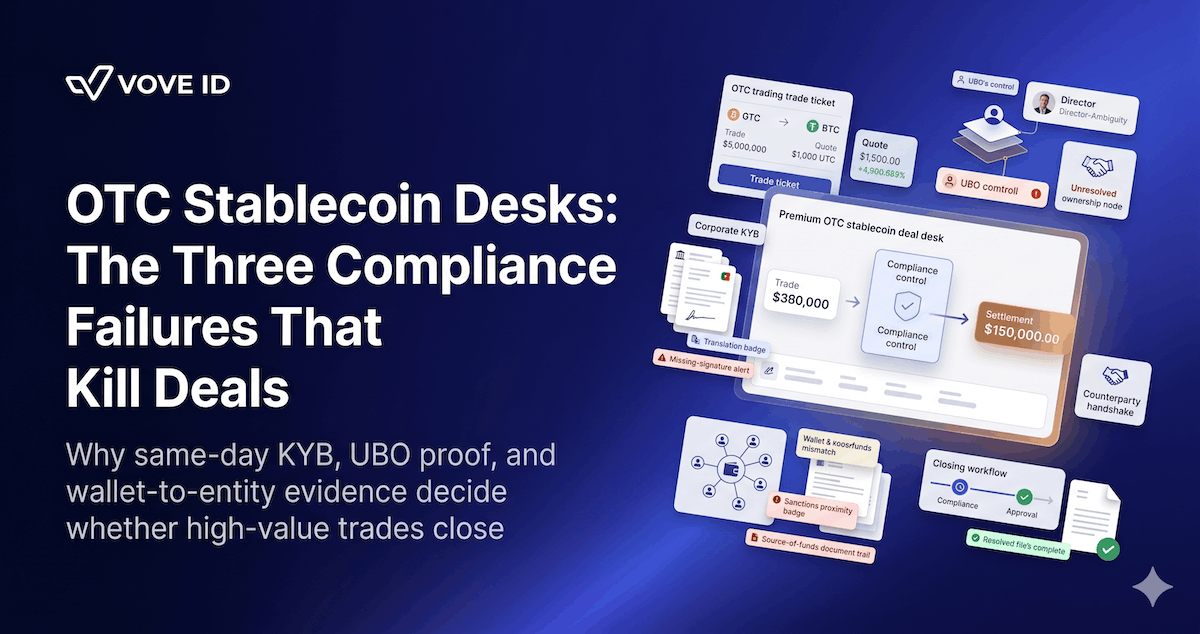

OTC Stablecoin Desks: The Three Compliance Failures That Kill Deals

OTC stablecoin desks rarely lose major trades on price alone. In 2026, deals usually fail because KYB takes too long, UBO visibility is incomplete, or the wallet and source-of-funds story cannot be tied into one defensible compliance file.

OTC stablecoin desks rarely lose serious business on spread alone. In 2026, they lose deals when the corporate counterparty cannot be verified fast enough, the beneficial-owner picture is incomplete, or the wallet, source-of-funds, and sanctions story never reconciles into one defensible file.

What are the three compliance failures that kill OTC stablecoin deals? They are delayed corporate verification, incomplete control or UBO visibility, and weak wallet-to-entity plus source-of-funds evidence. By the time pricing is agreed, those three failures decide whether the trade closes, stalls, or becomes too risky to touch.

VOVE ID helps crypto and cross-border fintech teams run compliance in markets where the counterparty wants same-day execution and the regulator still expects a full file. On paper, OTC looks lighter than exchange onboarding because the trade is negotiated directly.

In practice, OTC compresses the compliance problem into a shorter clock.

Why OTC desks now feel more compliance pressure, not less

The old story was simple.

An OTC desk knew the client, screened the wallet, checked sanctions, and settled the trade.

That model is too thin now.

The European regulatory perimeter around crypto is clearer in 2026 than it was even two years ago. MiCA's titles on asset-referenced tokens and e-money tokens started applying on 30 June 2024, the wider MiCA framework applied from 30 December 2024, and Regulation (EU) 2023/1113 also started applying on 30 December 2024 for transfer traceability around funds and certain crypto-assets.

Then FATF updated Recommendation 16 on 18 June 2025, clarifying responsibilities in the payment chain and pushing harder on the quality of information that travels with cross-border payments.

That combination matters even for OTC.

The desk is not only closing a trade.

It is building a file that has to survive:

- counterparty review

- sanctions review

- source-of-funds scrutiny

- wallet attribution questions

- later supervisory or banking-partner challenge

Why deals die in compliance before they die on price

Serious OTC buyers and sellers usually arrive with urgency.

They want:

- a quote fast

- a settlement path fast

- a clear answer fast

The desk wants the same thing.

But compliance introduces a different clock. The desk has to know:

- which legal entity is really trading

- who controls it

- where the funds originate

- whether the stated business activity matches the trade

- whether the receiving or sending wallet fits the approved counterparty

When one of those answers is weak, the trade often does not fail dramatically.

It just stops moving.

That is why the biggest OTC compliance failures are usually operational, not theoretical.

Failure 1: same-day KYB for a non-EU corporate counterparty collapses

This is the most common deal-killer.

The desk receives an inquiry from a corporate counterparty outside the EU. The trade is large enough to matter. The timing is tight. The documentation arrives in several pieces, sometimes in another language, sometimes with missing certification, sometimes with group-structure ambiguity.

The problem is not that the company necessarily looks illicit.

The problem is that the desk cannot verify it to the level the trade requires before the commercial window closes.

Same-day KYB breaks when the desk lacks:

- fast access to foreign registry data

- reliable entity matching across naming variants

- document extraction for non-English corporate records

- a clean way to escalate missing incorporation, director, or ownership evidence

So the trade stalls for a reason that was predictable.

Why this hits OTC harder than retail crypto

Retail onboarding has more time to normalize friction.

OTC does not.

The desk is often handling:

- a treasury conversion

- a corporate liquidity event

- a family-office allocation

- a cross-border settlement need

- a high-value operational deadline

If the desk cannot validate the entity within the commercial window, the deal is effectively dead even if the counterparty later produces the missing paper.

Failure 2: the entity exists, but the control perimeter is still unclear

A company registration is not the same thing as a clean approval file.

Many OTC desks get stuck here.

The corporate name is real. The incorporation documents are real. But the desk still cannot explain:

- who ultimately owns the entity

- who controls it operationally

- whether the signatory fits the ownership story

- whether there is a parent, holdco, nominee, or parallel structure that changes the risk

That gap becomes lethal when the trade is urgent.

The desk now has to choose between:

- delaying the trade until ownership is clear

- taking exposure on a partial file

- declining the business

In 2026, more desks are choosing the third option because the supervisory environment is less forgiving.

Why UBO work becomes the bottleneck

Beneficial-owner analysis is slowest exactly where the commercial pressure is highest:

- foreign holding structures

- recently formed vehicles

- non-EU entities with uneven registry quality

- family offices or investment vehicles with layered ownership

The desk may know the commercial counterparty well enough to price the trade. For a structured look at how UBO verification works across jurisdictions, see the KYB framework.

It may still know the ownership picture too poorly to approve it.

That is how UBO becomes the hidden killer of a same-day OTC deal.

Failure 3: the wallet, source of funds, and sanctions story never becomes one file

This is the failure most teams underestimate.

An OTC desk can clear the company and still lose the trade because the movement-of-value story is weak.

That weakness usually appears in one of three ways:

- the wallet is screened, but not convincingly tied to the approved entity

- source-of-funds evidence exists, but not at the right level for the size or urgency of the trade

- sanctions checks run on one name or one wallet view while the actual transaction path points somewhere else

This is where apparently small inconsistencies become fatal:

- an entity approved under one group name but settling from a different wallet cluster

- a source-of-funds explanation that makes business sense but lacks supporting evidence

- a wallet sitting close to a risky or sanctioned cluster that needs more than one-hop screening

The desk may still want to trade.

But it can no longer explain the trade simply.

That is usually enough to stop it.

A realistic OTC failure: when a fund cannot prove UBOs in 24 hours

An OTC desk in Lithuania quotes 5 million USDC to a Latin American family office.

Commercially, the opportunity is attractive.

The counterparty wants quick execution. The pricing works. The desk has available liquidity.

Then the file begins to crack.

The entity documents arrive in Portuguese. One notarial formality is missing. The signatory is authorized, but the ultimate ownership chain runs through two other companies. The desk has one receiving wallet, but the source-of-funds explanation points to assets consolidated elsewhere. Screening does not produce a clean stop, but it does produce enough proximity and ambiguity to require a second look.

Now the desk has to answer six questions in less than a day:

- which company is the actual trading counterparty

- who ultimately owns it

- whether the signatory has authority at the right level

- whether the wallet truly belongs to the approved entity

- whether source-of-funds evidence is proportionate to the size of the trade

- whether the sanctions result still holds once the full structure is mapped

If the desk cannot answer those questions fast, the trade does not close.

The client may call it delay.

Compliance should call it an incomplete file.

What strong OTC compliance looks like in 2026

The best OTC desks now treat compliance as part of execution quality, not as a post-quote gate.

That means building workflows that compress time without lowering standards.

1. Corporate verification runs in parallel, not in sequence

The desk should not wait for one document review to finish before starting the next task.

Fast desks run:

- entity resolution

- sanctions review

- document parsing

- signatory verification

- wallet screening

at the same time.

2. Wallet-to-entity binding is explicit

A screened wallet is not enough.

The desk needs a defendable explanation for why that wallet belongs to the approved business counterparty or to a clearly documented affiliate or settlement path.

3. UBO and source-of-funds review scale by deal context

Not every trade needs the same depth.

But high-value OTC cannot run on light-touch assumptions. The desk needs risk-based escalation that moves quickly without pretending every structure is simple.

4. One case file survives the whole deal

This is the real dividing line.

If the desk stores:

- entity evidence in one tool

- ownership notes in another

- sanctions review elsewhere

- wallet analysis in a separate screen

- commercial approvals in chat

then the desk does not really have a file.

It has fragments.

How VOVE ID turns OTC compliance into a closing tool

VOVE ID helps OTC and stablecoin teams compress the path from inquiry to approval without dropping control quality.

That means helping teams:

- verify foreign corporates faster

- extract and normalize non-English documents

- resolve UBO and control relationships across layered structures

- tie wallets to approved counterparties

- run sanctions and source-of-funds review inside the same case trail

The point is not only to block bad business.

It is to close good business faster because the file is strong enough early.

When compliance becomes predictable, the desk stops losing clean trades to preventable operational friction.

Practical checklist for OTC stablecoin desks

KYB

- Verify the entity before quoting size that depends on same-day execution.

- Pull foreign registry and signatory evidence in parallel.

- Escalate translation and certification gaps immediately, not at final approval.

UBO and control

- Map the control perimeter beyond the first company certificate.

- Check whether the signatory authority matches the ownership story.

- Treat layered ownership as a timing risk, not only a legal risk.

Wallet and source of funds

- Bind each settlement wallet to the approved counterparty or documented affiliate.

- Match source-of-funds evidence to trade size and urgency.

- Use multi-hop wallet screening where settlement risk justifies it.

Case integrity

- Keep entity review, wallet review, sanctions review, and approval notes in one timeline.

- Record what was still missing when a trade was delayed or declined.

- Review lost deals for recurring compliance bottlenecks and fix those upstream.

FAQ

Do OTC stablecoin desks really lose more deals to compliance than to price?

Often, yes. Once a serious counterparty accepts the spread, the bigger risk becomes whether the desk can complete KYB, ownership, wallet, and source-of-funds review fast enough to settle safely.

Why does 2026 matter specifically?

Because the EU crypto framework is already live. MiCA's stablecoin-specific titles have applied since 30 June 2024, the broader MiCA framework and the EU transfer-traceability regime have applied since 30 December 2024, and FATF's 18 June 2025 update to Recommendation 16 sharpened the direction on payment transparency.

Is wallet screening by itself enough for OTC approval?

No. Wallet screening without entity, UBO, and source-of-funds context is too thin for a serious OTC file. The desk needs the wallet story and the legal-entity story to match.

What should an OTC desk improve first?

Improve parallel review first. Most desks do not need lower standards. They need a workflow that runs entity verification, ownership review, wallet screening, and sanctions analysis together instead of one after another.

Conclusion

OTC stablecoin desks do not lose their most important deals because compliance is impossible.

They lose them because three predictable failures still happen too late in the cycle: weak same-day KYB, incomplete control visibility, and a wallet-plus-source-of-funds story that never becomes one defensible record.

In 2026, the desk that closes best is often the desk that files best.

That is what makes compliance a closing tool instead of a closing delay.

OTC stablecoin desks lose clean deals when KYB, UBO, sanctions, and wallet review run too slowly or land in separate tools. VOVE ID turns those four workflows into one fast approval file — so compliance becomes a closing tool, not a closing delay.