From Sole Trader to GmbH: Why the Same Workflow Doesn't Cover Both

One SME onboarding workflow trying to cover both sole traders and incorporated entities will over-collect for one path and under-check the other. Here's why.

Most SME onboarding friction is not a document problem first. It is a classification problem. In 2026, teams still lose good applicants because the workflow treats a sole trader and an incorporated company as if they generate the same compliance file. They do not.

VOVE ID helps fintechs onboard sole traders and incorporated SMEs in markets where a single workflow is doing both jobs badly. This guide covers how entity class changes the verification logic and where shared flows break. For the underlying KYB framework, see our KYB Requirements Explained 2026.

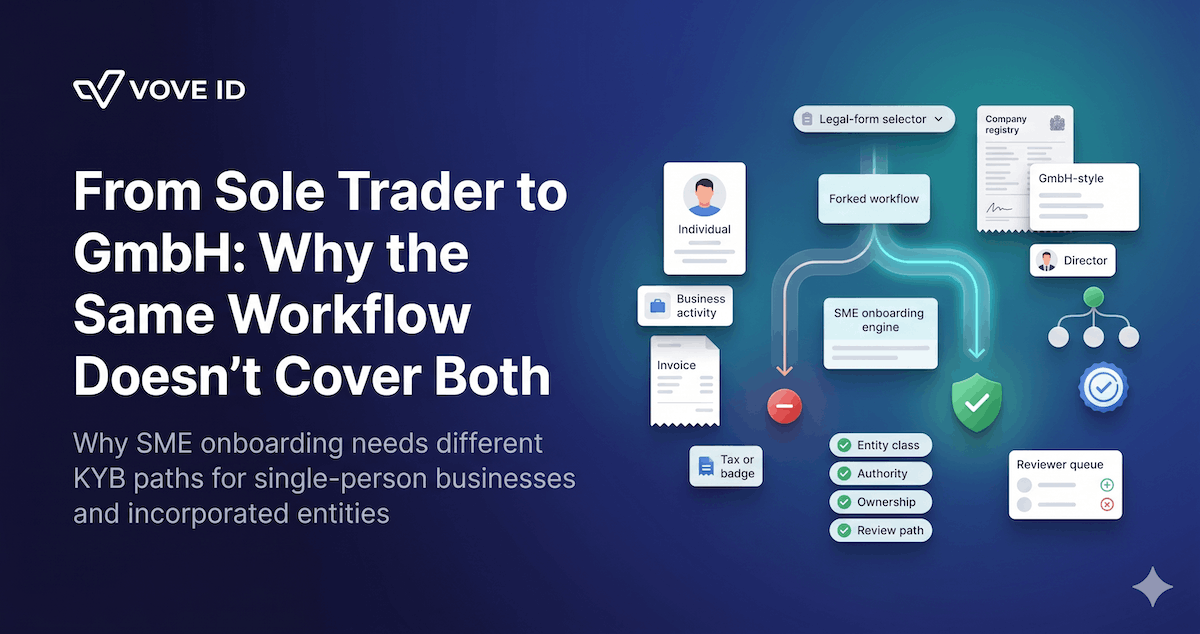

Why can't one SME onboarding workflow cover both sole traders and GmbHs? Because a sole trader and a GmbH create different KYB questions. A sole trader usually collapses business identity and personal identity into one person, while a GmbH adds a separate legal-entity layer, representation rules, and beneficial-ownership logic. When one workflow tries to cover both without branching early, it over-collects for one path and under-checks the other.

On paper a single SME flow looks simpler. In practice it costs conversion and compliance both.

Sole trader vs incorporated SME: what is actually different

The mistake usually starts with language.

Teams say "SME" as if it were one customer type. It is not. It is a commercial segment that contains multiple legal forms, and those legal forms change what the file must prove.

For a sole trader, the business often sits much closer to the human being behind it. The onboarding file still needs to establish legitimacy, activity, and risk. But the legal separation between person and business is thinner, and beneficial-ownership logic is often irrelevant or much lighter.

For a GmbH, the file has to answer a different set of questions:

- Does the legal entity exist in the claimed form?

- Who has authority to act for it?

- Who ultimately owns or controls it?

- Do directors, signatories, and owners align with the relationship being requested?

A workflow that asks every SME the same questions will almost always ask the wrong amount for at least one path.

Where one flow under-checks and where it over-checks

When teams force both entity classes through one path, the problems show up in two directions at once.

It over-checks the sole trader

The sole trader gets pushed into fields that make sense only for a more layered legal structure:

- beneficial-owner declarations that do not fit the reality

- board or director questions that do not apply cleanly

- corporate-document requests built for incorporated entities

That creates avoidable drop-off. The applicant is not refusing to comply. The applicant is being asked to explain a structure they do not have.

It under-checks the incorporated SME

At the same time, the GmbH or equivalent incorporated entity may pass through a path that focuses too heavily on the individual operator and not enough on the legal entity and control layer.

That leaves gaps around:

- representation authority

- shareholder or beneficial-owner mapping

- sanctions screening on relevant control parties

- evidence that the business relationship actually fits the entity being onboarded

The workflow ends up too heavy where it should be light and too light where it should be structured.

The legal form changes the risk model

This is not only a UX issue. It is a risk-model issue.

A sole trader often creates concentration risk around one natural person. The identity, business purpose, bank-account logic, and operating activity can all converge on the same individual.

An incorporated SME creates a different challenge. The file may involve a legal entity, one or more directors, a beneficial owner, a trading name, and an operating reality that does not map neatly to the registry extract on the first pass.

That is why KYB for incorporated entities usually needs stronger logic around entity verification, ownership and control, signatory authority, and change monitoring after onboarding. The workflow should reflect those differences early. If it does not, reviewers end up rebuilding them manually later.

A realistic flow failure: when a Spanish autónomo cannot pass a German GmbH path

A pan-EU marketplace opens onboarding for SMEs across several countries. The workflow was originally built around incorporated entities because the first launch market focused on German GmbH applicants. Then Spanish autónomos start applying.

The applicant reaches a beneficial-owner step that assumes a corporate structure. The form asks for ownership percentages, director records, and company-document logic that does not fit the applicant's legal form.

Then the inconsistencies appear:

- the applicant uploads an individual tax or business-activity record

- the workflow expects a corporate registration extract

- the ownership step implies multiple layers of control that do not exist

- the reviewer cannot tell whether the applicant is incomplete or simply misclassified

The case stalls. Nothing is inherently wrong with the customer. The path is wrong. This is not a verification failure. It is a workflow-classification failure.

The first decision should be entity class, not document type

Many teams branch too late. They start collecting documents before deciding what kind of entity is actually applying.

The classification should happen near the start of the flow. Once the entity class is known, the workflow can change cleanly:

- sole traders move into identity, business-activity, and operating-purpose checks that fit their structure

- incorporated SMEs move into entity, authority, and ownership checks that fit theirs

The key is not to create two entirely separate products. The key is to fork the logic at the right gate.

How VOVE ID forks the workflow at the right gate

VOVE ID helps fintech teams turn legal-form differences into routing logic instead of reviewer confusion. That usually means four things.

Entity-class detection happens early. The workflow identifies whether the applicant is a sole trader or an incorporated entity before the heavy collection logic begins.

The collection path changes with the entity class. Sole traders are not asked to navigate a GmbH-style ownership path. Incorporated SMEs are not allowed to skip the entity-and-control steps that actually matter.

Authority and control stay visible in one file. For incorporated applicants, the workflow keeps entity evidence, signatory logic, and beneficial-owner questions inside one case record instead of scattering them across reviewer notes.

Review is reserved for real mismatches. The human queue should focus on unresolved edge cases, not on customers who were routed into the wrong path at step three. That is how teams recover both conversion and control quality.

Practical KYB checklist

Entity class

- Determine the legal form before requesting full evidence.

- Route sole traders and incorporated SMEs into different logic paths early.

Path

- Remove beneficial-owner steps that do not apply to sole traders.

- Add authority and ownership checks where the entity class requires them.

Conversion

- Track drop-off by legal form, not only by country or channel.

- Review whether queue backlogs are caused by real risk or wrong-path routing.

Q&A

Why do sole traders need a different onboarding flow from incorporated SMEs?

Because the compliance questions are not the same. A sole trader often ties business activity closely to one natural person, while an incorporated entity creates an additional legal and control layer that must be verified separately.

Does a sole trader still require business verification?

Yes. The file still needs to establish legitimate activity, intended use, and risk. The difference is that the workflow should not force a sole trader into corporate-ownership questions that do not match the legal form.

What is the main risk of using one shared SME flow?

The main risk is that the workflow becomes inaccurate in both directions. It creates unnecessary friction for simpler entities and leaves control gaps for layered ones.

Where should the workflow split happen?

As early as the team can determine entity class reliably. If the split happens after document upload or manual review, the workflow is branching too late.

Conclusion

SME onboarding is not one path with a few local variations. It is a set of entity classes that need different verification logic.

Teams that treat a sole trader like a GmbH lose conversion. Teams that treat a GmbH like a sole trader lose control. The practical answer is not more manual review. It is earlier classification and cleaner routing. Entity class, path design, and case logic are one workflow.

Running SME onboarding across multiple markets and entity types? VOVE ID routes sole traders and incorporated SMEs into the right verification path from the first step — so the workflow collects what matters and skips what does not.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.