EMT vs ART: A Compliance Reality Check for EU Stablecoin Startups

Under MiCA, EMT and ART aren't branding choices. They're different legal categories with different issuance paths, reserve logic, and compliance consequences. In May 2026, getting the classification wrong is still one of the most expensive mistakes an EU stablecoin startup can make.

For EU stablecoin startups in May 2026, the most expensive classification mistake is still treating EMT and ART as branding choices. Under MiCA, they are not branding choices. They are different legal categories with different issuance paths, different operating assumptions, and different consequences for onboarding, reserves, redemption, and transaction monitoring.

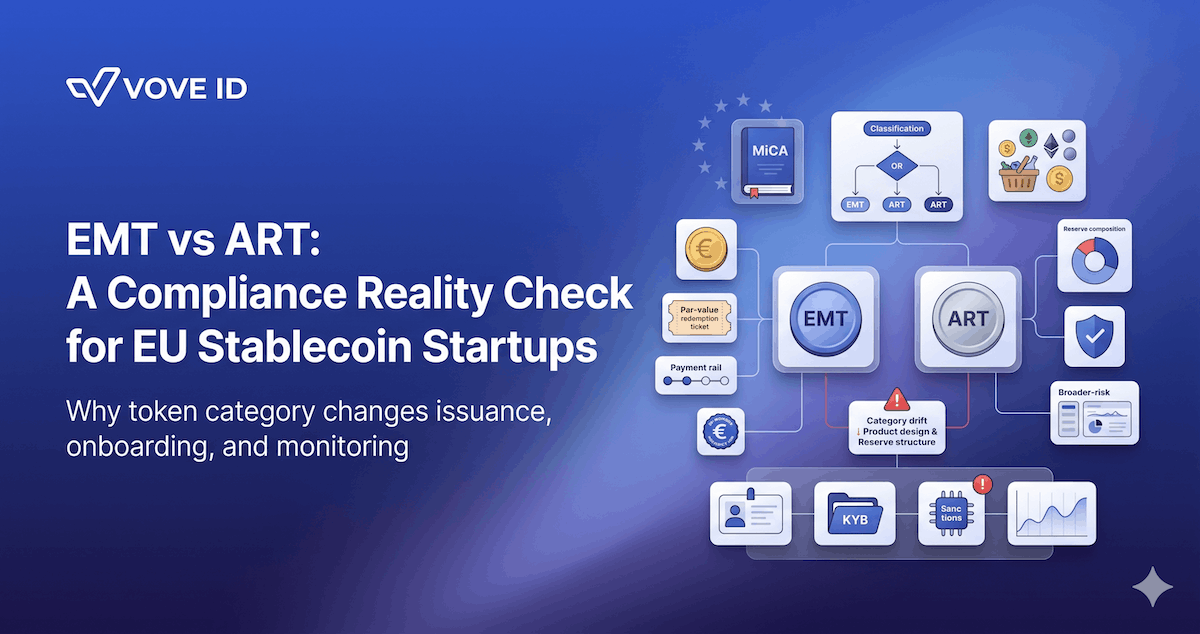

What is the real compliance difference between an EMT and an ART? An EMT is a crypto-asset that aims to keep a stable value by referencing one official currency, and under MiCA it sits close to the electronic-money regime. An ART is a different type of stable-value crypto-asset that references another value, right, or combination, including baskets. In practice that means the token category changes who can issue it, what the reserve logic looks like, how the product is explained to users, and how the compliance stack has to operate day to day.

The hard part is that many founders still talk about category as if it were obvious.

It is not.

The token that looks like "just a stablecoin" in a product meeting can trigger a very different regulatory path once the reference asset, redemption design, payment use case, or reserve structure is examined closely.

That is why the first compliance reality check for an EU stablecoin startup is simple:

if you do not know whether you have built an EMT or an ART, you do not yet know what your operating model needs to be.

Start with the legal definitions, not the marketing story

MiCA is clear about the basic split.

Under Article 3, an asset-referenced token or ART is a type of crypto-asset that is not an EMT and that purports to maintain a stable value by referencing another value or right, or a combination thereof, including one or more official currencies.

An electronic money token or EMT is a type of crypto-asset that purports to maintain a stable value by referencing the value of one official currency.

That sounds like a small distinction.

Operationally, it is not.

The single-currency point is the hinge.

If the token references one official currency, MiCA pulls it toward the electronic-money logic. If the token references a basket, a mix of assets, another right, or a more complex stabilisation structure, the token can move into ART territory instead.

And MiCA is explicit that this is judged by what the token really does, not by what the issuer prefers to call it.

That is why founders get into trouble when they say things like:

- "we are basically an EMT"

- "we call it a euro token, but the reserve has a broader structure"

- "we market it as payments-first, so it should be treated like e-money"

Category follows substance.

The timeline is not future tense anymore

For stablecoin issuers, the relevant MiCA titles have already applied for a long time.

Titles III and IV of MiCA, covering ARTs and EMTs, started applying on 30 June 2024. The broader MiCA framework applied from 30 December 2024.

That means EU stablecoin startups in May 2026 are not in a theory phase.

They are in a classification-and-execution phase.

And while the ESMA statement of 17 April 2026 on the end of MiCA transitional periods focused on CASPs, it reinforces the broader point: the EU supervisory environment now assumes live operating models, not slide-deck readiness.

The operational difference no one explains clearly

Most discussions frame EMT vs ART as a legal memo issue.

The more useful frame is this:

- EMT asks: can you operate something that behaves like tokenised electronic money under EU rules?

- ART asks: can you operate a stable-value crypto-asset with a broader reserve, risk, and governance profile?

That changes everything downstream.

EMT is narrower in reference and heavier in money-like expectations

MiCA treats EMTs as crypto-assets referencing one official currency. It also says issuers of EMTs should be authorised as either credit institutions or electronic money institutions.

That is a major operating signal.

It means the EMT path is not just "the simpler stablecoin path." It is the path that pulls the startup closest to the payments and e-money perimeter.

MiCA also requires issuers of EMTs to issue them at par value on receipt of funds. In other words, the product promise is tighter, more money-like, and less forgiving of fuzzy reserve or redemption design.

ART is broader in reference and heavier in structural risk

The ART path covers tokens whose stable value depends on a broader reference mechanism. That can include:

- one or more official currencies

- other assets

- another value or right

- combinations of those references

That broader structure means the compliance challenge is often less about pure payment logic and more about reserve composition, governance, disclosures, and ongoing prudential control.

ARTs also face a specific restriction when they become heavily used as a means of exchange. Under MiCA, if an ART crosses the threshold of more than 1 million transactions and EUR 200 million in aggregate daily value within a single currency area, the issuer faces additional consequences and restrictions.

That should already tell founders something:

ART and EMT may both be called stablecoins in market conversation, but MiCA does not supervise them as if they were interchangeable.

What the category choice does to onboarding and KYC depth

This is where the legal distinction becomes product reality.

The token category changes what the institution has to understand about the user, the flow, and the risk context.

EMT onboarding is usually closer to payment and redemption logic

If the token behaves like tokenised e-money, the onboarding and monitoring stack needs to support:

- clear identification of users funding and redeeming the token

- strong controls around source of funds where risk warrants it

- transaction patterns consistent with payment-like use

- redemption handling that is operationally tight, not improvisational

- monitoring that can connect the holder, the wallet, and the redemption event cleanly

This is also where the PSD2 overlap matters in 2026.

On 10 June 2025, the EBA published a no-action letter on the interplay between PSD2 and MiCA, warning that some CASPs transacting EMTs may also be carrying out payment services. On 12 February 2026, the EBA followed with an opinion on what national authorities should do after the transition period under that no-action approach ended on 2 March 2026.

The practical implication is not that every startup must panic about dual licensing on day one.

The implication is that EMTs can create payment-services consequences that founders should not discover halfway through launch.

ART onboarding is often more about reserve structure, user understanding, and risk mapping

For ARTs, the onboarding challenge is usually broader.

The firm has to understand not only who the user is, but how the token's stabilisation design affects:

- product disclosures

- reserve expectations

- monitoring of usage patterns

- concentration and redemption risk

- supervisory concern if the token starts being used widely for exchange

That means the KYC stack for an ART issuer is rarely enough if it only verifies identity and stops there.

The startup also needs a compliance record that can explain:

- what the token is actually referencing

- why the customer or counterparty interaction fits the token design

- how reserve and redemption logic line up with the product claim

- what monitoring triggers will show when reality drifts from the original classification assumptions

The biggest founder mistake is assuming category is fixed by intent

This is where many stablecoin startups still get exposed.

They think:

- if the white paper says EMT, the token is EMT

- if the product team says "payments use case," the token is EMT

- if the reserve mostly looks single-currency, the details will not matter

That is the wrong approach.

The European Supervisory Authorities published classification guidelines on 10 December 2024, including a standardised test to support consistent classification under MiCA. The reason is obvious: the market cannot rely on self-labelling alone.

Classification depends on the token's characteristics.

That means founders need to ask harder questions up front:

- what exactly is the token referencing?

- does the stabilisation mechanism rely on one official currency only?

- are there embedded claims or structural features that push the token outside the EMT logic?

- could the reserve or disclosure design create an ART outcome even if the product copy sounds money-like?

Those questions are not abstract.

They decide the build path.

A realistic categorisation failure

Imagine a Berlin startup building a euro-denominated stablecoin for treasury and B2B payments.

The team positions the product as an EMT because:

- the token is marketed in euros

- settlement use cases are payment-focused

- redemption is described as straightforward

Then the structure gets more complicated.

To improve yield and operational resilience, the startup designs a reserve framework that does not sit cleanly on plain euro-funds logic. Product materials begin to describe broader reserve support. Secondary documentation references additional stabilisation features. The treasury and legal teams start talking about flexibility, while the commercial team keeps selling "digital euro cash for businesses."

At that point, the problem is no longer branding.

It is classification drift.

Now the startup faces harder questions:

- Is the token still truly referencing one official currency in the MiCA sense?

- Does the reserve structure still fit the EMT operating model?

- Are the onboarding, redemption, and disclosure flows built for the right category?

- Are transaction monitoring and holder communications aligned with what the token actually is?

This is the failure mode that matters most in 2026.

The token starts as one thing in the founder's mind and becomes another thing in the regulator's file.

What a stronger EU stablecoin stack looks like

A stronger stack starts with one discipline: classify first, build second.

That means the startup should align four layers early.

1. Product design and legal classification

Do not let treasury design, product copy, and legal analysis drift apart.

The token's reference logic, reserve logic, and redemption promise should all point to the same category.

2. Onboarding and user disclosures

The onboarding flow should gather the evidence the operating model actually needs.

For EMT-heavy use cases, that means payment and redemption integrity. For ART-heavy use cases, that often means broader disclosure, reserve transparency, and stronger risk mapping.

3. Monitoring and exception management

The token category should shape what the institution monitors.

If the product promise is tighter, the exceptions should be tighter too. If the token structure is broader, monitoring should be designed to catch drift between the intended classification and the real-world use pattern.

4. Governance and change control

Most category failures do not begin with one bad legal memo.

They begin with small product decisions that slowly mutate the token's actual characteristics. Governance has to catch that before launch or before scale.

How VOVE ID helps teams adapt to the right category

VOVE ID helps EU stablecoin teams build the compliance layer around the token they actually have, not the one they casually describe in fundraising decks.

That matters because classification affects:

- onboarding depth

- wallet and user monitoring

- KYB for business users and counterparties

- sanctions and AML review

- redemption-case evidence

- operational readiness for supervisory questions

For EMT-like products, the stack needs to stay tight around payment flows, holder identity, and redemption control.

For ART-like products, the stack needs to support broader risk context, reserve-linked explanations, and stronger evidence when the product structure is more complex.

The value is not just having KYC or KYB tools.

The value is having workflows that still make sense after the category decision is tested.

Practical checklist for founders

- Write down the exact reference mechanism of the token in one sentence and test whether legal, product, and treasury teams all describe it the same way.

- Check whether the token really references one official currency only, or whether the real structure is broader.

- Review whether the reserve and redemption design fit the claimed category.

- Map where EMT activity could also create PSD2 or payment-services consequences.

- Stress-test whether your onboarding and monitoring flows would still make sense if a supervisor challenged the category.

- Treat any mismatch between white paper language and reserve mechanics as a red flag, not a wording issue.

FAQ

What is the core MiCA definition difference between EMT and ART?

An EMT references the value of one official currency. An ART maintains a stable value by referencing another value or right, or a combination thereof, including one or more official currencies, and is not an EMT.

Why does the distinction matter so much operationally?

Because it changes the issuance path, reserve logic, redemption assumptions, onboarding design, and monitoring requirements. The category is not cosmetic.

Can any startup issue an EMT?

No. MiCA ties EMT issuance to entities authorised as credit institutions or electronic money institutions.

Why is 2026 a key year for this question?

Because the stablecoin-specific MiCA titles have already been in force since 30 June 2024, and by 2026 EU supervisors expect real operating models rather than category theory.

Conclusion

The real compliance difference between EMT and ART is not that one is a "payment stablecoin" and the other is "something more complex."

The real difference is that MiCA expects different institutions, different controls, and different operating evidence depending on which category the token actually falls into.

In May 2026, EU stablecoin startups cannot afford to classify by branding instinct. They have to classify by function, build the onboarding and monitoring stack around that function, and keep governance tight enough to catch category drift before regulators do.

That is the reality check.

Want to see how VOVE ID helps stablecoin teams build onboarding, KYB, and AML workflows that fit the token category they are actually issuing?