Why One-Size-Fits-All KYB Fails in Africa and MENA

Most KYB vendors were designed around German Handelsregister logic. That assumption fails in markets where registry data is sparse, UBO disclosure is informal, and document formats vary by city.

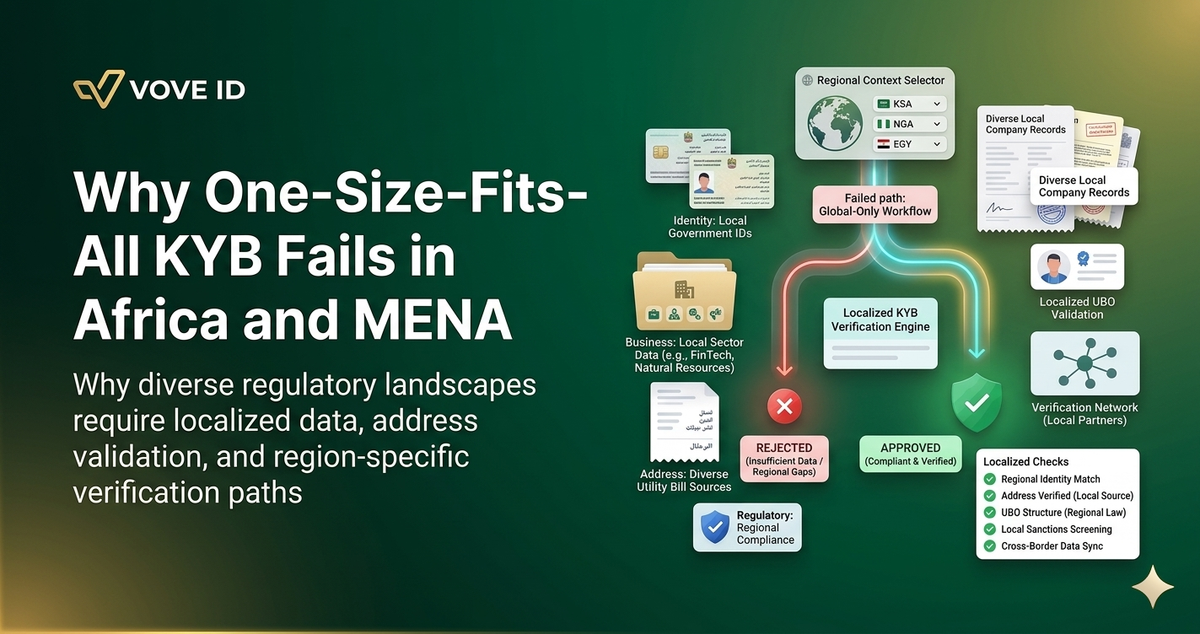

Most KYB tools were designed with a specific assumption baked in: that a company registry exists, is current, and can be queried programmatically. That assumption holds in Germany, the Netherlands, or France. It breaks in a lot of the markets where cross-border fintech is actually growing.

VOVE ID works with compliance teams onboarding business clients across Africa and MENA — markets where registry infrastructure, document formats, entity structures, and regulatory pressure all look different from what most KYB vendors were built to handle. This article covers where the standard KYB playbook fails in these regions, and what teams need to do differently.

This article covers the operational failure points in Africa and MENA specifically. For the full KYB framework, see our KYB Requirements Explained 2026.

The Registry Problem

In most Western European markets, company registration data is centralized, public, and machine-readable. The KYB workflow that grew up around this infrastructure treats registry lookup as step one — confirm legal existence, pull registration number, cross-reference filed documents.

That workflow starts to fail in Africa and MENA at the registry stage itself.

In Nigeria, the Corporate Affairs Commission (CAC) maintains a central register, but data completeness varies and agent-based onboarding is common enough that the registered address and operating address frequently don't match. In Egypt, commercial registry data exists across governorate-level offices — there's no single national lookup. Saudi Arabia's MISA (Ministry of Investment) and SACO (Saudi Authority for Accredited Valuators and Analysts) have improved digital access, but foreign-invested entities, holding structures, and free zone registrations are held under different authorities and have different disclosure rules.

Across Francophone West Africa — Senegal, Côte d'Ivoire, Cameroon, Gabon — the OHADA legal framework standardizes commercial law, but the underlying registries (RCCM) are maintained at the national level and digital access is inconsistent. An RCCM extract may be current as of filing date but not reflect subsequent changes in ownership or management.

The practical problem for KYB teams: a vendor tool that queries one registry per jurisdiction and treats no result as a failure will generate a lot of false negatives, false positives, and dead ends in these markets. The registry is a starting point, not the whole picture — and in some jurisdictions, it's a weak starting point.

UBO Disclosure Is Structurally Different

The 25% UBO threshold is standard in FATF-aligned jurisdictions. The problem isn't the threshold; it's the disclosure infrastructure around it.

In the EU, beneficial ownership registries are public in most member states (France's INPI, the Netherlands' UBO Register, Spain's Registro Mercantil). The French UBO register was restricted in mid-2024 following a CJEU ruling, but still accessible to obligated entities. In most African and MENA jurisdictions, there is no equivalent public registry.

Saudi Arabia introduced UBO regulations in April 2025, requiring disclosure of beneficial owners holding 25% or more and mandating updates within 15 days of any ownership change. That's a real change. But disclosure goes to MISA and isn't publicly searchable — KYB teams onboarding Saudi entities can't verify UBO by querying a registry. They're relying on declared information and document review.

In Gabon, there's no public UBO registry at all. Beneficial ownership is disclosed in RCCM filings where applicable, but coverage for holding structures and foreign-controlled entities is thin. Angola added UBO requirements under Law 5/20 and BNA Directives 01/2025 and 02/2025, but enforcement is early-stage and registry quality hasn't yet caught up with the regulation on paper.

Across sub-Saharan Africa more broadly, the UBO gap runs through holding company layers, family-controlled groups, and nominee arrangements that aren't prohibited but also aren't captured in standard registry data. KYB vendors built to pull UBO data from a register will surface nothing — and the compliance team has to decide whether "nothing" means compliant or means the data isn't there.

Document Formats Don't Fit Standard Templates

Most KYB document review is built around a predictable set of document types: articles of incorporation, certificate of good standing, shareholder registry, director IDs. The formats vary but the categories are stable. In Africa and MENA, the documents themselves work differently.

Arabic-language commercial documents are the norm across MENA. A KYB workflow that can't process Arabic text — trade licenses from DIFC or ADGM in the UAE, commercial registration certificates from Saudi Arabia or Egypt, memorandums of association in Jordan or Kuwait — either requires manual translation at every step or produces incomplete data on entity details, registered agents, and ownership structure.

Portuguese is the document language across Angola, Mozambique, and Cabo Verde. French governs Francophone West and Central Africa. Swahili is widely used alongside English in Tanzania. Document review tools built primarily for English-language filings create friction at the extraction stage before KYB analysis even starts.

Beyond language, document formats are less standardized. A Kenyan company certificate from 2015 looks different from one issued in 2022 after the Business Registration Service digitized its processes. A Tanzanian corporate file may include a certificate of incorporation, a certificate of compliance, and TIN documentation as separate physical documents, not a single extract. In Nigeria, the CAC issues different certificate formats depending on when and how the entity was registered.

VOVE ID handles document verification across 190+ countries with OCR that covers Arabic, Portuguese, and other local-language formats — so the document review layer works across jurisdictions rather than defaulting to manual processing for anything outside English or EU languages.

Entity Structures Are Different

Standard KYB logic maps well onto a Ltd. or GmbH with a small number of identified shareholders and a clear corporate hierarchy. The entity structures common in Africa and MENA introduce variations that complicate that model.

In MENA, layered holding structures are common — particularly in UAE free zones, Saudi Arabia's corporate ecosystem, and Gulf family business groups. A Cayman-registered holding company may own a DIFC-incorporated intermediate vehicle that in turn holds operating entities in Saudi Arabia and Egypt. Each layer requires separate registry verification, and the beneficial owner at the top may be documented in a jurisdiction with limited disclosure requirements. Free zone entities in UAE (JAFZA, DIFC, ADGM, RAKEZ) have separate registration authorities from mainland DED-registered entities, with different documentation and disclosure rules.

In Africa, mobile money operators and fintech platforms often work through agency networks and sub-agent structures that don't map neatly onto standard corporate entity models. KYB for a mobile money principal is straightforward; KYB for an agent network that's processing transactions introduces questions about entity scope that aren't answered by a registry lookup.

Across West Africa, particularly in Francophone markets, OHADA-governed entities (SARL, SA, SAS) have defined structures, but the practical ownership verification often runs through shareholder registers that are held by the entity itself, not deposited in a public registry. The document is real; it just has to be requested and reviewed rather than pulled from a database.

FATF Pressure Without Registry Infrastructure

Nine African countries are currently on the FATF grey list, including Tanzania (which exited in June 2025, under enhanced monitoring), Angola (added in 2023), and several others across sub-Saharan Africa. Grey list status means regulators in those countries are under pressure to demonstrate AML/CFT effectiveness, which flows downstream to obligated entities, including any fintech or financial institution onboarding business clients there.

The practical tension: grey list countries often have the weakest registry and UBO disclosure infrastructure, which means compliance teams face the highest regulatory scrutiny at exactly the point where automated verification tools are least reliable.

Tanzania's fintech sector grew around 63 million mobile money subscriptions with 1.4 million agents — onboarding at that scale with manual document review for every business client isn't operationally viable. But the data infrastructure that would support automated KYB at scale is still developing. KYB programs that work there have to be designed around the available data, not around the assumption that registry data fills the same role it does in Europe.

For the AML compliance context across African markets, see our AML Requirements Explained 2026.

What "Adapted KYB" Actually Means

Adaptation isn't a feature; it's a design choice about what happens when standard data sources return incomplete results.

Document-first verification. In markets where registry data is thin or access is inconsistent, the document layer carries more of the verification weight. That means the KYB workflow needs to be able to extract and process entity information from source documents — not just cross-reference a registry output against a submitted document.

Manual escalation that's structured, not ad hoc. Not every KYB case in Africa or MENA will close automatically. The question is whether the manual review workflow is integrated — with clear decision points, documented rationale, and audit-ready outputs — or whether "we couldn't verify this automatically" triggers an unstructured process that leaves gaps in the compliance record.

UBO verification that works without a public registry. For jurisdictions without public UBO registries, beneficial ownership verification runs on declared documents (shareholder registers, UBO declarations, corporate constitutional documents) plus identity verification on the declared individuals. VOVE ID supports biometric verification and document review for UBO individuals in exactly these cases — where the registry doesn't surface beneficial ownership and the compliance team needs to verify identity on the declared ownership chain.

Ongoing monitoring that accounts for registry lag. Even where registry data is accessible, changes in ownership or management may take weeks or months to appear. Ongoing KYB monitoring in these markets can't rely solely on registry refresh as a signal of change — it needs to include document update requests and periodic re-verification as part of the process.

Sanctions screening that covers relevant lists. UAE, UN, EU, and OFAC lists are baseline. For MENA markets, coverage of relevant regional designations matters. For African markets, understanding which sanctions regimes apply to the counterparty's jurisdiction and sector is part of calibrating the screening setup rather than applying a single global standard uniformly.

The Vendor Selection Problem

Most KYB vendors were built for European or North American markets and then extended to other regions. That extension often means coverage exists on paper — the vendor will claim to support KYB in Nigeria or Egypt — but the underlying workflow assumes registry data quality that isn't there. The failure mode is invisible: the tool processes the case and returns a result, but the result is built on incomplete data that the team doesn't know is incomplete.

Compliance teams evaluating KYB vendors for Africa or MENA operations should ask specific questions: What happens when registry data is unavailable or incomplete? How does the platform handle Arabic-language or Portuguese-language documents? What does the UBO verification workflow look like in markets without a public UBO registry? What's the case escalation process and what does the audit trail look like for manually reviewed cases?

The answers reveal whether the vendor has actually built for these markets or has an aspirational coverage map.

Running KYB programs across Africa or MENA and finding that standard vendor tools don't handle the edge cases? VOVE ID supports entity verification, UBO identity checks, and document review in Arabic, Portuguese, and other regional formats — across the jurisdictions where the standard playbook breaks.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.