UBO Verification Across the EU: When Registries Don't Agree

One registry answer is not a complete UBO answer. Cross-border ownership chains, partial registries, and conflicting records are now standard operating conditions for EU KYB.

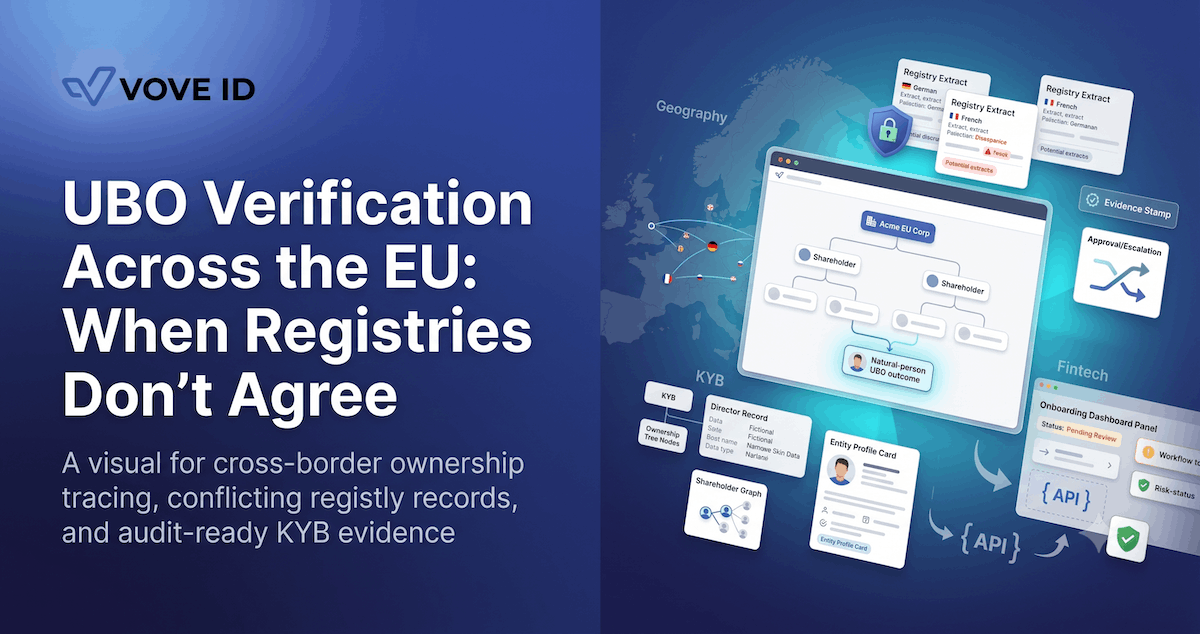

UBO verification across the EU breaks down when teams treat one registry answer as a complete answer. In 2026, the harder problem is not finding a company — it is reconciling ownership, control, and evidence across sources that update at different rates, expose different fields, and often stop at the edge of a local jurisdiction.

VOVE ID helps fintechs verify UBOs in markets where the public registry is gated, partial, or out of date.

On paper, UBO verification looks like a registry lookup. In practice, it is an evidence exercise. This is exactly where KYB slows down.

This guide covers the structural reasons EU registries disagree, where the ownership-vs-control distinction matters most, and what a defensible cross-border UBO workflow looks like. For the underlying KYB framework, see our KYB Requirements Explained 2026.

The registry answer is only the first layer

Most teams start in the right place. They pull the company record, confirm legal existence, review directors, and look for shareholder information. That establishes the entity. It does not always establish the beneficial owner.

The UBO question starts when the simple record stops being simple.

If the direct shareholder is another company, the file is not finished. If a registry shows a current director but not the real control chain, the file is not finished. If one source shows a natural person and another shows an intermediate holdco, the file is not finished.

UBO verification is not about finding one answer quickly. It is about reaching the most defensible answer with enough evidence behind it.

Why registries disagree across the EU

The disagreement is usually structural.

One registry updates faster than another. One source exposes direct ownership but not indirect control. One country shows broader shareholder data than another. One source reflects a filing that another has not yet processed. One source stops at the domestic entity while the control chain continues abroad.

This is where false confidence becomes the real risk. A clean local record can make the file look complete even when the control chain leaves the jurisdiction two layers up.

The problem is sharpest when the case involves cross-border SMEs, holding-company structures, nominee or administrative layers, or higher-risk sectors that require deeper explanation.

Why the hardest part is control, not paperwork

A company can be easy to document and still hard to understand. That happens when the legal paperwork answers one question and the operational control picture answers another.

The compliance team may receive a registry extract, an articles document, a shareholder chart, and a board list. Those documents may all be valid. They may still leave open the questions that matter most: who ultimately controls the entity? Who should be screened as a UBO or controller? Which evidence supports that conclusion?

This is where many KYB programs become inconsistent. Two reviewers can read the same pack and reach two different conclusions because the process never defined how to resolve conflicting ownership signals.

A realistic UBO failure: when two sources tell two different stories

A Dutch fintech onboards a Belgian SME for a cross-border payments product.

The first source shows one natural-person UBO. The second source suggests there are two controlling individuals through an intermediate company. The customer sends a shareholder chart by email. The chart conflicts with one of the registry records.

One reviewer wants to approve because the entity is real and active. Another wants escalation because the ownership picture is not consistent. Commercial pressure builds because the customer wants to go live before payroll week.

What failed here is not entity verification. It is the inability to turn multiple sources into one clear, evidence-backed ownership conclusion. That is the real UBO bottleneck.

What strong cross-border UBO verification looks like

Good UBO verification across the EU is a workflow, not a lookup.

Start with entity verification, then branch fast. Confirm legal existence first. Then determine immediately whether the ownership chain is simple, layered, or cross-border. If it is layered, the workflow should escalate early rather than treating the domestic record as sufficient.

Separate ownership from control. The file should not assume that the visible shareholder list tells the whole story. It should test whether control sits with direct shareholders, indirect shareholders, directors with effective control, founders acting through holding structures, or other controlling persons the documents reveal.

Reconcile primary and secondary sources. When two sources differ, the answer is not to pick whichever one appeared first. The team needs a consistent resolution path: record what each source says, identify what is current versus historical, request targeted evidence for the gap, and capture why the final conclusion was accepted.

Screen the real control perimeter. Entity-only screening is too thin for most SME and B2B onboarding cases. Once the control picture is clear enough, screening should cover the people and entities that actually shape the risk decision.

Preserve the evidence trail. The final conclusion should survive later review. The case file should show the sources consulted, the ownership logic used, any unresolved points, the reviewer decision, and the reason the customer was approved, escalated, or declined.

Why manual UBO work fails at scale

Manual UBO work looks manageable until volume rises. Then the invisible cost appears: analysts spend hours stitching sources together, onboarding times stop being predictable, commercial teams stop trusting compliance timelines, refresh work gets skipped, and decision quality varies by reviewer.

This is why UBO verification becomes one of the slowest parts of KYB for SME lending, B2B payments, marketplaces, embedded finance, and higher-value counterparties. The issue is not only time — it is inconsistency. When every complex case depends on reviewer memory, the business cannot scale the workflow cleanly.

How VOVE ID resolves UBO across primary and secondary sources

VOVE ID helps teams turn UBO verification into a structured decision flow rather than a document chase. That includes entity verification across relevant company sources, branching logic for layered and cross-border ownership, UBO and controller mapping, screening across the real control perimeter, and one audit-ready case record with evidence and decision history.

The goal is not to retrieve data faster. It is to make the ownership conclusion explainable when a bank, partner, auditor, or regulator asks why the file was approved.

Practical UBO verification checklist

Collection

- Capture the legal entity identifier and jurisdiction first

- Request an ownership chart when the chain is not obviously direct

- Ask for targeted evidence only where public sources stop being clear

Verification

- Confirm whether ownership and control point to the same natural person

- Reconcile conflicting registry and secondary-source results before approval

- Escalate early when the chain leaves the domestic jurisdiction

Screening

- Screen UBOs, directors, and other real controllers

- Extend review to linked parent entities where they shape the risk

- Treat entity-only screening as incomplete for layered structures

Evidence

- Record which sources were used and when they were checked

- Save the reasoning behind the final UBO conclusion

- Build a file that can be reopened months later without guesswork

Q&A

Why is UBO verification harder than ordinary company verification?

Company verification proves that an entity exists. UBO verification has to explain who ultimately owns or controls it — which often requires more than one source and more than one jurisdiction.

What should a fintech do when two registries disagree?

It should not approve on whichever source appeared first. The team should compare the records, request targeted evidence for the gap, and document why the final conclusion is still defensible.

Is one national company registry enough for EU UBO verification?

For a simple domestic structure, sometimes yes. For layered or cross-border SMEs, no — the local registry often establishes the entity but not the full control chain.

What is the real operational risk of weak UBO verification?

Weak UBO work affects more than KYB speed. It weakens sanctions review, EDD decisions, monitoring context, and the ability to defend the relationship under later scrutiny.

Conclusion

UBO verification across the EU is a reconciliation task, not a registry lookup. Teams need a workflow that moves from entity existence to control, from control to screening, and from screening to an evidence trail that holds up under review. Cross-border ownership, partial registries, and conflicting records are not edge cases — they are normal operating conditions.

The workflow stops breaking down when ownership, control, screening, and evidence run as one process rather than four separate steps.

Cross-border UBO verification is one part of a broader KYB problem. VOVE ID helps teams operating across EU jurisdictions build a workflow where ownership decisions are traceable and the case file stays defensible — even when the registry picture is incomplete at the start.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.