Stablecoin Remittances: When the Compliance Bill Comes Due

Stablecoin corridors compress settlement time. They don't compress the compliance workload. The bill comes due the moment fast settlement meets real counterparties, payout partners, and supervisory review.

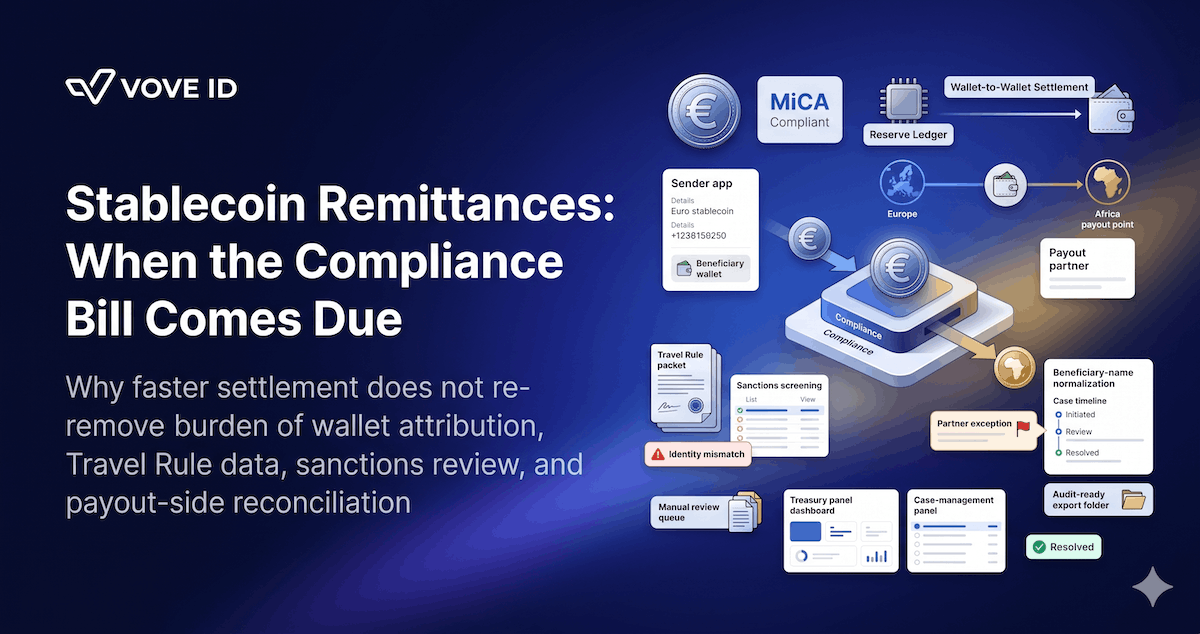

Stablecoins can reduce settlement friction in remittances, but they do not reduce compliance work by themselves. In 2026, the hard part is no longer proving that a stablecoin corridor can move value quickly. It is proving that onboarding, wallet attribution, Travel Rule data, sanctions review, and payout-side records still hold together when the corridor scales.

When does the compliance bill come due in stablecoin remittances? It comes due the moment a fast settlement flow meets real-world counterparties, payout partners, and supervisory review. By 30 June 2024, the EU had already started applying MiCA's stablecoin-specific titles, and by 30 December 2024 both the wider MiCA framework and the EU transfer-of-funds traceability regime were in force. In 2026, that means the remittance question is no longer whether stablecoins move faster. It is whether the compliance record moves with them.

VOVE ID helps stablecoin and remittance teams run compliance in corridors where the technology stack looks modern but the control stack is still fragmented. On paper, stablecoins promise cheaper corridors, faster settlement, and lower dependency on legacy intermediaries.

In practice, the compliance bill arrives as soon as the corridor becomes real.

Speed is not the hard part anymore

Most stablecoin remittance teams start with the visible advantage.

Stablecoins compress settlement time. They can simplify treasury movement. They can reduce certain forms of correspondent-banking friction. They can make corridor economics look dramatically better in a product deck.

That part is real.

But the part that decides whether the corridor survives licensing, partner due diligence, and supervision is less visible:

- who exactly the sender is

- who exactly the beneficiary is

- whether the wallet is tied to a defensible customer record

- what transfer information followed the payment

- how sanctions and screening decisions were made

- how payout exceptions were resolved

That is where the compliance bill shows up.

Why 2026 feels different

Stablecoin remittances are now operating inside a clearer European rule environment than they had before.

The MiCA regulation was published in June 2023. Its titles on asset-referenced tokens and e-money tokens started applying on 30 June 2024, and the broader framework applied from 30 December 2024. In parallel, the EU transfer traceability regime under Regulation (EU) 2023/1113 also started applying on 30 December 2024.

That combination matters.

It means a stablecoin remittance business in 2026 is not only selling speed. It is operating in a market where:

- stablecoin activity sits closer to a defined EU regulatory perimeter

- transfer traceability rules are live

- counterparties expect cleaner originator and beneficiary data

- partner banks and payout institutions ask harder questions about evidence quality

So 2026 is the year where stablecoin remittance teams discover whether their corridor is operationally compliant or only technically fast.

Where the compliance bill actually lands

The bill rarely appears in one big fine first.

It appears in accumulated friction:

- onboarding fields that were good enough for an app but not for a payout partner

- wallet addresses that were screened without being tied cleanly to a customer record

- Travel Rule packets that were transmitted but not retained in one searchable case file

- sanctions reviews that were done on one name representation while the payout instruction used another

- treasury and redemption records that never reconciled with the AML case history

This is why stablecoin remittances often feel deceptively smooth in testing and unexpectedly heavy in production.

The settlement layer scales first.

The evidence layer breaks second.

The hidden cost is reconciliation

The usual narrative says stablecoins remove intermediaries.

Sometimes they remove some of them.

They do not remove the need to reconcile records across:

- the sender app

- the KYC or KYB provider

- the wallet or on-chain monitoring stack

- the Travel Rule workflow

- the sanctions engine

- the local payout partner

- the internal case-management process

That is the real cost center.

A corridor can look efficient in treasury terms and still become expensive in compliance terms if every suspicious case needs manual reconstruction across six systems. Once that happens, the supposed efficiency of the stablecoin rail starts getting consumed by reviewer time, support time, partner escalations, and delayed payouts.

A realistic stablecoin remittance failure

A euro-denominated stablecoin remittance startup serves diaspora users in Europe and pays out to mobile-wallet users in West Africa.

The team has:

- a clean sender onboarding flow

- sanctions checks on sender and beneficiary names

- a stablecoin settlement leg between two counterparties

- a local payout partner with mobile-wallet distribution

Then the corridor hits friction.

The sender's beneficiary entry uses one spelling. The local wallet partner stores another. The payout partner asks for an additional local identifier after the stablecoin leg has already settled. The sanctions team reviewed the beneficiary record attached to the original transfer, but the payout team is working from a corrected version. The Travel Rule data packet exists, yet the exception handling notes live in a separate inbox thread.

The money moved.

The compliance file did not.

Now the institution has to answer a harder question than "Did the transfer settle?"

It has to answer:

- who exactly received value

- which identity record was used for review

- why the payout changed after settlement

- whether sanctions review still matched the final beneficiary

- how the final case maps back to the original sender file

That is when the compliance bill comes due.

What strong stablecoin remittance operations look like

Strong teams treat stablecoin remittances as one supervised workflow, not a fast treasury trick.

They connect:

- sender onboarding

- beneficiary identity collection

- wallet attribution and monitoring

- Travel Rule data handling

- sanctions and watchlist review

- payout exception management

- case retention and audit retrieval

That is the layer VOVE ID is built for.

VOVE ID helps stablecoin remittance teams keep KYC, KYB, screening, monitoring, and case management inside one operational surface so the corridor can still be explained when settlement speed stops being the main story. The goal is not only to pass a first review. It is to keep one coherent file when a partner bank, regulator, or auditor asks for a corridor-specific case.

Practical checklist for 2026 stablecoin remittance teams

Onboarding

- Collect beneficiary and corridor fields that local payout environments will actually require.

- Tie wallet identifiers to customer records instead of storing them as detached transfer metadata.

- Escalate corridor-specific data gaps before release, not after settlement.

Transfer controls

- Retain the exact payload used for the transfer and the exact version used for review.

- Keep Travel Rule and sanctions evidence attached to the same transfer event.

- Track any post-initiation data correction as a control event.

Counterparties and payout

- Know which counterparty owned each stage of the transfer path.

- Record partner exceptions inside the same case trail instead of in email-only workflows.

- Test whether payout-side data standards are stricter than sender-app collection standards.

Evidence

- Make sure treasury, payout, and AML records can be reconciled for one transfer.

- Store both the original beneficiary input and the normalized final record.

- Review repeated manual interventions as a structural corridor problem, not a support issue.

FAQ

Are stablecoin remittances easier to run from a compliance perspective?

Not by default. Stablecoins can improve settlement speed and corridor economics, but the compliance workload remains heavy if identity data, Travel Rule information, sanctions review, and payout-side records are not connected.

Why does 2026 matter specifically?

Because the EU stablecoin and transfer-traceability framework is already live. MiCA's stablecoin-specific titles started applying on 30 June 2024, and the broader MiCA and transfer-traceability rules applied from 30 December 2024. By 2026, teams are feeling the operational consequences instead of only planning for them.

What is the first major failure point?

The first major failure point is usually record consistency. A stablecoin transfer can settle correctly and still create a compliance problem if the beneficiary data, screening decision, and payout record do not line up.

What should stablecoin remittance teams fix first?

They should fix the evidence layer first: one workflow connecting sender identity, beneficiary identity, wallet context, transfer data, screening, and final case handling.

Conclusion

Stablecoin remittances do not become defensible just because they become fast.

In 2026, the real dividing line is whether the institution can move value and preserve the compliance record at the same time. The corridor that looks cheapest on a treasury slide can become the most expensive one operationally if every exception requires manual reconciliation across onboarding, screening, and payout systems.

That is when the compliance bill comes due.

Stablecoin corridors move fast. Compliance records often don't. VOVE ID helps remittance teams keep onboarding, screening, Travel Rule data, and case handling in one workflow — so the corridor stays defensible when supervisors, partners, or auditors ask hard questions.