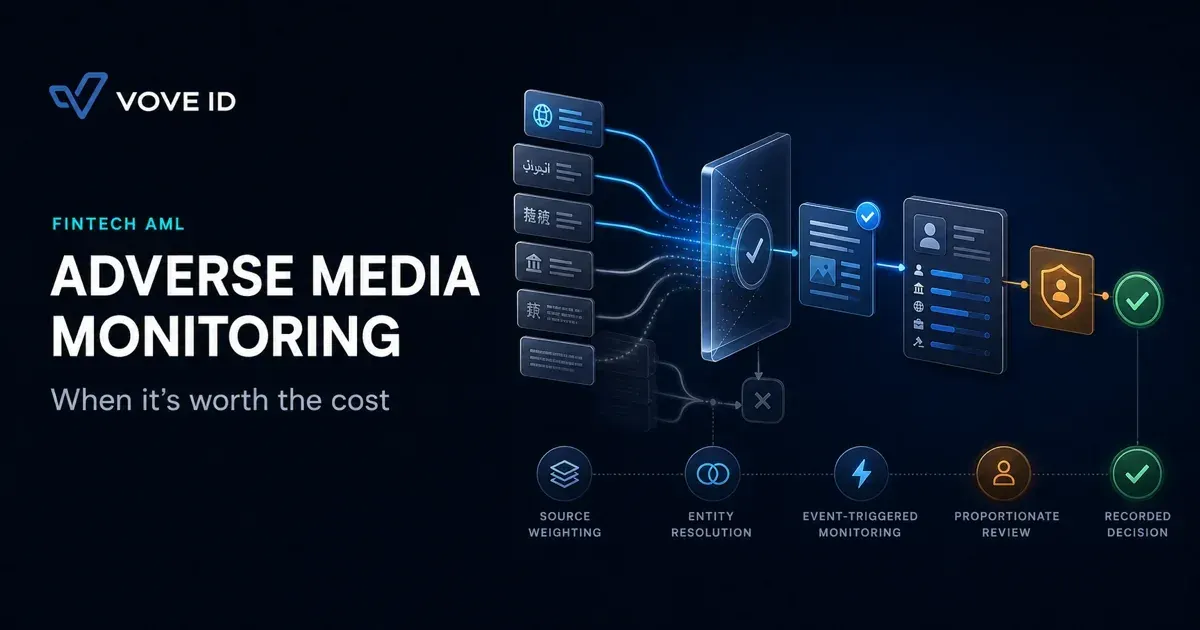

Adverse Media Monitoring for Fintech Startups: When It's Worth the Cost

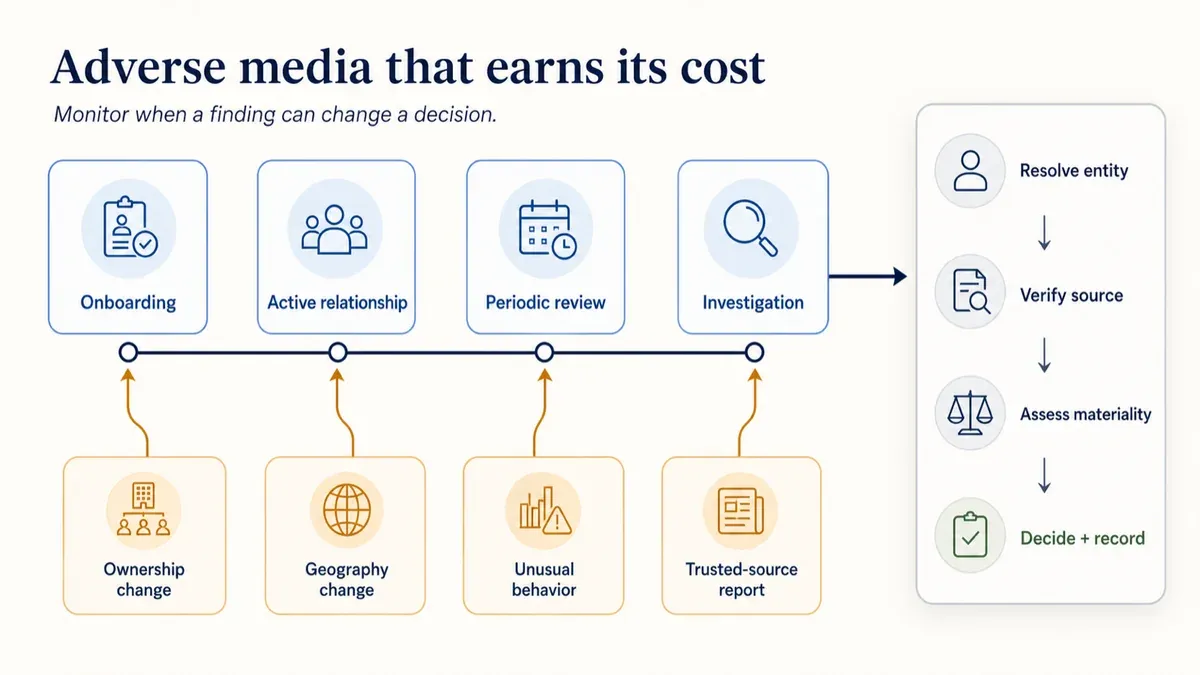

Adverse media isn't a blanket news feed. It earns its cost only at specific trigger points in the customer lifecycle.

VOVE ID helps fintech startups decide where adverse media earns its keep in markets where the signal-to-noise ratio is unforgiving. On paper adverse media is best practice. In practice it is best at specific trigger points.

The short answer

Adverse-media monitoring is worth the cost when it changes a defined decision — onboarding, enhanced due diligence, periodic review, transaction investigation or offboarding. It becomes expensive noise when a team scans everything continuously, cannot distinguish credible allegations from copied content, and has no escalation rule for what it finds.

The right question is not "Should we monitor the news?" It is "Which customers, events and sources can produce evidence material enough to change our risk assessment?"

Where adverse media earns its cost

Adverse media can reveal information that sanctions, PEP and watchlist screening do not yet contain: alleged fraud, corruption, organized-crime links, regulatory action, insolvency, environmental crime or a criminal investigation. It is most useful where that evidence changes the customer's expected risk or explains activity already visible in the account.

The EBA's ML/TF Risk Factors Guidelines place customer due diligence, risk assessment and ongoing monitoring inside one risk-based system. Adverse media should support that system; it should not operate as an unowned alert feed.

For an early-stage fintech, high-value uses usually include:

- high-risk customers, beneficial owners and counterparties;

- cases already escalated for enhanced due diligence;

- material changes in ownership, geography, product use or transaction behavior;

- periodic reviews of higher-risk relationships;

- investigations where public reporting can confirm or challenge an existing hypothesis.

Low-value uses include unlimited searches across every customer, weak keyword matches with no entity resolution, and continuous alerts that nobody can action within a defined service level.

For a full breakdown of ongoing monitoring and risk-based due diligence obligations, see our AML Requirements Explained 2026.

Periodic vs event-driven

Periodic monitoring is predictable. It checks a risk tier on a set cadence and supports scheduled customer reviews. Its weakness is latency: a material event can happen weeks or months before the next review.

Event-driven monitoring runs when something changes. A new director, UBO, country exposure, unusual transaction pattern, law-enforcement request or trusted-source report can trigger a focused search and risk reassessment. Its weakness is orchestration: if identity and customer data are fragmented, the system cannot reliably know whom or what to search.

Most fintechs need a hybrid model:

- At onboarding: search higher-risk customers and controlling persons.

- During the relationship: trigger focused checks after material customer or behavioral changes.

- At review: rerun searches at a cadence proportional to risk.

- During investigation: widen sources and languages when a case hypothesis justifies it.

A realistic adverse media failure: when a sanctioned customer is found through press, not screening

A Latvian fintech learns from a social-media thread that a corporate customer is under indictment in Italy. Its sanctions tool returned nothing because the entity itself had not been designated. The original post is noisy, but it points to reporting by a credible Italian outlet and a public prosecutor's statement.

The compliance team faces two opposite risks. If it dismisses the story because the sanctions screen is clear, it may ignore evidence that materially changes the relationship. If it treats the social post as proven fact, it may take a serious action on unreliable information.

A defensible response preserves the chain:

- resolve the company and relevant people;

- find the originating sources rather than relying on reposts;

- distinguish allegation, investigation, charge, conviction and designation;

- assess relevance to the customer's product use and observed activity;

- escalate, request information or adjust monitoring according to policy;

- record the evidence, decision owner and next review trigger.

The signal came from the press, but the decision comes from corroborated evidence and the firm's risk framework.

How VOVE ID makes adverse media a useful, not noisy, channel

VOVE ID connects adverse-media results to the customer record and the decisions they can affect. Source, publication date, language, entity confidence, allegation type and case outcome are structured rather than buried in screenshots or free text.

That enables teams to:

- weight official and established sources above unverified reposts;

- collapse duplicate and syndicated stories into one event;

- search names and entities across relevant languages and aliases;

- trigger checks from customer and transaction events;

- route high-confidence, material results to a named reviewer;

- retain the rationale for clearing, escalating or reopening a case.

Coverage alone does not create value. The value appears when a result reaches the right case, with enough context to support a proportionate decision.

Adverse-media checklist

- Sources: define source tiers, provenance rules and duplicate handling.

- Triggers: connect searches to onboarding, risk changes, reviews and investigations.

- Escalation: specify materiality, evidence thresholds, owners and response times.

- Support relevant languages, aliases and corporate relationships.

- Separate allegation, investigation, enforcement action, conviction and sanctions designation.

- Measure alerts per customer, duplicate rate, time to decision and cases that changed risk.

- Store the source and the decision trail, including why a result was cleared.

Q&A

Is adverse-media screening mandatory for every customer?

The practical requirement is to maintain effective, risk-based customer due diligence and ongoing monitoring under the rules that apply to the firm. How adverse media contributes should be defined by customer risk, product, geography and the firm's policy — not by a blanket scan with no decision path.

Is social media a reliable adverse-media source?

It can be a lead, but rarely the endpoint. Trace the claim to an original, authoritative or independently credible source before making a material decision.

How often should a startup rerun adverse-media searches?

Use risk-tiered periodic checks plus event-driven triggers. Higher-risk relationships and material changes warrant faster reassessment than low-risk, stable customers.

Conclusion

Adverse media is worth paying for when it changes a defined compliance decision. Source weighting, language coverage, entity resolution and risk-based triggers convert an open-ended news feed into a useful early-warning channel.

Want to see how VOVE ID turns adverse media into signal, not noise? The trigger points that matter are usually already visible in your onboarding and review workflow.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.