Buy Now Pay Later for Travel and High-Ticket: KYC at the Point of Decision

Why a fast BNPL approval on a large basket isn't the same as a defensible one, and what CCD2 requires once the ticket size shifts the risk.

VOVE ID helps high-ticket BNPL providers in markets where the basket size pushes the product into a different compliance regime. On paper it is BNPL. In practice it is consumer credit.

Low-value BNPL flows taught the market to optimize for speed, short forms, and near-instant approval. That muscle memory becomes dangerous when the basket changes from a routine retail purchase to a 4,800 EUR holiday, a premium clinic package, or a multi-thousand-euro electronics bundle. The product may still be labeled BNPL, but the compliance weight starts to look like credit.

That changes the job of onboarding. Identity, affordability, and decision evidence can no longer be treated as separate back-office steps. They need to happen together, at the point of decision, without breaking the checkout experience.

What Changes When The Basket Goes From 50 EUR To 5,000 EUR

At lower ticket sizes, providers often accept thinner evidence because the product economics and regulatory expectations are different. At higher ticket sizes, that tolerance shrinks quickly.

The provider now has to think about:

- stronger identity assurance

- clearer evidence that the applicant is the real borrower

- affordability logic that survives review

- decision records that explain why approval happened in seconds

A team that keeps the same thin-file workflow while simply increasing the basket size usually creates a gap between approval speed and compliance defensibility.

For a full breakdown of identity assurance requirements, see our KYC Requirements Explained 2026.

Affordability At Checkout Speed

Affordability is where many high-ticket BNPL models become fragile. The challenge is not just computing a score. It is producing a decision that can later be explained.

That means the provider needs structured inputs, verified identity, and a documented decision path in the same moment. If affordability relies on sparse self-declared fields, disconnected third-party calls, or a score with no recoverable context, the approval may look fast today and indefensible tomorrow.

Speed still matters. Travel and other high-ticket flows lose conversion when customers are pushed into manual underwriting queues too early. But speed without evidence is not really speed. It is deferred compliance debt.

A Realistic High-Ticket Failure: When An Instant Approval Ends In A CCD2 Audit

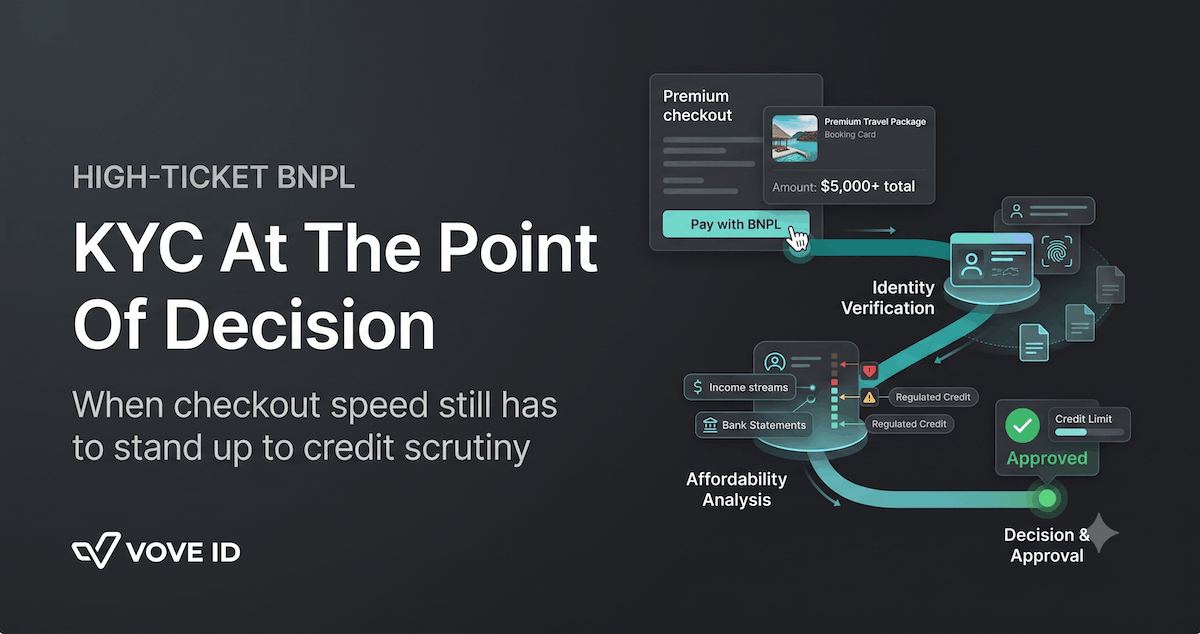

Consider a travel BNPL provider that approves a 4,800 EUR package in seven seconds. The user journey feels polished. The customer verifies basic identity data, receives an approval, and checks out immediately.

Months later, a CCD2-focused review asks how affordability was assessed, which signals were used, and whether the provider can reproduce the decision context for that exact approval. The answer turns out to be a thin-file score and a set of disconnected vendor responses. No one can clearly show how identity assurance, affordability inputs, and the final approval were tied together.

The product did not fail because the approval was fast. It failed because the fast approval was not stored as a defensible credit decision.

How VOVE ID Runs Affordability And Identity In The Same Second

VOVE ID is built for flows where customer experience and credit-grade evidence have to coexist.

Identity checks can run in step with the checkout flow rather than as a separate compliance detour. That helps confirm the borrower and clean the applicant record before affordability logic is applied.

From there, affordability inputs and decision signals can be captured as part of one auditable path. Instead of producing only a yes-or-no outcome, the stack can preserve the evidence that explains the decision later.

For high-ticket BNPL, that matters more than abstract automation. The provider needs a process that remains fast for the customer and legible to compliance teams, partners, and auditors.

High-Ticket BNPL Checklist

- Identity: verify the borrower strongly enough for a credit-weight decision

- Affordability: use decision inputs that can be explained and reproduced later

- Decision: store the approval trail as evidence, not just as a status

Q&A

Why is high-ticket BNPL treated differently from standard checkout BNPL?

Because larger baskets can shift the risk, product expectations, and regulatory scrutiny toward consumer-credit territory even if the front-end label still says BNPL.

Is affordability really possible without slowing checkout too much?

Yes, if identity and affordability are designed as one decision path instead of separate steps stitched together after the fact.

What usually breaks first in a high-ticket BNPL audit?

The missing link between the fast approval and the evidence behind it. Teams often have a score, but not a clean decision record that explains the score.

Conclusion

High-ticket BNPL cannot rely on the same thin-file assumptions that work for low-value checkout finance. Once the basket size carries real credit weight, identity, affordability, and decision evidence have to happen together. The goal is not to slow the flow down. It is to make the fast decision defensible.

Want to see how VOVE ID runs high-ticket BNPL inside the credit regime?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.