

In reality, it has expert heroics.

Those are not the same thing.

How VOVE ID helps solve the Eastern Europe UBO problem

VOVE ID is useful here because the objective is not just to collect a company document. The objective is to turn fragmented cross-border ownership evidence into one usable KYB file.

That means helping teams:

- verify the local entity quickly

- identify when the ownership chain leaves the country

- map UBO structures across jurisdictions

- screen relevant people and linked entities

- keep evidence attached to the case file

- trigger refresh or escalation when the structure changes

The product value is not "a registry result."

The product value is collapsing a five-day ownership clarification exercise into a workflow that compliance, operations, and business teams can all rely on.

A better standard for Eastern Europe KYB

If your business onboards Eastern European companies, the right standard is not:

"Did we find the company?"

The right standard is:

- Did we identify the real controlling person or persons?

- Did we understand where the ownership chain crosses borders?

- Did we screen the right people and entities?

- Did we capture enough evidence to defend the conclusion later?

- Can we refresh that conclusion when the structure changes?

That is the difference between surface KYB and durable KYB.

And in Eastern Europe, durable KYB matters more than ever.

FAQ

1. Why is UBO verification harder in Eastern Europe than a simple company lookup?

Because the local company record often confirms only the immediate entity layer. The harder part is tracing who ultimately owns or controls that entity when the ownership chain crosses into holding companies, offshore structures, or intermediate jurisdictions that do not appear clearly in the first registry result.

2. Is a registry extract enough to approve an Eastern European business customer?

No. A registry extract is useful for confirming legal existence, directors, and core identifiers, but it rarely answers the full beneficial-ownership question. A strong KYB decision also needs ownership tracing, screening on relevant people and linked entities, and evidence that can survive later review.

3. What usually causes delays in Eastern Europe UBO checks?

The biggest delays usually come from cross-border holding structures, incomplete ownership documentation, manual evidence gathering across multiple jurisdictions, and the lack of a clean workflow for deciding when the file is complete enough to approve or escalate.

4. What should a fintech capture in a good Eastern Europe UBO file?

A strong file should capture the verified entity, the real controlling person or persons, the ownership path across jurisdictions, linked screening results, the evidence sources used, and a dated audit trail that explains why the onboarding decision was made.

Conclusion

The ultimate beneficial owner problem in Eastern Europe is not that companies are impossible to verify.

It is that many compliance stacks still stop at the first layer of verification while the real ownership story begins in the second, third, or cross-border layer.

That is why teams keep getting surprised:

- the local registry was not enough

- the direct shareholder was not the real answer

- the parent jurisdiction mattered more than expected

- the evidence file did not survive review

In 2026, the teams that win in Eastern Europe are the ones that treat UBO verification as a traced, evidence-based, multi-jurisdiction process rather than a one-country lookup.

If you want to see how VOVE ID resolves cross-border UBO chains for Eastern European SMEs with faster evidence collection and a cleaner audit trail, talk to the team.