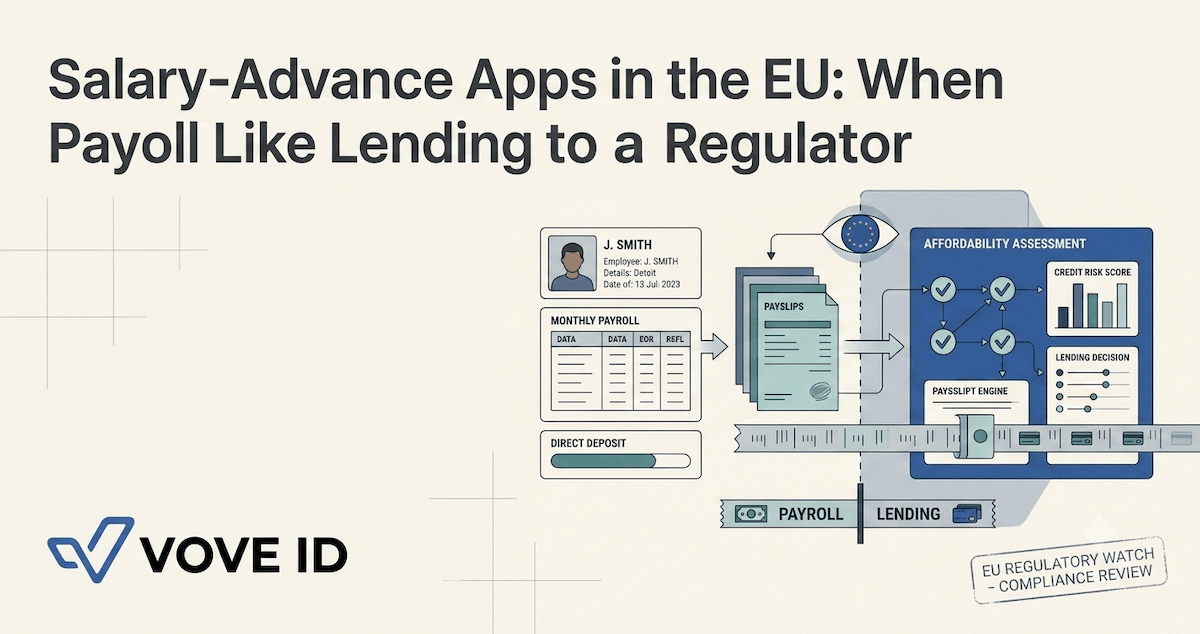

Salary-Advance Apps in the EU: When Payroll Looks Like Lending to a Regulator

Why earned-wage access products can't rely on the payroll label alone, and what affordability, disclosure, and audit trails CCD2 actually requires.

VOVE ID helps salary-advance startups in markets where the regulator decides what the product is. On paper it is payroll. In practice the NCA reads CCD2.

Salary-advance products still get sold internally as a payroll feature: a smoother HR benefit, a retention lever, a short-term employee experience tool. That framing is useful for marketing, but it does not settle the regulatory question. Across the EU, the harder question is whether the advance behaves like consumer credit in the moments that matter to a regulator.

The problem for product teams is not only that the answer can vary by market. It is that the answer can vary by supervisory reading, by product structure, and by the control evidence available when the file is reviewed. A team that ships with payroll logic only may discover too late that it needs affordability checks, disclosures, and decision logs that look much closer to lending infrastructure than HR software.

Salary advance: payroll, credit, or both

Most salary-advance products sit in an uncomfortable middle zone. The user experience feels payroll-native: an employee accesses earned wages early, often through an employer-linked workflow. But a regulator does not stop at the user interface. The regulatory reading follows the substance of the arrangement: how funds are advanced, when repayment happens, what fees are charged, what risk sits on the provider, and what expectations exist if repayment fails.

That is why the same product can be described internally as an earned-wage tool and externally reviewed as a credit-like product. If the supervisory lens moves toward consumer credit, the operating model changes with it. Teams need to show who was onboarded, what checks were applied, when a decision was made, and why a given advance moved through the system without manual intervention.

For salary-advance apps, the real risk is not uncertainty by itself. The risk is building a stack that only works under one legal reading and has no room to adapt when the regulator applies another.

For a full breakdown of the identity verification layer this onboarding sits on, see our KYC Requirements Explained 2026.

The CCD2 reading and what it changes

CCD2 raises the practical stakes because it broadens the perimeter around products that previously lived in a lighter-touch zone. For salary-advance apps, that means the safe assumption is no longer "we are adjacent to payroll, so credit rules are someone else's problem." The safer assumption is that at least some advances may need to withstand a credit-grade review.

When that happens, three requirements show up fast. First, affordability becomes material. It is no longer enough to know the user is attached to an employer or has a recurring payslip pattern. The team needs a documented approach to deciding whether the advance is appropriate. Second, disclosure requirements become operational. Product copy, terms, and event timing all need to align with what the regulator expects the user to have seen before the advance is granted. Third, the audit trail becomes a frontline control rather than a back-office convenience.

The teams that struggle most are the ones that treat these as legal add-ons. They are not. They affect workflow design, fallback paths, exception handling, reviewer queues, and what data must be available in one place when an audit arrives.

A realistic salary-advance failure: when the audit treats every advance as a credit event

Consider a French salary-advance app expanding quickly through employer partnerships. The product was designed as a payroll experience, so onboarding is optimized for speed: identity is verified lightly, employer linkage is the main trust signal, and the system assumes the payroll relationship explains the risk profile.

Then a review lands with a harder question: show how each advance was assessed, what evidence supported the decision, what disclosures were delivered, and how exceptions were handled. The team can show activity logs and payment records, but it cannot show a structured affordability assessment or a durable credit-style decision trail. Worse, the answer differs across operations, risk, and product because no single workflow owns the full decision.

That failure is expensive even before any enforcement outcome. Engineering gets pulled into reconstruction work. Compliance teams start manual sampling. Product changes freeze while the team decides which advances need a stricter path. What looked like a payroll UX problem becomes an operating model problem.

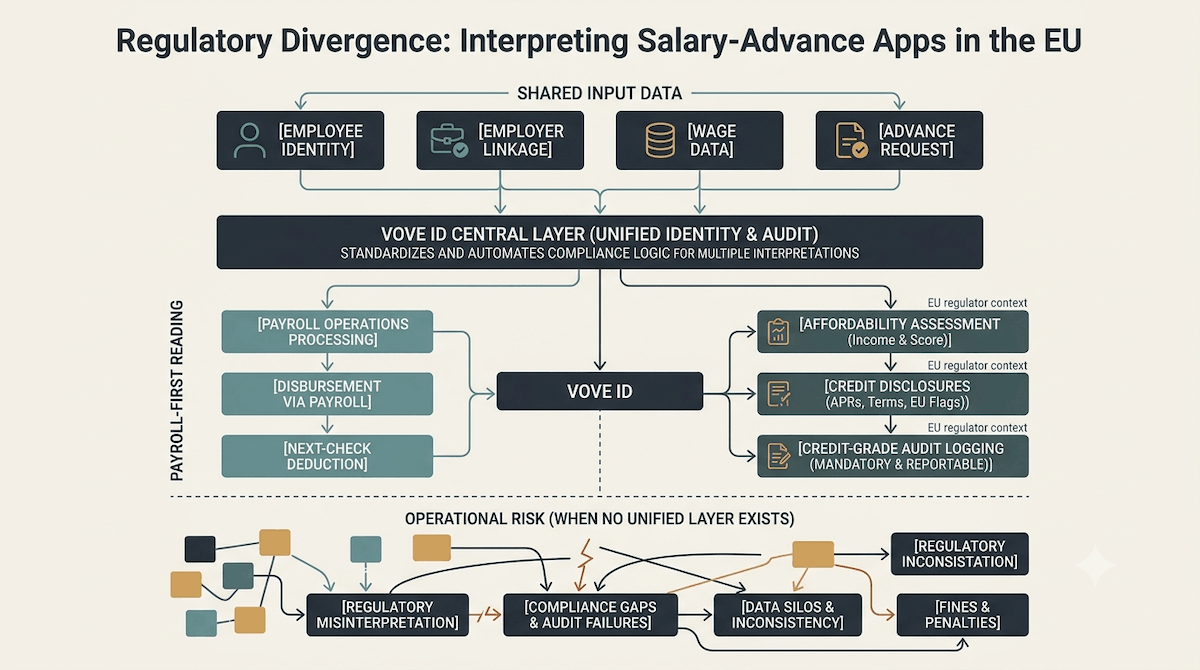

How VOVE ID covers both the payroll and the credit reading

VOVE ID gives salary-advance teams a way to operate under both interpretations without duplicating the whole stack. Identity checks, affordability logic, and audit evidence can be orchestrated inside one onboarding and decision flow, with stricter controls triggered only where the product structure or jurisdiction requires them.

That matters because most teams do not need every advance treated the same way. They need a system that can distinguish between lower-risk cases and the advances that need stronger evidence. Instead of bolting credit controls onto payroll operations later, VOVE ID lets the team define when affordability is required, when disclosures must be logged, and how reviewer intervention should be captured.

The result is a product that still feels operationally light where it can, but is defensible where it has to be. That is the real requirement for salary-advance apps now: not choosing between payroll and credit, but being able to survive both readings.

Checklist

- Identity verification mapped to the employer-linked flow

- Affordability logic triggered where the product or market requires it

- Audit logs that show the decision path for every reviewed advance

Q&A

Is every salary-advance product automatically treated as consumer credit?

No. The point is not that every product gets the same answer. The point is that salary-advance teams cannot rely on the payroll label alone. The supervisory reading depends on product design, fees, repayment structure, and local interpretation.

Why is CCD2 such a problem for salary-advance teams?

Because it narrows the room for light-touch assumptions. Products that previously operated with a payroll-first mindset may need to prove affordability, disclosures, and decision evidence in a much more explicit way.

What usually breaks first when the regulator reads salary advance as credit?

The audit trail. Many teams can show payment activity and basic onboarding data, but not a coherent record of how the advance decision was made and what controls were applied.

Conclusion

Salary advance is one of the clearest examples of a product category where regulatory meaning can outrun product language. If the app is built only as payroll, the team gets exposed the moment a regulator reads it as credit. The operational answer is not to guess which interpretation will win, but to build a workflow that can handle both.

Want to see how VOVE ID covers the dual-read of salary advance?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.