Multi-Currency Accounts for European Startups: Compliance Beyond the Headline

Adding USD or GBP to a EUR account isn't just an FX feature. It's a new corridor your bank partner will start watching.

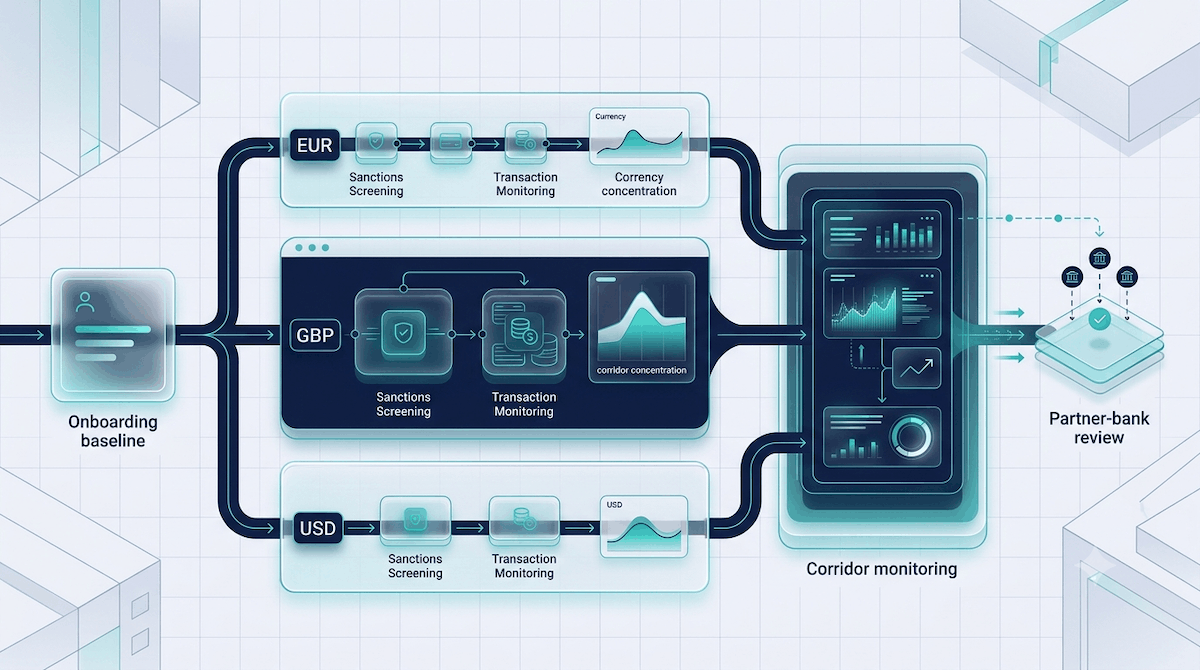

VOVE ID helps fintechs that offer multi-currency accounts to European startups in markets where each added currency creates another compliance surface. On paper, multi-currency is a product feature. In practice, it is a corridor problem, a monitoring problem, and a bank-partner confidence problem at the same time.

Direct answer: Multi-currency accounts are not harder because of the wallet UI. They are harder because every additional currency and payment rail can change sanctions exposure, transaction behavior, safeguarding expectations, and partner-bank scrutiny. The fintech that treats multi-currency as onboarding plus corridor monitoring instead of just account provisioning is the one that scales without triggering avoidable compliance friction.

Why each currency adds a compliance surface

A startup that opens a plain EUR account usually has one main story to tell: who the customer is, where the business operates, and what the expected money flows look like. The moment that same product adds USD and GBP, the account stops being one story.

Now the compliance team has to understand why those currencies are needed, which counterparties are involved, how fast balances turn over, and whether the startup is using the extra rails the way it said it would at onboarding. The account may still belong to one company, but the transaction profile becomes multi-lane.

That is why multi-currency products create more than FX complexity:

- Each rail can bring a different sanctions and screening context.

- The corridor mix can drift far away from the original onboarding narrative.

- One currency can start to dominate volumes and pull the risk profile with it.

- A partner bank may be comfortable with the home-currency business but uneasy about one foreign corridor.

- Monitoring logic that works in aggregate can miss the rail that is actually changing the story.

For a full breakdown of transaction monitoring and sanctions screening requirements, see our AML Requirements Explained 2026.

Where the bank partner watches first

Bank partners rarely begin by questioning the existence of a multi-currency feature. They begin by looking for mismatches between the declared use case and the live corridor mix.

The first questions are usually operational:

- Does the startup's business model justify the extra currencies?

- Are the incoming and outgoing countries consistent with the declared customer base?

- Is one rail growing unusually fast compared with the others?

- Are payment descriptions, counterparties, and transaction timing consistent with payroll, contractor payouts, treasury use, or marketplace settlement?

- Is the fintech able to explain that pattern immediately, with evidence?

| Area | What the bank partner wants to see | What raises concern |

|---|---|---|

| Onboarding narrative | Clear reason for EUR, USD, and GBP usage | Vague "international growth" language with no corridor detail |

| Counterparty profile | Expected countries, merchant types, and business purpose | New geographies or counterparties unrelated to the original file |

| Rail concentration | Balanced or explainable volume distribution | One currency suddenly outgrowing everything else |

| Monitoring evidence | Alerts, thresholds, and documented reviews by rail | One pooled AML view with no corridor-level insight |

| Refresh discipline | Periodic re-checks when usage changes | No trigger when the account behaves differently after launch |

For a full breakdown of business verification and onboarding requirements, see our KYB Requirements Explained 2026.

A realistic multi-currency failure: when the GBP rail outsizes everything else

Consider a Lithuanian EMI serving European startups with EUR, USD, and GBP accounts. At launch, the customer file says the target users are EU software companies that occasionally pay UK contractors. That is easy enough to explain.

Six months later, GBP volume is four times larger than EUR. Most outgoing transfers now cluster around a small set of UK counterparties, and the average balance turns faster than the original risk model assumed. Nothing is necessarily illegal or suspicious on its face, but the live behavior is no longer the story the partner bank originally signed off on.

This is where teams get into trouble. The account was onboarded correctly, but the product was not monitored as a set of distinct corridors. By the time the bank partner asks for a justification, the fintech is trying to rebuild the explanation after the fact:

- Why did GBP become the main rail?

- Was the UK contractor use case always the real one?

- Which alerts should have fired when concentration shifted?

- Did anyone refresh the customer profile when corridor behavior changed?

The issue is not that the fintech offered GBP. The issue is that its compliance stack treated the extra rail as a product toggle instead of an evolving exposure.

How VOVE ID balances the corridor mix for the bank partner

The practical fix is to connect onboarding, monitoring, and review logic around the corridor mix itself.

VOVE ID helps teams do that in four ways:

- It captures the intended currency and corridor story at onboarding, so there is a baseline worth monitoring against.

- It segments activity by rail instead of forcing investigators to infer changes from one blended transaction feed.

- It sets review triggers when a single currency grows faster, turns over faster, or starts attracting a different counterparty pattern than the approved use case.

- It gives the fintech and the bank partner one shared view of the same risk explanation instead of two different dashboards and two different interpretations.

That matters because bank-partner confidence is often the real bottleneck in multi-currency growth. The institution that can explain its corridor mix clearly is easier to support, easier to defend in oversight, and less likely to be slowed down by manual escalations.

Operational checklist for multi-currency accounts

- Capture the expected purpose of each currency at onboarding, not just the list of enabled rails.

- Monitor volumes and counterparties by corridor, not only at customer level.

- Set concentration triggers when one rail grows out of proportion to the original file.

- Refresh the customer profile when corridor behavior changes materially.

- Keep an audit trail that the compliance team and bank partner can review from the same evidence base.

Q&A

Are multi-currency accounts automatically higher risk than single-currency accounts?

Not automatically. They become harder to supervise because the product can hide several different transaction stories inside one customer relationship. The risk rises when the fintech cannot explain the corridor mix clearly.

What usually concerns a bank partner first?

The first concern is usually not the feature itself. It is the mismatch between the original onboarding explanation and the live currency pattern, especially when one rail starts to dominate unexpectedly.

When should a fintech refresh the file on a multi-currency customer?

The file should be refreshed when the main corridors change, when counterparties shift meaningfully, or when one rail begins to drive volumes in a way the original onboarding file did not anticipate.

Conclusion

Multi-currency accounts are easy to market because the customer benefit is obvious. The compliance burden is less visible but just as real. The fintech that treats each new rail as a new monitoring surface, rather than a minor extension of the same account, is the one that keeps growth aligned with partner-bank trust.

Can you explain your corridor mix as clearly as your bank partner needs to? Multi-currency growth stalls when one rail outgrows the onboarding story and nobody catches it first. VOVE ID helps fintechs baseline the intended currency mix at onboarding and flag concentration drift by corridor, not just by customer.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.