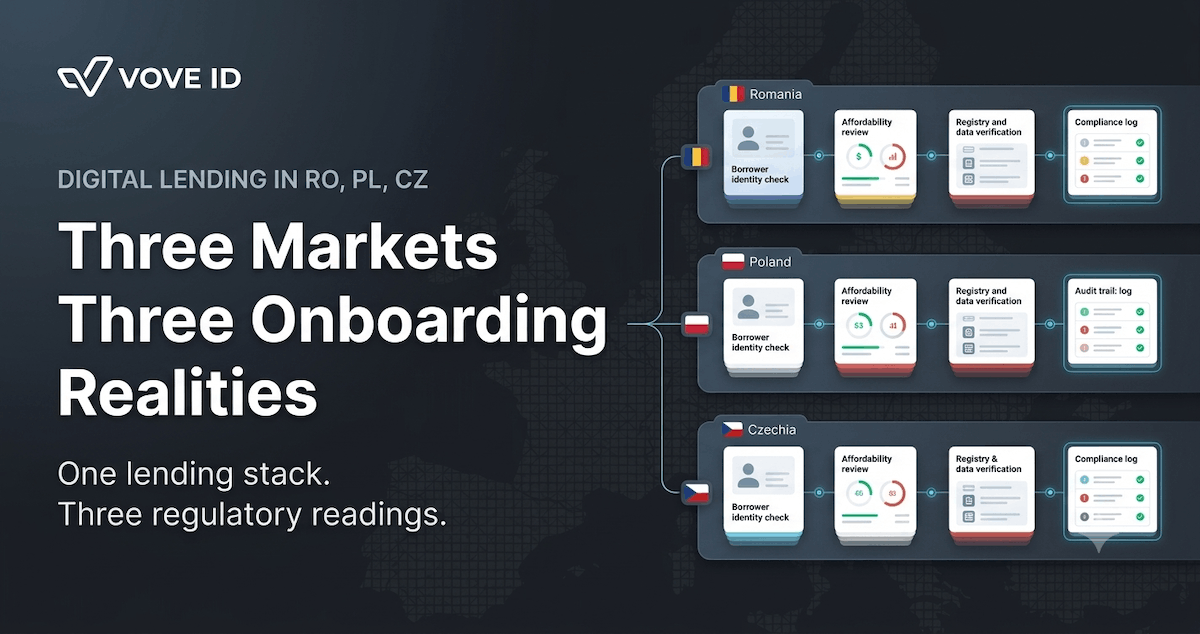

Digital Lending in Romania, Poland, Czechia: Three Markets, Three Onboarding Realities

BNR, KNF, and CNB ask the same questions about a borrower in a different order, with different proof.

VOVE ID helps embedded lenders launch across Romania, Poland, and Czechia without pretending the three markets can share one untouched onboarding stack. The regional opportunity is real, but the operational reality is three different supervisory readings of identity, affordability, and local data.

Direct answer: a lender can reuse its core decisioning engine across RO, PL, and CZ, but it cannot reuse the same onboarding logic without local adaptations. The winning stack keeps one product experience while swapping country-level checks, disclosures, and audit evidence behind the scenes.

Romania, Poland, and Czechia are often grouped together in expansion plans because the borrower profile looks familiar: urban digital demand, rising embedded-finance distribution, and investors looking for scalable loan books. That grouping is useful for market sizing, but it breaks down fast at onboarding. The moment a lender moves from growth deck to go-live checklist, each country asks a different first question.

Romania tends to force the team back into the operational basics: identity quality, traceable onboarding evidence, and confidence that the lender can explain the file after origination. Poland pushes hard on affordability discipline and local data expectations. Czechia usually exposes whether the lender's process is structured enough to stand up as a controlled, reviewable workflow instead of a collection of front-end screens and vendor calls.

That is why Eastern European lending expansion fails less often on scoring models than on onboarding design.

BNR, KNF, and CNB: Three Readings of the Same Borrower

On paper, all three markets ask familiar questions. Who is the borrower? Can the lender justify the decision? What evidence exists if the file is reviewed later? Where firms get caught is assuming those questions are answered in the same order and with the same proof.

In Romania, the practical pressure is usually on identity, traceability, and document quality. A lender needs to know that the onboarding file can show what happened, when it happened, and what evidence supported the approval path. If the identity step is weak, the rest of the risk stack inherits that weakness.

In Poland, affordability quickly becomes central. A lender may have a good fraud flow and still stall because the affordability layer is too light, too generic, or too hard to defend in audit. Poland is where many regional lenders discover that "we assess ability to repay" is not the same as proving how they assessed it in a local operating context.

In Czechia, the issue is often control architecture. Teams can get through pilot volume with manual interventions, spreadsheet workarounds, or loosely connected vendors. That stops scaling once the lender needs a repeatable, governed workflow with clear decision points, timestamps, escalation paths, and review evidence.

The borrower looks similar. The regulatory reading does not.

Affordability, Identity, and Registry Checks

Most cross-border lenders think first about IDV coverage. That matters, but it is only one third of the job. A durable Eastern Europe lending flow needs three layers working together:

1. Identity

The lender needs strong identity capture, document verification, liveness where appropriate, sanctions and PEP screening, and a clean audit trail. This is the layer most teams build first because it is visible and vendor-friendly.

For a full breakdown of identity verification requirements, see our KYC Requirements Explained 2026.

2. Affordability

The lender needs a consistent way to collect income inputs, structure borrower declarations, apply country-specific policy thresholds, and show why the affordability decision passed or failed. This is where one regional policy usually becomes three country variants.

3. Local data and registry connectivity

The lender needs the ability to pull, store, and reference the right local data sources, whether that means credit bureau feeds, registry checks, or market-specific enrichment. The exact connectors differ by market, but the architectural lesson is consistent: if registry logic lives outside the main workflow, launch timelines slip and audit quality drops.

Lenders that succeed in RO, PL, and CZ do not treat these as three separate products. They treat them as one operating model with country-specific evidence modules.

A Realistic Expansion Failure

Imagine a Bucharest-based digital lender that has proven origination economics in Romania and decides to expand into Poland and Czechia in one quarter. The product team keeps the same mobile onboarding, the same approval copy, and the same decision engine. Only the language layer changes.

The first problem appears in Poland. The team can verify identity, but the local affordability file is too thin. Inputs were collected, but the documentation model does not clearly show how the repayment assessment was formed or what evidence supported it.

The second problem appears in Czechia. Manual review exceptions start piling up because the fallback process was never formalized. Reviewers use chat, email, and spreadsheet notes. By month two, the lender cannot explain why similar files received different outcomes.

Nothing is "broken" in the product sense. But the launch stalls because the control system never localized.

That is the hidden cost of regional expansion. The failure is not usually credit policy. It is onboarding architecture.

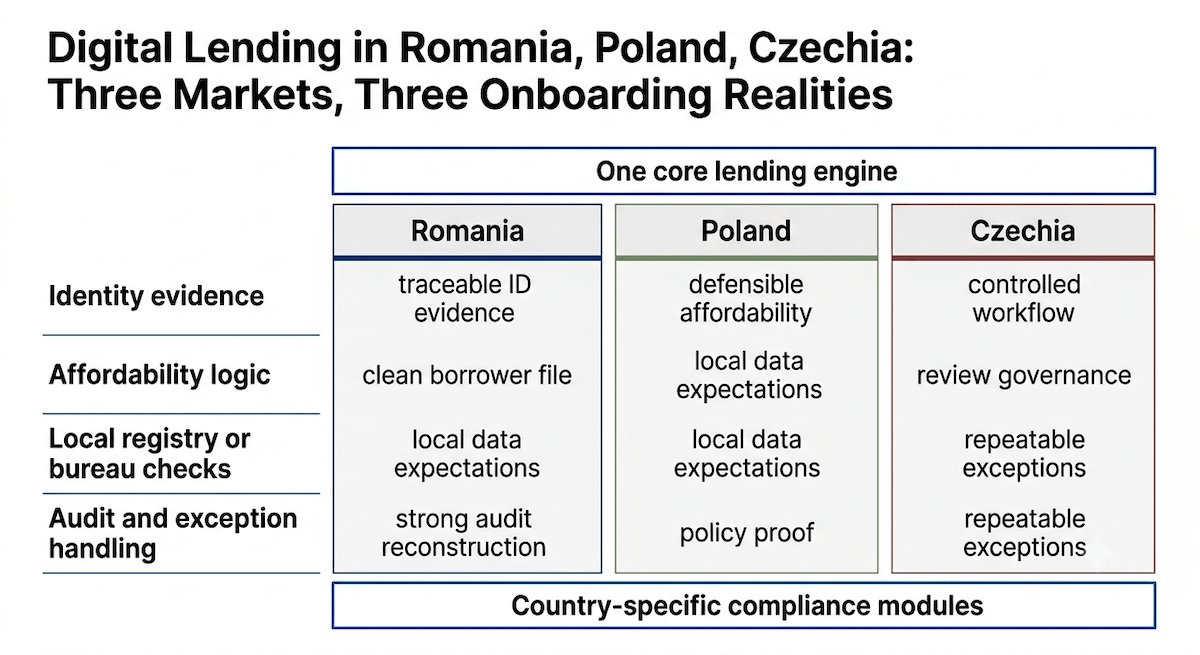

How VOVE ID Adapts One Stack to Three Regulators

VOVE ID is useful here because it does not force lenders to choose between one rigid global flow and three isolated local builds. The platform gives teams one core onboarding engine and lets them localize the control points that actually change.

For Romania, that means strong identity capture, reusable audit logs, and a file that can be reconstructed without hunting across tools.

For Poland, that means affordability-specific forms, decision evidence, and country-tuned review rules that sit inside the same borrower journey instead of in an offline appendix.

For Czechia, that means a governed exception process with structured reviewer actions, timestamps, escalation states, and a decision trail that survives scale.

The lender still runs one product. But the compliance logic bends where each market requires it:

| Layer | Romania | Poland | Czechia |

|---|---|---|---|

| Identity | High emphasis on clean evidence and file traceability | Must link identity to affordability decision quality | Must sit inside a controlled workflow |

| Affordability | Policy proof matters | Strong local defensibility is critical | Needs repeatable review logic |

| Local data | Market-specific enrichment and records | Local bureau or registry expectations are harder to ignore | Data plus process control must align |

| Audit trail | Reconstructable file | Justified decisioning | Governed exception handling |

That architecture matters commercially too. When one engine can localize policy, disclosures, reviewer paths, and evidence output, expansion stops depending on one-off operational heroics.

Checklist for RO, PL, and CZ Launches

- Identity: Can the lender prove what identity evidence was collected and how it affected the decision?

- Affordability: Is the repayment assessment visible, reviewable, and country-specific where needed?

- Registry: Are local bureau or registry checks integrated into the main flow instead of handled offline?

- Exceptions: Is manual review structured with states, timestamps, and ownership?

- Audit: Can the full borrower file be reconstructed without switching across five systems?

Q&A

Can one digital lending stack really work across Romania, Poland, and Czechia?

Yes, but only if the lender localizes compliance logic inside the same core workflow. Reusing the same front end without local policy and evidence changes is usually where expansion breaks.

What is the most common mistake in Eastern Europe expansion?

Treating onboarding as a translated UI problem instead of a country-specific operating model. The local friction usually sits in affordability evidence, registry integrations, and audit reconstruction.

Is identity verification enough to enter these markets?

No. Identity is necessary, but not sufficient. Lenders also need defensible affordability logic, local data connections, and a review process that stands up after scale.

Why do launches slip even when the decision engine is ready?

Because the decision engine is only one layer. Launches usually slip when disclosures, evidence capture, manual reviews, and local data dependencies were not built into the onboarding path.

Conclusion

Romania, Poland, and Czechia reward lenders that expand with discipline instead of copy-paste. The shared regional opportunity is real, but the onboarding stack has to adapt in three different places: identity, affordability, and local evidence.

The lenders that win in Eastern Europe do not build three products. They build one controlled system that knows how to behave differently in each market.

Would your onboarding file survive a review from BNR, KNF, and CNB on the same day? Most lenders discover the gap only after launch, when Poland asks for affordability evidence they don't have or Czechia asks for a review trail that was never structured. VOVE ID runs one onboarding engine that localizes identity, affordability, and audit evidence market by market.

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.