Why Romanian and Polish Remittance Startups Need a Multi-Jurisdiction Stack

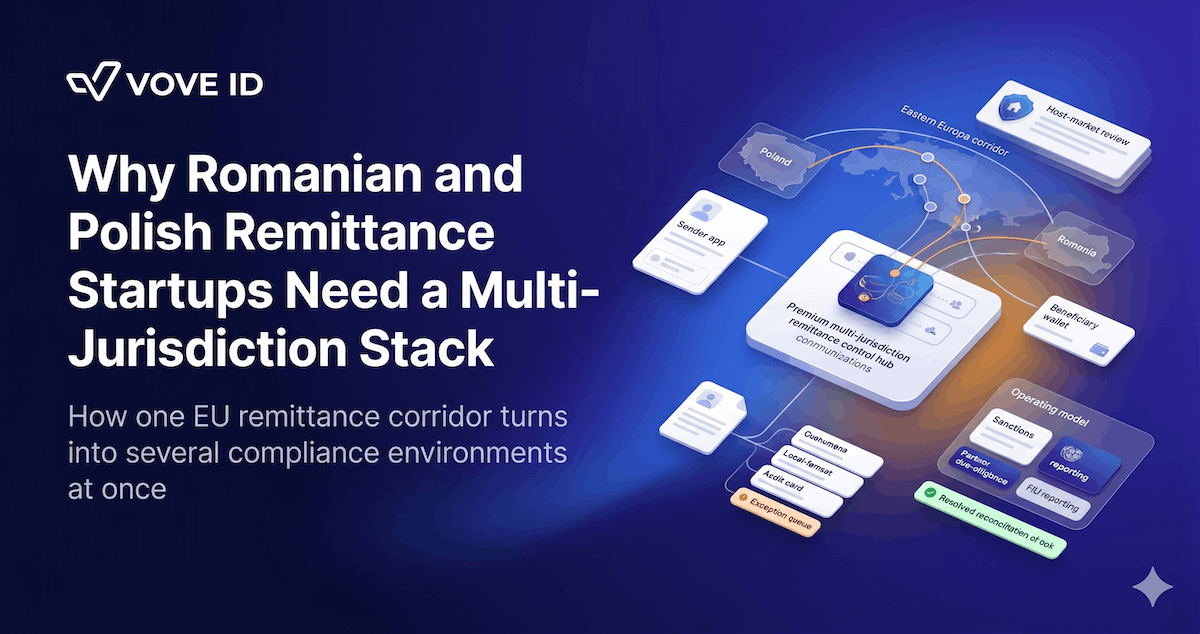

Romanian and Polish remittance startups rarely operate inside one jurisdictional reality. In 2026, EU passporting may open market access, but corridor operations still depend on foreign payout partners, local AML expectations, beneficiary-side identity rules, and cross-border evidence portability.

For remittance startups in Poland and Romania, the product may launch from one home market, but the compliance exposure never stays there. In 2026, a corridor that starts with one EU license can still trigger host-state AML questions, payout-partner data demands, FIU reporting issues, and counterparty-review gaps across several jurisdictions at once.

Why do Romanian and Polish remittance startups need a multi-jurisdiction stack? Because the business model crosses more jurisdictions than the license does. A Polish or Romanian startup may be supervised from home, but the corridor still depends on foreign payout partners, beneficiary-side identity rules, local FIU expectations, and sometimes crypto-asset traceability rules that do not fit inside one domestic workflow.

VOVE ID helps cross-border fintech teams run compliance in corridors where one onboarding record has to survive several legal and operational environments at once. On paper, a home-market authorization, a passport notification, and a payout integration can look sufficient.

In practice, a remittance startup serving diaspora corridors is rarely operating in one jurisdictional reality.

The home state is real, but it is not the whole operating model

Poland and Romania both give fintech founders a credible EU starting point for payments and remittance infrastructure.

That matters.

Under the PSD2 framework, payment institutions and e-money institutions can use passporting routes to serve more than one EU Member State. The European Banking Authority's PSD2 passporting standards have been in force since 2 December 2017, and they are specifically designed to structure information exchange between home and host authorities for branch establishment, agent activity, and freedom-to-provide-services models.

But founders often overread what that means.

Passporting helps a firm extend regulated activity across the EU.

It does not mean that:

- beneficiary-side identity standards become uniform

- payout-partner documentation requirements become identical

- host-market AML expectations disappear

- suspicious-activity reporting logic becomes one-size-fits-all

- evidence requests arrive in one shared format

That is the first reason a multi-jurisdiction stack becomes necessary.

Romania and Poland sit inside corridor businesses, not only domestic ones

This is especially visible in remittance.

A Romanian or Polish startup often serves:

- diaspora users sending outward from the EU

- beneficiaries in non-euro markets nearby

- payout partners in neighboring states

- treasury or settlement counterparties across several countries

- banks and payment institutions reviewing the corridor from different angles

So the firm may be licensed in one country while operationally exposed to four or five.

That is not a niche scenario.

It is the default cross-border remittance model in Eastern Europe.

The oversight architecture already hints at this. The Polish Financial Supervision Authority (KNF) maintains the payment-institutions framework under Poland's payment-services regime. Romania's National Bank supervises Romanian payment institutions and electronic money institutions, including activity conducted directly in another EU Member State, while Romania's ONPCSB acts as the country's financial intelligence unit under Law No. 129/2019.

The legal perimeter starts at home.

The evidentiary perimeter does not.

Why a single-jurisdiction stack breaks faster than founders expect

Single-jurisdiction stacks usually assume that one KYC flow, one case format, and one reporting logic can stretch across the whole corridor.

That assumption breaks in three places.

1. Beneficiary identity does not travel cleanly

The sender-side record is usually stronger.

The startup owns onboarding on that side. It controls the app, the KYC provider, the sanctions engine, and the transaction trigger.

The beneficiary side is weaker because it depends on:

- local naming conventions

- local identifiers

- payout-partner data rules

- corridor-specific exception processes

- whatever evidence the foreign partner can actually return

A sender file that looks fully compliant in Warsaw or Bucharest can still fail when a foreign payout partner asks for a field that was never captured upstream.

2. Reporting and review obligations do not arrive in one format

A corridor can be commercially simple and operationally fragmented.

One institution wants the original onboarding evidence. Another wants the normalized beneficiary record. A third wants proof that the sanctions review matched the final payout data, not the first draft.

This is where a domestic-only stack struggles.

It can store documents.

It often cannot re-express the same case in the format a host-country reviewer, partner bank, or FIU-adjacent inquiry will expect.

3. Partner and counterparty risk outgrows the license framework

Remittance businesses do not run on licensing alone.

They run on counterparties:

- payout institutions

- wallet providers

- banking partners

- treasury venues

- corridor intermediaries

Once those relationships span multiple markets, the startup has to show more than its own authorization. It has to show how it evaluates the businesses and infrastructure touching the corridor. For a deeper look at what business verification involves at this level, see the KYB framework.

That is where a multi-jurisdiction stack becomes more than a nice-to-have.

It becomes the operating model.

2026 raises the bar further for mixed fiat and crypto corridors

Some Romanian and Polish remittance startups now mix:

- fiat collection on the EU side

- stablecoin settlement in the middle

- local-currency or wallet payout on the receiving side

That makes the evidence problem even harder.

Regulation (EU) 2023/1113 has applied since 30 December 2024. For firms touching crypto-asset transfer chains, payer and payee traceability now sit inside a live EU regime rather than a future-planning discussion. FATF then updated Recommendation 16 on 18 June 2025, clarifying responsibilities in the payment chain and reinforcing the direction toward better payment transparency.

So if a corridor mixes regulated payments, crypto settlement, and foreign payout, the startup is not reducing the need for compliance coordination.

It is increasing it.

A realistic failure: when the receiving country audits the sender's KYC

A Polish-licensed remittance API serves corridors into Moldova, Romania, Ukraine, and Bulgaria.

The startup has:

- a working sender onboarding flow

- sanctions checks at transfer creation

- a local payout network in each receiving market

- a central case-management view for the Polish team

The business scales.

Then a Romanian review connected to one corridor asks for the original onboarding evidence behind a sender whose funds were paid out locally.

The file exists.

But not in the right shape.

The Polish onboarding system stores one set of document labels. The Romanian-side review wants evidence classified differently. The beneficiary record was corrected by the payout partner after initiation. The sanctions review note sits in one queue, while the transfer exception note sits in another.

Now the startup has to reconstruct:

- which sender identity was verified

- which beneficiary record was finally paid

- which data fields changed after initiation

- whether the screening decision still matched the final transfer data

- how the case should be presented to a foreign reviewer

The corridor did not fail because the money could not move.

It failed because one domestic stack could not explain a multi-jurisdiction event.

What a real multi-jurisdiction stack includes

The answer is not building a different core product for every corridor.

It is building one compliance operating layer that can absorb jurisdictional variation without losing record integrity.

That usually means:

- one canonical sender record with jurisdiction-specific output formats

- one beneficiary model that stores both original input and local normalized output

- corridor-level rules for extra fields, identifiers, and exception thresholds

- partner-side notes and evidence stored inside the same case trail

- reporting overlays that can present one event differently for different authorities or partners

That is the difference between a domestic workflow and a multi-jurisdiction stack.

One stores the case.

The other makes the case portable.

How VOVE ID adapts one stack to multiple jurisdictions

VOVE ID is built for teams that do not want to rebuild compliance every time a corridor crosses a new border.

For Romanian and Polish remittance startups, that means helping teams:

- normalize sender and beneficiary records across markets

- attach corridor-specific evidence to the same transfer event

- track foreign payout exceptions without losing the original onboarding context

- score counterparty and corridor risk at the operating layer

- retrieve one file that still makes sense when another jurisdiction asks the question

The benefit is not abstract.

It is operational.

A corridor becomes easier to defend when:

- the home supervisor asks about foreign activity

- the receiving market asks for sender evidence

- a partner bank wants a corridor-specific control explanation

- a mixed fiat-crypto payout path triggers traceability questions

Practical checklist for Romanian and Polish remittance teams

Home-state control

- Know which parts of the workflow are actually covered by the home authorization.

- Separate licensing comfort from corridor evidence readiness.

- Treat passporting as a market-access mechanism, not a full compliance model.

Beneficiary and payout

- Capture corridor-specific payout identifiers before the transfer reaches the foreign partner.

- Store the original beneficiary data and the final normalized payout record together.

- Review which corridors generate repeated data repairs and redesign those fields upstream.

Counterparties

- Map which legal entity owns each payout, treasury, and settlement relationship.

- Keep partner exceptions inside the case file instead of in email-only workflows.

- Score counterparty quality as part of corridor risk, not as a separate vendor task.

Evidence and reporting

- Make one sender file portable across multiple output formats.

- Keep sanctions, transfer, and payout exception notes in one timeline.

- Test whether another jurisdiction could understand the case without manual reconstruction.

FAQ

Isn't an EU passport enough for cross-border remittance expansion?

No. An EU passport helps a payment institution or e-money institution extend regulated activity, but it does not remove local AML expectations, partner due diligence, foreign payout data requirements, or record-format differences across corridors.

Why are Romanian and Polish startups especially exposed?

Because they often build diaspora and near-neighbor corridors that touch several jurisdictions at once. The business may be licensed from one home market while depending on payout, banking, and review environments in multiple others.

Does this only matter for crypto-heavy corridors?

No. It matters for fiat remittance too. Crypto or stablecoin settlement only makes the problem sharper because traceability and counterparty evidence now have to survive another layer of complexity.

What should founders fix first?

Fix the evidence layer first. The startup needs one canonical case model that can absorb jurisdiction-specific fields, partner exceptions, and reporting requests without rebuilding the file every time.

Conclusion

Romanian and Polish remittance startups do not outgrow a domestic compliance stack because they get bigger.

They outgrow it because the corridor is bigger than the home market from day one.

In 2026, the winning teams are not the ones that only add more payout routes. They are the ones that can keep sender records, beneficiary records, partner exceptions, and reporting evidence coherent when several jurisdictions touch the same transfer.

That is what a multi-jurisdiction stack is for.

Romanian and Polish remittance teams operating across multiple corridors need more than a home-market authorization. VOVE ID connects sender verification, beneficiary records, partner exceptions, and reporting evidence into one stack that holds up when several jurisdictions touch the same transfer.