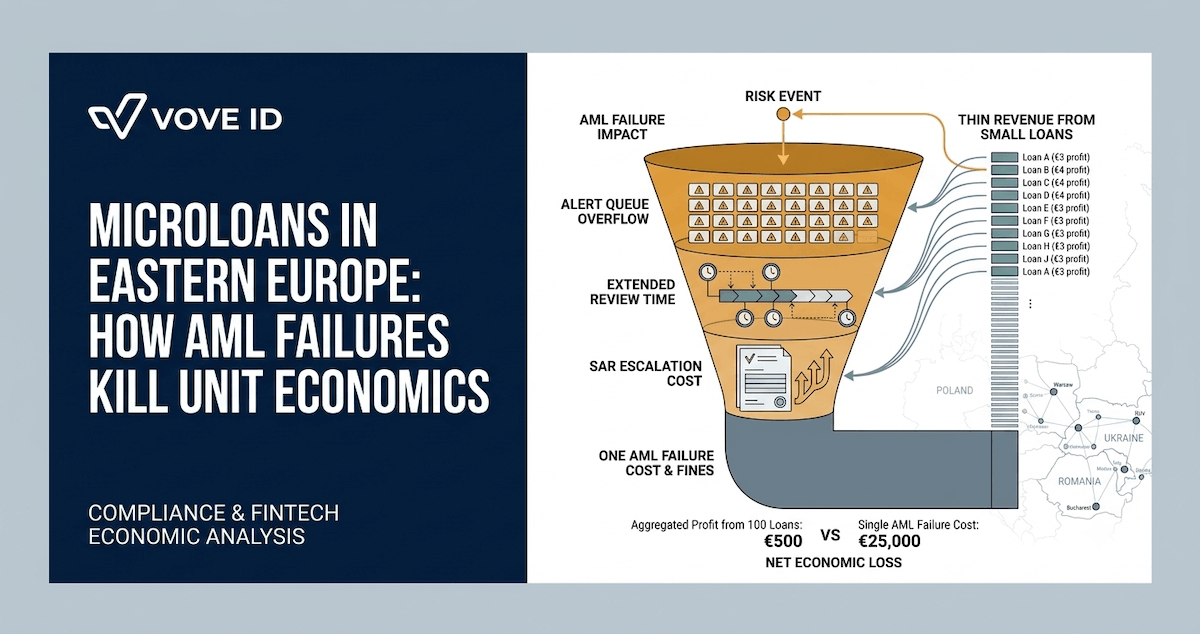

Microloans in Eastern Europe: How AML Failures Kill Unit Economics

Why a single manual AML review can cost more than a microloan's entire margin, and how Eastern European lenders fix tiering, escalation, and case handoffs.

Microloan businesses in Eastern Europe live on thin margins, high velocity, and operational discipline. That is exactly why AML failures are so expensive. A lender can earn money slowly across hundreds of small loans and lose that advantage quickly through a single badly handled case, a delayed review, or a sanctions or SAR workflow that absorbs disproportionate human time.

VOVE ID helps Eastern European microlenders keep AML controls aligned with the economics of small-ticket lending. The point is not to make compliance lighter. The point is to make the control model precise enough that low-risk loans stay fast while higher-risk cases get the depth they actually require.

Direct Answer

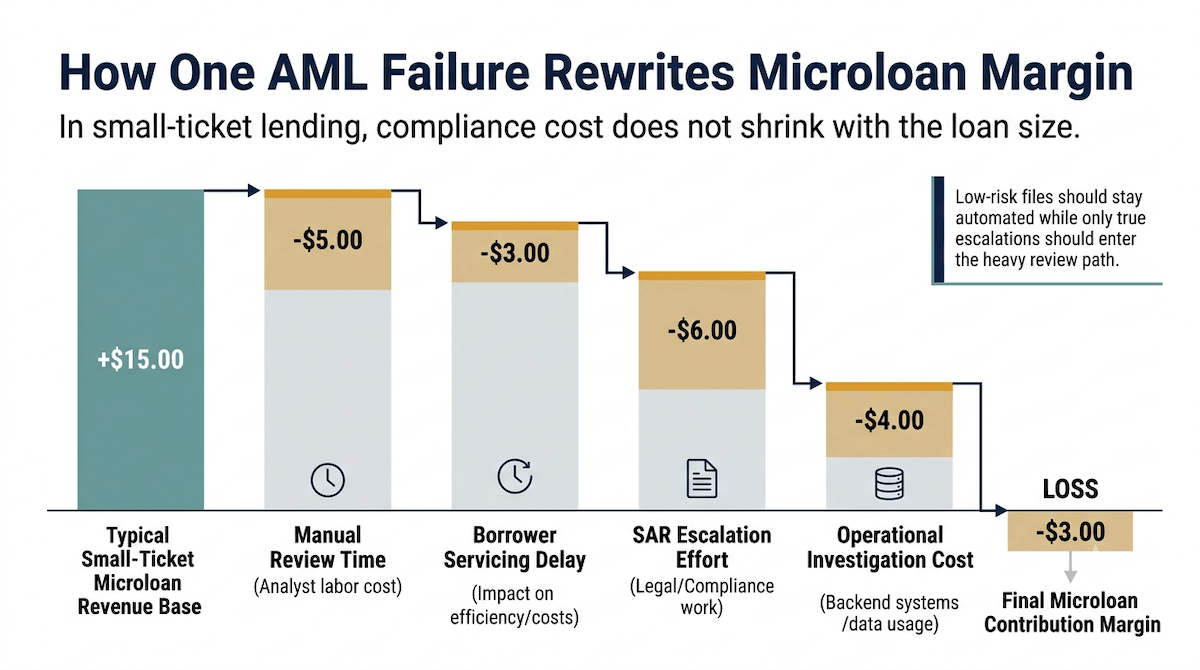

AML failures kill microloan unit economics because compliance cost is mostly fixed while loan revenue is variable and small.

For a lender issuing 300 to 700 EUR loans, one manual escalation can consume days of reviewer time, delay disbursement, frustrate the borrower, and create additional servicing cost that far outweighs the margin on the underlying loan. The lenders that scale are not the ones with weaker AML. They are the ones that run AML with tighter tiering, better case routing, and cleaner evidence.

Why Microloan AML Cost Is Fixed And Revenue Is Variable

That mismatch is the heart of the problem.

The revenue from a microloan is constrained by the ticket size, the term, the local competitive environment, and the borrower risk profile. The compliance workload, however, does not shrink proportionally just because the loan is small. A sanctions hit still needs review. A suspicious pattern still needs investigation. A SAR process still needs evidence, narrative, and operational time.

This creates a structural asymmetry:

- the upside on a single loan is small

- the operational downside of a control failure is large

- the cost of a manual review is often similar whether the loan is 500 EUR or 50,000 EUR

That is why microloan AML cannot just copy the control posture of larger-ticket credit products. It has to be designed for scale, triage, and reviewer efficiency from the start.

For a full breakdown of sanctions screening, SAR/STR obligations, and transaction monitoring requirements, see our AML Requirements Explained 2026.

The Three Failures That Hit Unit Economics Hardest

1. Over-reviewing low-risk borrowers

Many lenders start with an AML rule set that treats too many cases as exceptional. That creates queues, slows approvals, and pushes experienced reviewers into work that should have been automated or tightly scoped.

The visible problem is delay. The underlying problem is cost distortion. If the queue keeps expanding, the lender is effectively paying enterprise-review costs on small-ticket products.

2. Poorly scoped SAR escalation

A SAR process should be serious, but it should also be narrow. When a case is escalated without good event framing, reviewers spend too long collecting context, duplicating earlier work, or investigating noise that never should have entered the queue.

That is expensive in any lending model. In microloans, it can erase the economics of a whole cohort.

3. Broken handoff between onboarding and ongoing monitoring

Microloan failures often happen because onboarding made one decision and monitoring later raises another signal with no operational bridge between them. The team then has to reconstruct who the borrower was, what was known at onboarding, why the original decision was made, and whether the new signal changes the risk posture.

When that reconstruction happens manually, time expands, servicing cost rises, and the file becomes harder to defend.

A Realistic Eastern European Failure Pattern

Consider a Polish microlender issuing 500 EUR loans. The pricing model assumes high throughput and a mostly automated decision path. A borrower is flagged through a suspicious activity pattern shortly after application. The signal is real enough to justify a pause, but the queue is poorly tiered, so the case sits with other ambiguous alerts for days.

By the time the reviewer reaches it, the lender has already spent time on servicing, customer communication, and internal investigation. The borrower experience has deteriorated, the loan timing is broken, and the operational cost of the file now exceeds the likely profit from the loan itself.

Nothing about that loss is theoretical. It comes from three ordinary failures working together:

- the alert threshold was too blunt

- the review queue was not prioritized well

- the case evidence was not organized for fast decisioning

That is how a small AML miss becomes a unit-economics problem instead of just a compliance problem.

What Good AML Looks Like In Microloans

Strong AML in microloans is not a heavier version of enterprise banking. It is a more selective and more disciplined version of it.

The right operating model usually includes:

- risk tiering that keeps straightforward files automatic

- alert logic that distinguishes noise from real escalation signals

- reviewer queues based on urgency and exposure

- a unified case file linking onboarding, screening, and monitoring

- audit evidence that can be reconstructed without operational archaeology

The theme is precision. The lender does not win by cutting controls. The lender wins by applying the right control depth to the right loan at the right moment.

How VOVE ID Protects Unit Economics

VOVE ID helps microlenders keep compliance cost proportional to the product.

Instead of pushing every exception into the same manual path, the platform supports tiered decisioning, clearer escalation logic, and a more connected audit trail between onboarding and monitoring. That lets low-risk files stay fast while genuine AML events receive focused attention with less duplication.

For microloan businesses, that has three direct effects:

- reviewer time is spent on truly material cases

- disbursement friction drops for the majority of borrowers

- the business can defend its AML posture without turning every alert into a margin event

The result is not weaker oversight. It is a control design that respects the economic reality of small-ticket lending.

Checklist: Microloan AML Controls That Protect Margin

- Can low-risk borrowers pass without unnecessary manual review?

- Are SAR and sanctions escalations tightly scoped?

- Can reviewers see onboarding and monitoring context in one file?

- Is queue priority based on risk and exposure rather than arrival order?

- Can the team reconstruct an AML decision without manual stitching?

If the answer to several of these is no, the lender is probably losing margin through process design rather than credit quality.

Q&A

Why are AML failures especially painful in microloans?

Because loan revenue is small while compliance review cost is relatively fixed. A manual case can consume more value than the loan is expected to generate.

Does tighter AML always slow down microloan approvals?

No. Weakly designed AML slows approvals. Well-tiered AML speeds up the majority path and reserves manual review for genuinely higher-risk cases.

What is the most common operating mistake?

Treating every alert as if it deserves the same review depth. That overloads teams and distorts economics.

What should lenders measure first?

Measure reviewer time per escalated file, approval delay caused by AML alerts, and the percentage of alerts that produce no meaningful risk outcome. Those figures expose where margin is leaking.

Conclusion

In Eastern European microloans, AML is not just a compliance obligation. It is a unit-economics variable. The lenders that scale are the ones that can keep high-risk signals serious without forcing every small loan into an expensive manual process.

Ready to see how VOVE ID can connect onboarding, screening, and monitoring into one decision model that protects your margin?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.