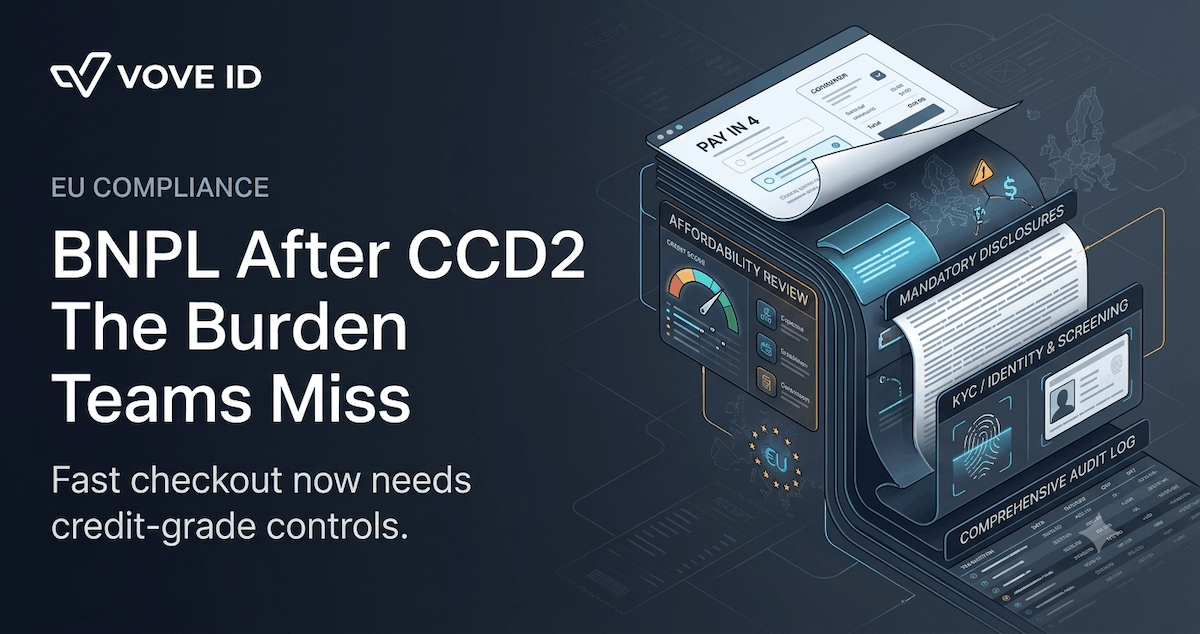

BNPL in the EU After CCD2: The Compliance Burden Most Teams Underestimate

The checkout can stay lightweight after CCD2. The affordability and disclosure evidence behind it cannot.

VOVE ID helps BNPL providers operate like credit businesses in a market that increasingly expects them to behave like credit businesses. That is the real shift after CCD2: the checkout experience may still feel lightweight, but the compliance burden does not.

Direct answer: after CCD2, BNPL teams can no longer assume that a fast checkout exempts them from credit-grade onboarding, affordability thinking, disclosure controls, and defensible audit evidence. If the product extends consumer credit in substance, regulators will expect the onboarding stack to prove it was treated that way.

For years, many BNPL operators were built around a product assumption that speed was the moat and friction was the enemy. The checkout had to feel invisible. The risk stack could sit in the background, and the compliance file was often thinner than what a traditional lender would tolerate.

CCD2 changes the direction of travel. Even where local implementation details still vary across Member States, the policy signal is clear: BNPL cannot keep relying on the idea that installment credit offered at checkout is operationally closer to payments than to lending.

That matters because many BNPL teams are still running a 2023 operating model in a 2026 regulatory environment.

What CCD2 Actually Does to BNPL

The practical impact of CCD2 is not just that more products fall under closer consumer-credit scrutiny. It is that the product, compliance, and operations teams have to stop pretending short-duration credit is exempt from credit discipline.

For BNPL providers, that means at least four things:

- the onboarding flow has to capture enough data to support a legitimate lending decision

- disclosures have to be structured, timely, and demonstrable

- affordability cannot be hand-waved away as a generic risk score

- the audit trail has to show what the customer saw, what the system checked, and why the decision was made

This is where many teams underestimate the burden. They assume CCD2 is mainly a legal-text problem. In practice it is a workflow problem. If affordability, disclosures, and evidence capture are not built into the product path itself, the business ends up trying to retrofit compliance around a checkout that was designed to avoid friction at all costs.

Affordability and Pre-Contractual Disclosures

BNPL teams often separate commercial UX from compliance UX. That separation becomes expensive once the regulator asks where affordability was assessed and what the customer was shown before entering the agreement.

Affordability is not the same thing as saying "the amount is small" or "defaults are low." It is the ability to show the inputs, thresholds, and decisioning logic that supported the extension of credit. The exact design can vary by product and jurisdiction, but the compliance expectation is simple: the lender should be able to explain the decision as a decision, not as a black-box conversion optimization output.

Pre-contractual disclosures matter for the same reason. A checkout can be elegant and still fail if the operator cannot prove the customer received the right information at the right time, in the right sequence, and in a recoverable format.

That is the real burden most teams underestimate. They think CCD2 adds more policy. In reality, it forces operational proof.

A Realistic BNPL Failure

Take a Spanish BNPL provider with one million users and a highly optimized merchant checkout flow. The product works. Approval rates are strong. Merchant conversion is the core KPI, and every extra field in the flow is treated as a threat to growth.

The firm carries that same onboarding architecture into the post-CCD2 environment. At review time, the regulator asks three simple questions:

- How was affordability assessed?

- What information did the customer receive before taking the credit?

- Can the firm reproduce the exact decision path for a sampled transaction?

The team has partial answers to all three. The risk engine has scores, but not a clean explanation layer. The disclosure copy exists, but evidence of delivery is inconsistent across merchants and devices. The borrower journey is fast, but the audit trail is fragmented across front-end events, PSP logs, and vendor systems.

Nothing in that scenario requires fraud, misconduct, or a broken business. It only requires a team that optimized for conversion before it optimized for control.

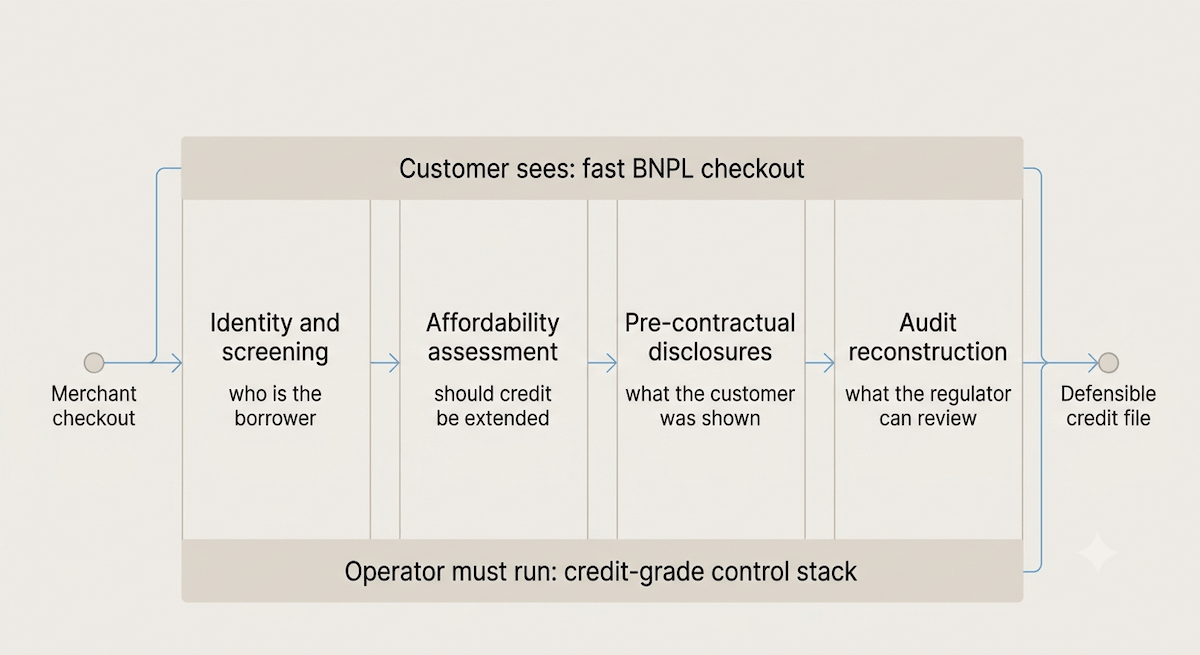

How VOVE ID Turns BNPL Onboarding Into Credit-Grade Onboarding

VOVE ID helps BNPL teams keep the checkout fast while making the underlying control system more defensible. That matters because BNPL operators do not need a slower product. They need a better-structured product.

The right stack brings four layers into one journey:

1. Identity and screening

Customer identity, sanctions screening, PEP screening, and fraud checks sit at the start of the flow with clean event logs and decision timestamps.

For a full breakdown of identity verification requirements, see our KYC Requirements Explained 2026.

2. Affordability logic

The platform captures and stores the signals that support a lending decision, then ties them to a clear pass, fail, or review state.

3. Disclosure evidence

The system records what disclosure content was served, when it was shown, and how it aligned to the specific transaction or agreement path.

4. Audit reconstruction

The provider can rebuild the full decision file without piecing together screenshots, PSP exports, and manual reviewer notes after the fact.

That is what changes BNPL compliance from reactive legal clean-up to built-in operational control.

Why the Existing Checkout Usually Fails

Most BNPL stacks were built around a payment mindset:

- approve quickly

- hide friction

- maximize merchant conversion

- investigate only when something breaks

CCD2 pushes the operating model toward a credit mindset:

- assess the borrower, not just the transaction

- prove what was disclosed before commitment

- show why the decision was appropriate

- preserve evidence in a way a regulator can actually review

The product can still feel fast. But the underlying system now has to behave like lending infrastructure.

Checklist for BNPL Teams in 2026

- Affordability: Can the team explain the decision inputs and thresholds for a sampled transaction?

- Disclosure: Can the business prove what the customer saw before taking the credit?

- Audit: Can one case file reconstruct the full user journey and approval logic?

- Exceptions: Are manual reviews structured, timestamped, and governed?

- Merchant variation: Do all merchant integrations preserve the same evidence quality?

Q&A

Does CCD2 mean every BNPL flow has to look like a bank application?

No. The customer experience can still be short and well-designed. The real requirement is that the control system behind it can support a defensible credit decision and disclosure record.

What do BNPL teams usually underestimate first?

Affordability evidence. Many teams have risk scoring, but they do not have a clean explanation layer that shows how the extension of credit was justified.

Is checkout speed now incompatible with compliance?

No. Speed and compliance only conflict when the stack was built without structured evidence capture. A well-designed flow can stay fast while still producing a complete decision file.

Why is merchant variation such a problem?

Because disclosure timing, UI rendering, and event capture often differ across checkout environments. A provider may think it has one product while actually operating multiple evidence models.

Conclusion

The post-CCD2 problem for BNPL is not that the model stops working. It is that the model can no longer run on lightweight assumptions about affordability, disclosures, and auditability.

BNPL providers that adapt early will keep the product speed merchants want while building the credit-grade operating discipline regulators expect. The rest will discover too late that a clean checkout is not the same thing as a defensible lending workflow.

Could your team reproduce the exact decision path for a sampled BNPL transaction today? Most providers have risk scores but not a clean explanation layer, and disclosure copy without proof it was actually delivered. VOVE ID ties identity, affordability, and disclosure evidence into one reconstructable decision file, without slowing the checkout down.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.