Embedded Lending in Marketplaces: Where Compliance Quietly Becomes Your Problem

Why the host-of-record isn't the same as the compliance owner, and what marketplaces running embedded credit need to prove when the lender gets audited.

VOVE ID helps marketplaces with embedded lending in markets where the host-of-record is not the lender-of-record and the regulator still reads both. On paper the lender carries the file. In practice the marketplace runs the relationship.

When a marketplace embeds credit, it usually tells itself a simple story: the licensed lender owns compliance, so the marketplace only needs to focus on conversion. That story rarely survives a real audit. The marketplace owns the merchant relationship, controls the application surface, shapes the data collected at checkout, and often becomes the first place regulators and partners look when something goes wrong.

The result is predictable. Teams launch embedded lending fast, then discover that merchant onboarding, borrower identity capture, consent records, audit handoffs, and exception handling all sit partly on the marketplace side. That is where compliance quietly becomes your problem.

Host Of Record Vs Lender Of Record

The legal structure may say the credit partner originates the loan, underwrites the exposure, and books the product. That matters. But it does not erase the operating role of the marketplace.

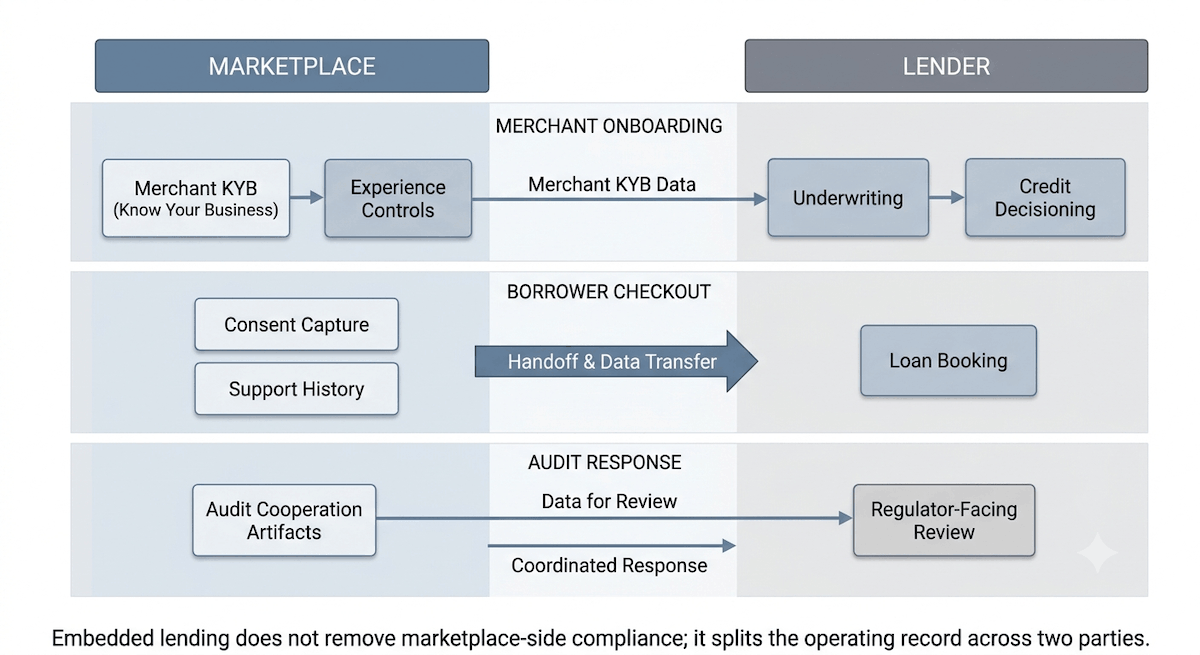

The marketplace often:

- decides which merchants can access the credit flow

- controls the checkout or seller dashboard where the borrower enters data

- passes the application payload into the lender stack

- handles user support when an application is blocked or reviewed

- stores or routes a meaningful share of the evidence trail

That means the marketplace is not a passive referrer. It is part of the operating perimeter. If the lender is audited, investigators will still ask how customer data was gathered, how eligibility was routed, what controls existed around merchant access, and whether the marketplace can reproduce the relevant evidence on time.

Where The Marketplace Inherits Compliance Load

The hidden load usually appears in four places.

First, merchant onboarding. If the marketplace lets sellers surface financing without properly verifying the business, ownership, and risk profile of that merchant, the lender inherits a weak distribution channel.

Second, application integrity. The marketplace may be the system that captures user identity fields, device context, business metadata, or transaction intent before passing them to the lender. Weak capture here becomes weak evidence later.

Third, audit cooperation. When a lender receives a review request, the marketplace may have to provide the seller file, session records, consent proofs, and operational history within strict deadlines.

Fourth, exception handling. False positives, manual reviews, and escalations frequently start in the marketplace workflow, not inside the lender's back office. If those paths are poorly documented, responsibility becomes blurred exactly when documentation matters most.

For a full breakdown of business verification and merchant KYB, see our KYB Requirements Explained 2026.

A Realistic Embedded Failure: When The Lender's Audit Pulls The Marketplace's Data

Imagine a pan-EU marketplace that embeds a credit partner's loan offer for business buyers. The lender is later reviewed on affordability decisions, borrower verification, and seller-level fraud controls. On paper, the lender owns the product. In practice, the lender now needs evidence from the marketplace in three business days.

The marketplace can export merchant profiles but cannot show which onboarding checks were completed at the time financing was enabled. Session logs exist, but the identity payload sent to the lender is not tied to a stable audit trail. Support notes sit in a separate tool. Consent wording changed twice, and no one can prove which version the borrower saw.

Nothing about this failure looks dramatic during launch. It becomes serious only when the lender needs a defensible file and discovers the marketplace cannot reproduce its share of the record cleanly.

How VOVE ID Covers The Marketplace-Side Compliance Work

VOVE ID gives the marketplace its own compliance layer instead of forcing it to rely on assumptions about the partner stack.

That starts with KYB and merchant risk controls before financing is enabled. The marketplace can verify the business, directors, ownership structure, and geography before a merchant ever routes borrowers into a lending flow.

It continues with auditable identity and event capture around the borrower journey. Rather than treating the marketplace as a front-end shell, VOVE ID helps structure the evidence trail so the marketplace can show what was collected, when it was collected, and how it was handed off.

For a full breakdown of individual identity verification and event capture, see our KYC Requirements Explained 2026.

The final piece is audit cooperation. Marketplace-side controls, merchant files, and decision evidence can sit next to the lender relationship instead of living in disconnected tools. That shortens response time when a partner, auditor, or regulator asks for proof.

Marketplace Compliance Checklist For Embedded Lending

- Host: define which entity controls the user journey, data capture, and merchant access

- Lender: map which controls truly sit with the credit partner and which only appear to

- Audit cooperation: make sure the marketplace can reproduce its own evidence trail without the lender rebuilding it manually

Q&A

Isn't embedded lending the lender's compliance responsibility?

The lender owns the licensed credit activity, but the marketplace often owns the merchant, the experience layer, and part of the evidence trail. Regulators and partners will still look at that operating role.

When does a marketplace need KYB in an embedded lending model?

Before merchants are allowed to distribute or benefit from financing. Weak merchant controls upstream create downstream audit and fraud risk for the lender relationship.

Why is audit readiness such a big issue here?

Because embedded models split the operating record across multiple systems. If the marketplace cannot return its share of the file quickly, the lender's compliance position weakens fast.

Conclusion

Embedded lending fails quietly when teams assume the legal booking entity is the same thing as the operating compliance owner. In reality, the marketplace usually carries meaningful responsibility for merchant controls, borrower data quality, and audit cooperation. The safer model is to treat marketplace-side compliance as first-class infrastructure from day one.

Want to see how VOVE ID covers marketplace-side compliance in embedded lending?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.