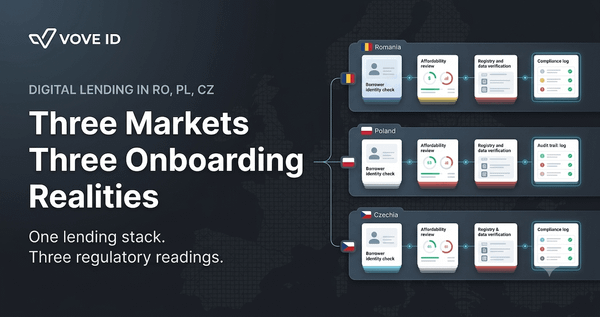

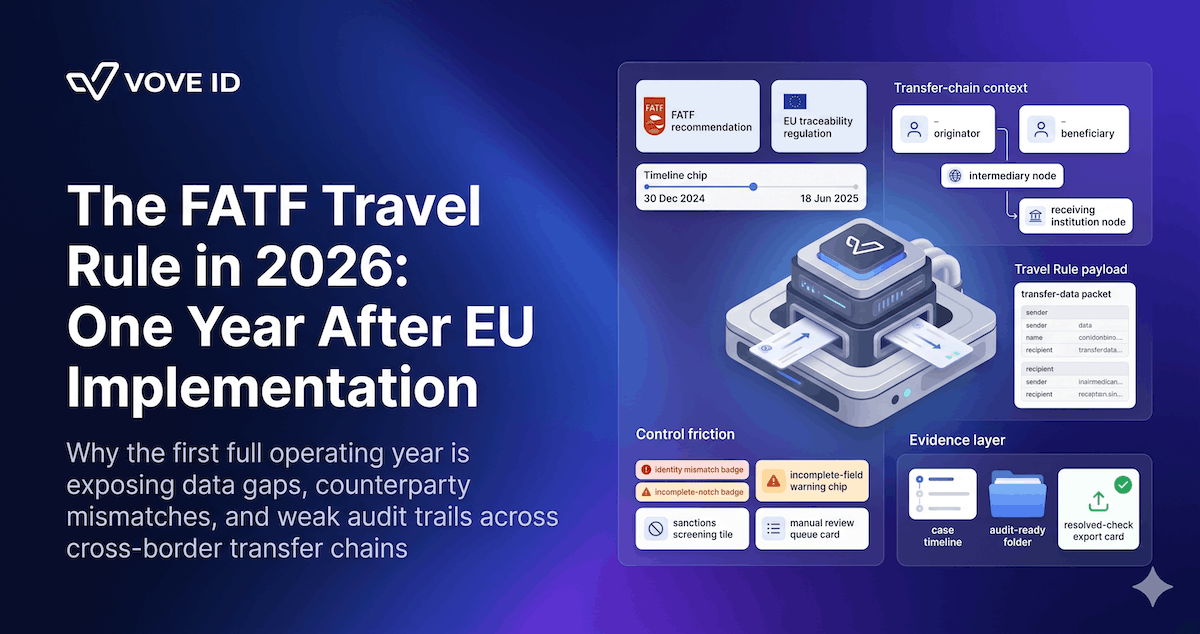

The FATF Travel Rule in 2026: One Year After EU Implementation

The EU Travel Rule has been live since December 2024. One year in, the real question isn't whether firms can send the packet. It's whether the transfer record, screening decision, and case history still describe the same event after the payment chain introduces friction.

In 2026, the FATF Travel Rule is no longer a policy project for European crypto and cross-border payment teams. The EU regime started applying on 30 December 2024, FATF updated Recommendation 16 on 18 June 2025, and the real question now is whether originator data, beneficiary data, screening decisions, and case handling stay coherent when transfers move across multiple counterparties.

What does the FATF Travel Rule look like in 2026, one year after EU implementation? It looks less like a messaging problem and more like an operating-model problem. The EU's traceability rules have already been live since 30 December 2024, FATF tightened the global payment-transparency direction on 18 June 2025, and fintech teams now have to prove that sender records, beneficiary records, sanctions checks, and exception handling all survive the full transfer chain.

VOVE ID helps crypto, stablecoin, and cross-border fintech teams run compliance in markets where transfers move quickly and records break quietly. On paper, the Travel Rule sounds straightforward: collect the required information, transmit it, and keep it available.

In practice, 2026 is where the evidence layer gets tested.

What changed in Europe first

The EU did not leave the Travel Rule as a vague principle.

Regulation (EU) 2023/1113 has applied since 30 December 2024. It requires information on payers and payees to accompany transfers of funds and extends a similar traceability model to certain crypto-asset transfers. For firms handling cross-border crypto flows, that means Travel Rule compliance is not a side workflow anymore. It is part of the transfer itself.

This matters because the operating burden lands in three places at once:

- collection of the right originator and beneficiary information

- transmission of that information to the next institution or crypto-asset service provider

- retention of a defensible record when the transfer later becomes a sanctions, fraud, or audit question

The regulation made the obligation clearer.

It did not make the operating model easier.

What FATF changed next

The FATF direction kept moving after the EU implementation date.

On 18 June 2025, FATF updated Recommendation 16 on payment transparency. FATF said the revision clarifies responsibilities in the payment chain and strengthens transparency for cross-border payments over USD/EUR 1,000, with formal compliance against the revised standard measured from the end of 2030.

That future deadline can mislead teams.

The operational signal is immediate. Supervisors, partner institutions, and infrastructure providers already know where the direction is going:

- clearer responsibility at each point in the payment chain

- better integrity of originator and beneficiary information

- stronger controls around incomplete, inconsistent, or suspicious transfer data

- less tolerance for fragmented handoffs that only look complete on paper

So 2026 is not a waiting period.

It is the first full operating phase where European implementation and FATF direction now point the same way.

Why 2026 feels harder than the launch date

The launch date mostly tests connectivity.

The year after launch tests everything else.

Teams now know whether their Travel Rule flow breaks on:

- missing beneficiary fields from upstream onboarding

- name mismatches across counterparties

- weak wallet-to-customer linkage

- sanctions reviews tied to one record while the transfer used another

- manual exception handling that never makes it back into the audit trail

That is why the pressure feels different in 2026.

The early question was whether the packet could be sent.

The later question is whether the packet, the customer file, and the case history still describe the same transfer after something goes wrong.

The common failure is not transmission

Many teams still frame the Travel Rule as a transmission problem.

That is too narrow.

A transfer can technically move with the required fields and still create a compliance failure if the receiving side cannot use those fields cleanly. The weak point is often not the first message. It is the mismatch between:

- the identity record gathered at onboarding

- the transfer record generated at execution

- the sanctions or screening record reviewed by compliance

- the exception notes kept by operations or a corridor partner

When those records drift apart, the institution no longer has one Travel Rule file.

It has several fragments that need to be reconstructed after the fact.

A realistic 2026 failure

A European stablecoin payments startup routes transfers to an offshore virtual-asset counterparty and then to a local payout partner.

The startup has:

- a valid sender KYC file

- a beneficiary name and wallet identifier

- a transfer packet sent on time

- sanctions checks on both sides of the transaction

Then the problem appears.

The beneficiary name was collected in one format at onboarding and another at the payout edge. The receiving counterparty accepted the transfer, but the payout partner flagged the wallet record for an additional identifier. The sanctions reviewer looked at a slightly different beneficiary representation than the one attached to the final payout instruction.

The transfer is not obviously unlawful.

But the case record is no longer clean.

Now compliance has to explain:

- which beneficiary identity was actually reviewed

- which version of the data was transmitted

- why the exception occurred

- who approved release or rejection

- how the final decision maps back to the original customer file

That is the real Travel Rule burden in 2026.

What strong Travel Rule operations look like now

Strong teams have stopped treating Travel Rule compliance as a messaging add-on.

They treat it as one controlled workflow that connects:

- onboarding and identity collection

- transfer creation and counterparty messaging

- sanctions and watchlist review

- exception handling and escalation

- record retention and retrieval

That is where VOVE ID fits.

VOVE ID helps teams keep one operational file across KYC, KYB, screening, monitoring, and case management so the transfer can still be explained after the payment chain introduces friction. Instead of letting each system keep a partial truth, the workflow keeps the originator record, beneficiary record, screening outcomes, and reviewer notes tied to the same event.

The benefit is not only cleaner operations.

It is a defensible file when a supervisor, partner, or auditor asks a narrow question about one transfer.

Practical 2026 Travel Rule checklist

Data collection

- Collect the exact beneficiary fields your counterparties and payout environments actually need.

- Keep wallet, account, and customer identifiers linked instead of storing them as separate references.

- Reject handoffs that rely on free-text repair later.

Transfer chain

- Track which institution or service provider held responsibility at each stage of the payment path.

- Retain the exact transfer payload that was transmitted, not a later reconstruction.

- Log every exception that changes the transfer outcome or data interpretation.

Screening and review

- Run sanctions and watchlist review against the same identity representation used for execution.

- Escalate recurring beneficiary mismatches as a control problem, not only an ops nuisance.

- Make sure analysts can see both the original input and the normalized final record.

Evidence

- Keep one case trail for transfer creation, exception handling, review, and final decision.

- Test whether one file can explain a suspicious transfer end to end.

- Remove workflows that depend on spreadsheets, screenshots, and partner inboxes to rebuild the story.

FAQ

Did the EU Travel Rule start in 2026?

No. The EU traceability regime under Regulation (EU) 2023/1113 started applying on 30 December 2024. The reason 2026 matters is that it is the first full operating period after implementation, when real exception patterns become visible.

What did FATF change in 2025?

On 18 June 2025, FATF updated Recommendation 16 on payment transparency to clarify responsibilities in the payment chain and strengthen transparency for cross-border payments over USD/EUR 1,000, with formal compliance against the revised standard measured from the end of 2030.

What is the main 2026 Travel Rule risk for fintechs?

The main risk is not only missing a field. It is losing consistency between the onboarding record, transfer message, sanctions review, and final case decision. That is what turns a technical transfer issue into a governance issue.

What should teams fix first?

Fix the evidence layer first. The institution needs one workflow that connects sender identity, beneficiary identity, transfer data, screening results, and review notes in one retrievable file.

Conclusion

The FATF Travel Rule in 2026 is not mainly about whether firms can send data.

It is about whether they can keep the transfer record coherent when counterparties, payout environments, and compliance reviews all touch the same event. The EU implementation date of 30 December 2024 made the obligation real. FATF's 18 June 2025 update made the direction even clearer.

Teams that still treat Travel Rule compliance as a packet problem will keep discovering the same failure later: the transfer moved, but the evidence did not.

The EU traceability regime is live. FATF's direction is clear. VOVE ID helps crypto and cross-border fintech teams keep sender records, beneficiary data, screening decisions, and case notes in one audit-ready workflow — so the transfer can still be explained after the payment chain introduces friction.