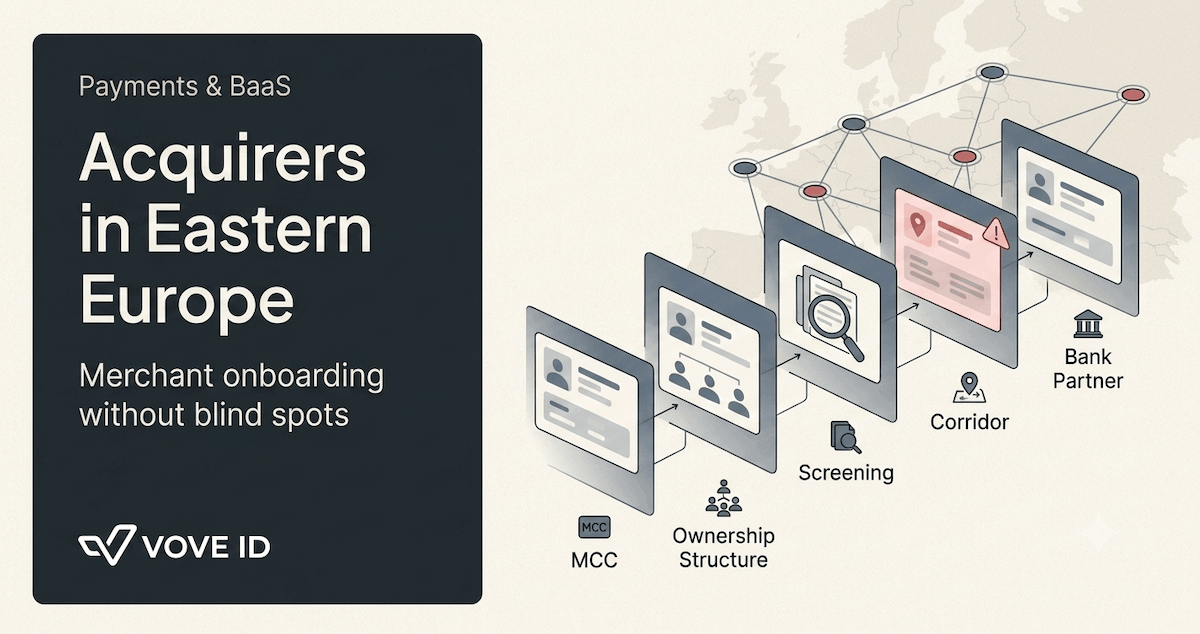

Acquirers in Eastern Europe: Onboarding Merchants Without Drowning in Risk

A clean registry extract and a plausible MCC code are the start of merchant risk review, not the end of it.

VOVE ID helps Eastern European acquirers onboard merchants in markets where the merchant base is fragmented, the documentation stack is inconsistent, and the risk model cannot rely on home-market assumptions. The hard part is not saying yes or no to a merchant. The hard part is proving, at onboarding, that the merchant is real, controlled by the people they claim, and operating inside a risk envelope your bank partners and card schemes can actually accept.

Direct answer: Eastern European acquirers avoid drowning in merchant risk by making onboarding an enrichment workflow, not a form-checking exercise. The winning stack combines merchant category review, beneficial ownership verification, registry lookups, sanctions and PEP screening, and market-specific risk overrides before the first transaction is processed.

What makes Eastern European acquiring different

Merchant acquiring in Eastern Europe is attractive for the same reason it is difficult: the region offers fast-growing merchant demand across ecommerce, digital services, marketplaces, cross-border sellers, and gray-zone verticals that look ordinary until you inspect them closely. A merchant that appears low-risk in a generic onboarding flow can carry a very different profile once you factor in local registry quality, nominee structures, adjacent high-risk activity, and scheme scrutiny.

That creates a problem for acquirers expanding from a Western European home market. On paper, the merchant onboarding flow looks transferable. In practice, the data coverage, document consistency, and enforcement pattern are different enough that a copied risk model becomes a blind spot.

The first operational mistake many acquirers make is treating merchant onboarding as a pure KYC problem. It is not. Merchant onboarding is a combined KYB, UBO, sanctions, fraud, and portfolio-concentration problem. The second mistake is over-trusting merchant-declared data such as website category, processing expectations, and beneficial ownership. In Eastern Europe, those fields are often the beginning of the review, not the end.

Six merchant attributes the home data does not return

A strong Eastern European merchant onboarding flow should surface six attributes early.

The first is the real business activity behind the declared MCC. Many merchants are technically registered under one activity while monetizing under another. If the acquiring decision only reads the declared category, the acquirer can miss exposure to high-risk segments such as speculative trading affiliates, lead-generation funnels for prohibited products, or disguised subscription businesses.

The second is the ownership and control structure. A registry extract alone does not tell you whether the named shareholders are the true controlling parties, whether control has shifted recently, or whether a sanctioned or politically exposed person sits one layer behind the visible entity. UBO mapping has to go beyond the top-level filing.

The third is the jurisdictional pattern of the merchant's revenue. A merchant incorporated in Romania may process mostly UK or CIS traffic. A Polish merchant may settle from one entity while marketing through another. When corridor exposure and entity structure do not line up, the onboarding file needs an explanation before the first scheme review asks for one.

The fourth is the operational footprint. A merchant that claims low-risk services but has no genuine local team, support process, fulfillment logic, or dispute-handling workflow should not be scored like a straightforward domestic seller. Operational thinness is often the clue that the declared model is incomplete.

The fifth is the adverse signal environment around the merchant and its controllers. That includes sanctions, PEPs, adverse media, regulatory mentions, related entities, and prior payment relationships. A merchant can be technically registrable and still unacceptable to a cautious acquiring program.

The sixth is the merchant's dependence on volatile processing spikes. In fragmented merchant segments, volume growth is not automatically good news. Rapid transaction expansion, especially into one corridor or one card mix, often changes the risk classification faster than the original onboarding file anticipated.

For a full breakdown of business verification and beneficial ownership requirements, see our KYB Requirements Explained 2026.

A realistic acquiring failure: when a high-risk merchant slips through MCC scoring alone

Imagine a Romanian acquirer onboarding roughly 400 merchants each month. The team has a clean application flow, basic KYB checks, and automated MCC scoring. One new merchant presents as a software-services company selling analytics subscriptions to small businesses across the EU. The incorporation documents check out. The shareholders are visible. The website is polished. The processing forecast seems plausible.

Three months later, card-scheme monitoring flags abnormal dispute patterns and elevated cross-border refund friction. A deeper review shows that the merchant's traffic mix is adjacent to a CFD lead-generation network, the real control sits with a beneficial owner omitted from the first-layer review, and the public-facing activity understates the merchant's actual risk profile. The acquirer now has to defend why the file passed in the first place.

That failure is rarely caused by a missing form field. It is usually caused by a model that trusted the declared MCC, treated registry data as conclusive, and skipped market-specific enrichment. Once the merchant is live, the acquirer is no longer reviewing a prospect. It is managing scheme exposure, bank-partner questions, reserves, and remediation timelines.

How VOVE ID enriches merchant onboarding with EE-native data

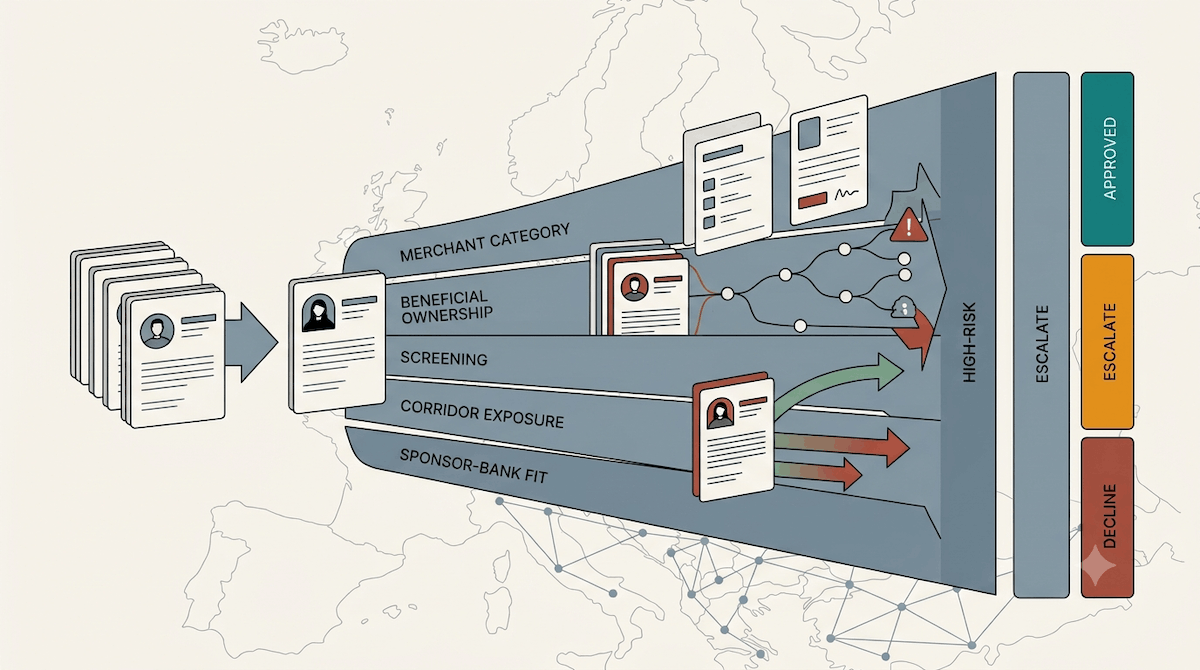

VOVE ID helps acquirers make Eastern European merchant onboarding defensible before scheme pressure arrives. The practical advantage is not just faster verification. It is layered evidence.

At the entity layer, the flow verifies registration data, directors, and business existence against the relevant corporate record. At the control layer, it maps beneficial ownership and screens the human parties who actually control the merchant. At the risk layer, it overlays sanctions, PEP, and adverse-signal checks on the entity and its controllers. At the operating layer, it lets the acquirer structure review rules around corridor concentration, expected merchant behavior, and category-specific escalation paths.

That matters because Eastern European acquiring is not won by approving more merchants blindly or by rejecting half the pipeline defensively. It is won by routing the right merchants into the right review depth. Low-risk domestic sellers can move quickly. Borderline files can be escalated with a documented rationale. High-risk or poorly evidenced merchants can be declined before they distort the portfolio.

For acquirers working with sponsor banks or scheme-facing oversight teams, this also improves explainability. A file with MCC review, ownership evidence, screening results, and market-specific enrichment is easier to defend than a file that says the merchant passed automated onboarding.

For a full breakdown of sanctions and PEP screening requirements, see our AML Requirements Explained 2026.

Merchant onboarding checklist for Eastern European acquirers

Before approving a merchant, an acquirer should be able to answer five basic questions clearly.

Is the declared business model consistent with the real merchant activity?

Do the entity, directors, and beneficial owners line up across filings, supporting documents, and digital footprint?

Does the geographic revenue pattern match the stated business model and risk appetite?

Have sanctions, PEP, adverse media, and related-entity checks been completed on both the company and controlling individuals?

Would this file still make sense if a card scheme or sponsor bank asked for the supporting logic ninety days from now?

If the answer to any of those questions is no, the onboarding file is not finished yet.

Q&A

Why is merchant onboarding in Eastern Europe riskier than a copied EU flow suggests?

Because the challenge is not only regulation. It is fragmented data quality, more variable merchant structures, and a higher chance that declared merchant activity does not capture the real risk profile.

Is MCC scoring enough to approve merchants at scale?

No. MCC is one signal, not a complete risk model. Acquirers need ownership checks, screening, and market-specific enrichment to avoid approving merchants that only look low-risk at the category level.

What does a strong acquiring onboarding stack need?

It needs KYB, director and UBO verification, sanctions and PEP screening, adverse-signal review, and workflow rules that adapt by merchant type and corridor exposure.

Conclusion

Eastern European acquiring rewards teams that can price and manage complexity, not teams that assume the home-market model will stretch cleanly across the region. Merchant onboarding has to do more than collect documents. It has to explain who the merchant is, how the merchant makes money, who controls it, and why the portfolio can live with the risk.

Acquirers that build this logic into onboarding avoid the worst trade-off in the business: approving merchants too loosely and discovering the real profile only after the schemes, sponsor bank, or disputes team finds it first.

Would your last approved merchant file still hold up if a card scheme asked for the logic behind it today? Merchant onboarding built around a registry extract and an MCC code misses the ownership, corridor, and adverse-signal layers that actually drive risk. VOVE ID layers entity, ownership, and screening checks into one onboarding flow built for Eastern European merchant data.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.