Card Issuing for Fintechs: KYC, KYB, and the Cardholder Lifecycle

A card is issued once. The compliance obligation behind it does not end there — it follows the cardholder for years.

VOVE ID helps fintechs that issue cards in markets where card issuance is one step but the compliance obligation lasts for the whole life of the cardholder relationship. On paper, KYC at issuance can look like the main event. In practice, activation, spending, replacement, ownership change, and closure all matter just as much.

Direct answer: Card issuing compliance does not end when the card is created. For retail programs, the obligation follows the customer through activation, usage, and account changes. For business programs, it also follows the company file, beneficial ownership, and delegated card users over time. The issuer that monitors lifecycle events instead of only the issuance event is the issuer that stays ahead of avoidable gaps.

Every lifecycle step is a compliance event

Card programs are often discussed like infrastructure: issue the card, activate it, route the payments, and manage limits. That framing is operationally useful, but it can hide where the compliance workload actually sits.

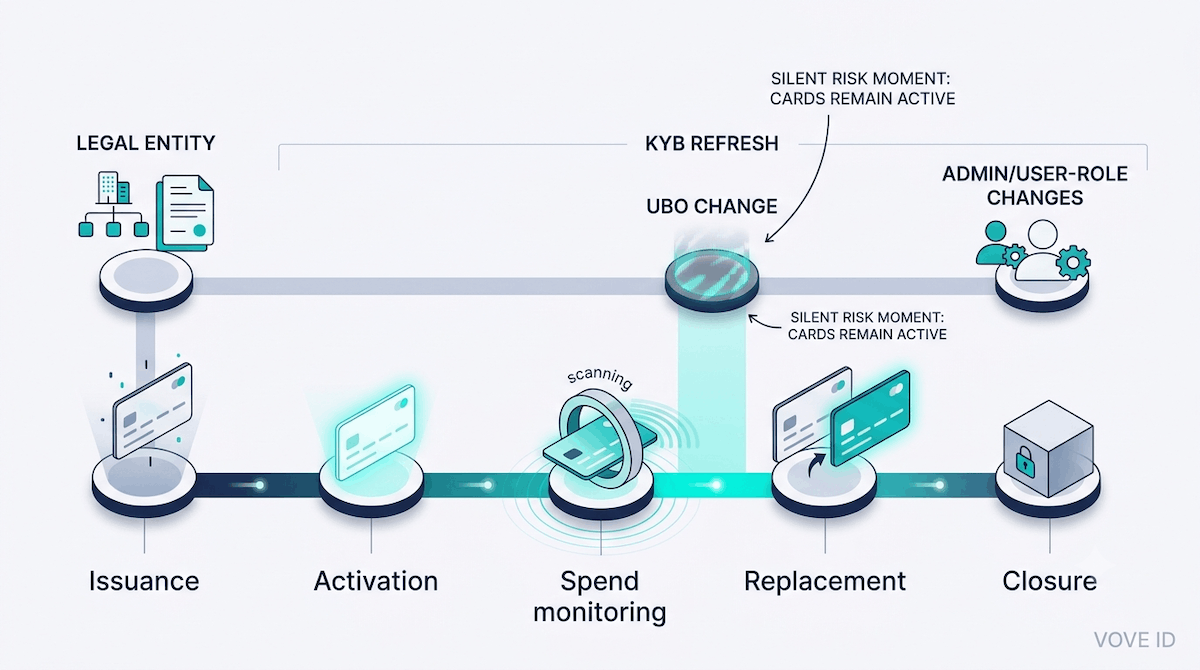

The cardholder lifecycle is not one event. It is a chain of moments that can each change the risk picture:

| Lifecycle moment | Compliance question | Why it matters |

|---|---|---|

| Issuance | Was the customer or business onboarded correctly? | The initial file sets the baseline for all later monitoring |

| Activation | Is the real user the one who should control the card? | Activation confirms the relationship is live, not just approved |

| Ongoing spend | Does transaction behavior still fit the expected use case? | Drift often appears in usage, not at onboarding |

| Replacement or reissue | Why is the card being replaced and who still has access? | Fraud, account takeover, or process weakness can surface here |

| Closure or dormancy | Was the relationship exited cleanly and documented? | Dormant cards and incomplete closure create residual exposure |

That is why card programs break when compliance is organized around a single approval gate. The actual obligation is longitudinal. It has to follow the cardholder over time.

For a full breakdown of identity verification frameworks, see our KYC Requirements Explained 2026.

Why corporate cardholders need a different lens than retail

Retail issuing is usually centered on one person, one identity file, and one main pattern of use. Corporate issuing is different because the cardholder relationship is layered:

- There is a legal entity that must be verified and refreshed.

- There are beneficial owners whose status can change after onboarding.

- There are admins, finance leads, and employee card users with different permissions.

- There may be cards tied to expense policies, travel flows, procurement, or contractor payouts.

A business card program can remain operationally stable while becoming compliance-stale. The company still spends. The cards are still active. But the beneficial ownership may have changed, the finance controller may have left, or the spending pattern may now reflect a different business model than the one originally approved.

That is why corporate issuing needs KYB, KYC, and lifecycle monitoring to sit together rather than in separate systems with separate review clocks.

For a full breakdown of business verification requirements, see our KYB Requirements Explained 2026.

A realistic failure: when a corporate cardholder's UBO changes silently

Imagine a B2B card issuer that onboards an SME cleanly. The company passes KYB, the beneficial owners are captured, and several employee cards are issued for operating expenses. Eighteen months later, the company raises a new round and control changes hands. The cards remain active, spend grows, and nobody refreshes the file.

Nothing about the card rails itself will announce that the beneficial ownership changed. If the compliance program is anchored only to issuance, the account can keep operating on an outdated corporate file long after the original KYB assumptions have expired.

That is the practical failure mode:

- The issuer still has an active card program.

- The customer entity is no longer the same control story it was at onboarding.

- Monitoring is focused on spend anomalies, not ownership drift.

- The next serious review starts from stale KYB evidence.

The gap is not usually a missing card-issuing capability. It is a missing lifecycle trigger.

How VOVE ID covers the cardholder lifecycle from one engine

VOVE ID helps issuers connect the compliance file to the moments that actually change risk.

That means:

- KYC and KYB are captured as the starting point, not the finishing point.

- Lifecycle events such as activation, card replacement, role change, inactivity, and ownership refresh can trigger review logic.

- Corporate-card programs can link legal-entity changes back to active users and active cards.

- Investigators can see the relationship as one compliance timeline instead of separate onboarding, monitoring, and support queues.

For issuers, that matters because the uncomfortable questions usually arrive late. Why was this company still active after control changed? Why was this user still spending after a role change? Why did the replacement event not trigger a closer look? A lifecycle-driven stack answers those questions before they become inspection issues.

Operational checklist for card issuers

- Treat issuance as the start of the compliance timeline, not the end.

- Separate retail and corporate monitoring logic because the risk signals are different.

- Link beneficial-ownership refresh to active corporate card programs.

- Use replacement, role change, and dormancy as review triggers, not just support events.

- Keep one audit trail that ties KYB, KYC, and card lifecycle decisions together.

Q&A

Is KYC at issuance enough for a card program?

No. It is necessary, but it is only the opening control. The real exposure often appears later through usage changes, replacement events, dormant cards, or corporate-file drift.

Why are business card programs more complex than retail card programs?

Because the issuer is supervising both a legal entity and the people spending through it. Ownership, control, permissions, and employee-card access can all change after onboarding.

What is the most common lifecycle gap in business issuing?

One common gap is stale KYB after the business relationship changes in the background. Cards stay active, spend looks normal, but the beneficial ownership or control structure is no longer the same as the approved file.

Conclusion

Card issuing looks simple when viewed as a provisioning problem. It becomes much more exacting when viewed as a compliance relationship that has to stay current for the life of the cardholder. The issuers that tie lifecycle events back into KYC and KYB are the ones that keep the program defensible as it scales.

Is your card program still monitored against the file you approved at onboarding? Corporate card programs rarely fail because KYC or KYB was skipped at issuance — they fail when ownership, roles, or spending patterns drift and nothing catches it. VOVE ID links KYC, KYB, and lifecycle triggers into one audit-ready timeline, so activation, replacement, and ownership changes get reviewed instead of ignored.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.