CASP Passporting Across the EU: Why Single-License Strategies Fail

Excerpt MiCA passporting opens EU markets. It doesn't build the operating model that survives them. In 2026, the firms that struggle aren't the ones without a passport — they're the ones whose compliance stack wasn't ready for the markets it opened.

For crypto firms serving Europe in May 2026, MiCA passporting is real, but the idea that one home-state authorisation automatically solves cross-border operations is still one of the most dangerous simplifications in the market. Legally, the passport is straightforward. Operationally, the minute a firm serves multiple Member States, it inherits multiple supervisory audiences, multiple complaint channels, and a much higher burden to prove that one operating model actually works everywhere it is used.

Why do single-license CASP strategies fail in practice? Because MiCA passporting gives a legal route to offer services across the EU, not a free pass to run one thin operational model everywhere. The firm still needs complaint handling, AML/CFT evidence, transfer-data controls, consumer-facing workflows, and supervisory records that hold up when host-state users, host authorities, or significant cross-border volumes create scrutiny beyond the home file.

The mistake is easy to understand.

Founders hear "EU passport" and translate it as:

- one authorisation

- one compliance file

- one consumer workflow

- one regulator relationship

That is not how cross-border crypto supervision works in 2026.

Start with the legal rule, because it is simpler than the reality

MiCA's legal passport is clear.

Article 65 says a CASP that wants to provide crypto-asset services in more than one Member State must notify its home authority with:

- the host Member States

- the services it will provide cross-border

- the intended start date

- its other activities outside MiCA

The home authority then has 10 working days to communicate that information to host single points of contact, ESMA, and EBA. The CASP can start providing services from the date it receives that communication, or at the latest on the 15th calendar day after submission.

That is the legal route.

It is efficient.

It is not the whole job.

Why 2026 still has a transition trap

This matters especially in the first half of 2026.

Some firms still speak as if grandfathering is close enough to passporting.

It is not.

ESMA said in January 2024 that grandfathered entities do not benefit from an EU passport. During the transitional period, cross-border services by a grandfathered entity depend on compliance with the relevant laws of both the home and host Member States.

That point still matters in May 2026, because some operators remain in the shrinking space between old national regimes and full MiCA authorisation.

So the first single-license failure is simple:

some firms try to scale a cross-border strategy before they actually hold the passport they think they have.

The passport solves market entry, not operating consistency

Once a firm is properly authorised, the next misconception appears.

The legal passport solves the authorisation route.

It does not eliminate cross-border operational complexity.

This is where the "single-license strategy" often breaks.

The firm is technically authorised.

But its operating model still assumes one-country conditions.

That fails quickly when the firm has to handle:

- complaints from users outside the home state

- different host-state supervisory concerns

- AML/CFT records touching several jurisdictions

- travel-rule and transfer-data issues involving counterparties across borders

- EMT-related payment-service overlaps in some product flows

In other words, the passport creates access to a market. It does not remove the need for multi-jurisdiction readiness.

ESMA has already signaled the real cross-border risk

This is not just a theoretical concern.

In its 31 January 2025 supervisory briefing on CASP authorisation under MiCA, ESMA said a significant amount of cross-border activity creates an additional layer of risk and responsibility. ESMA added that authorising one CASP can affect consumers outside the home Member State and said CASPs with more than 200,000 yearly active users outside the home state should face an elevated level of scrutiny.

More importantly, ESMA said home NCAs should coordinate with significant host NCAs so concerns about a CASP's ability to meet MiCA standards in host jurisdictions are identified as early as possible.

That is the quiet signal too many firms miss.

The passport may be home-state based.

The supervisory concern is not.

Once cross-border volume is meaningful, host-state reality comes back into the file.

Where single-license strategies usually fail

1. Complaints are local even when the licence is central

MiCA requires CASPs to maintain effective and transparent complaints-handling procedures. Clients must be able to file complaints free of charge, and the CASP must investigate them in a timely and fair manner.

MiCA also gives clients and other interested parties a route to complain to competent authorities, and those complaints must be accepted in an official language of the Member State where the complaint is submitted, or another language the authority accepts.

The practical lesson is obvious:

cross-border retail activity creates host-state complaint exposure whether the firm planned for it or not.

A CASP can hold one licence and still face:

- host-language customer complaints

- different complaint volumes by market

- local pressure after specific incidents

- questions from a host authority prompted by consumer patterns the home authority has not yet seen

So if the complaints process only makes sense in the home-state operating language, the passport strategy is thinner than it looks.

2. AML/CFT does not become one-country just because MiCA is harmonised

MiCA harmonises the CASP authorisation route.

It does not magically turn AML/CFT casework into a one-country operational file.

By 1 January 2026, AMLA had taken over EU-level AML/CFT mandates from the EBA, and the EBA said the existing AML/CFT guidelines remain in force until AMLA replaces them.

That means the cross-border AML expectation is becoming more converged at EU level.

But operationally, firms still need to manage:

- suspicious activity detection touching several Member States

- different FIU-facing consequences

- travel-rule failures involving non-domestic users or counterparties

- host-state pressure where local user populations become material

This is where founders confuse harmonisation with simplification.

They are not the same thing.

3. EMT-related services create an extra layer of coordination risk

The EBA's 12 February 2026 opinion on the end of the PSD2 and MiCA transition period is a direct warning here.

The EBA said that, where necessary, NCAs should cooperate with the relevant national authority under MiCA and other enforcement authorities when CASPs continue to provide EMT services that qualify as payment services.

That matters because a cross-border CASP may think it is scaling under one passport while parts of its EMT-related product set still create parallel payment-services questions.

That is not a purely theoretical overlap anymore.

It is a live 2026 supervisory coordination issue.

4. The same user file looks different once a host market becomes significant

This is the deeper operational problem.

A cross-border CASP may run one onboarding journey, one KYC logic, one complaints process, and one monitoring stack.

That seems efficient.

Then one host market becomes large enough that:

- its user complaints spike

- local payment behavior diverges

- local consumer expectations differ

- local supervisory attention increases

At that point, the platform is no longer judged only as "an EU CASP."

It is judged as a CASP materially active in that host market.

That is where a one-size-fits-all operating model starts to crack.

A realistic passporting failure

Imagine a France-authorised stablecoin platform serving users in Poland under MiCA passporting.

The legal setup is clean.

The home file looks fine.

The cross-border service is live.

Then two things happen:

- consumer complaints rise in Poland around redemption timing and account restrictions

- the Polish host market becomes material enough that local attention intensifies

Now the gap appears.

The platform can answer the AMF in French or English from one central team.

But it struggles to answer the more local questions that suddenly matter:

- how are complaints routed for Polish users?

- what local-language explanations do customers receive?

- how are travel-rule failures or account restrictions communicated?

- can the firm reconstruct the customer and case history for that host user cohort quickly?

The home regulator may see a manageable cross-border operation.

The host-state reality may look more fragile.

This is what single-license strategies miss.

The authorisation travels faster than the operating discipline.

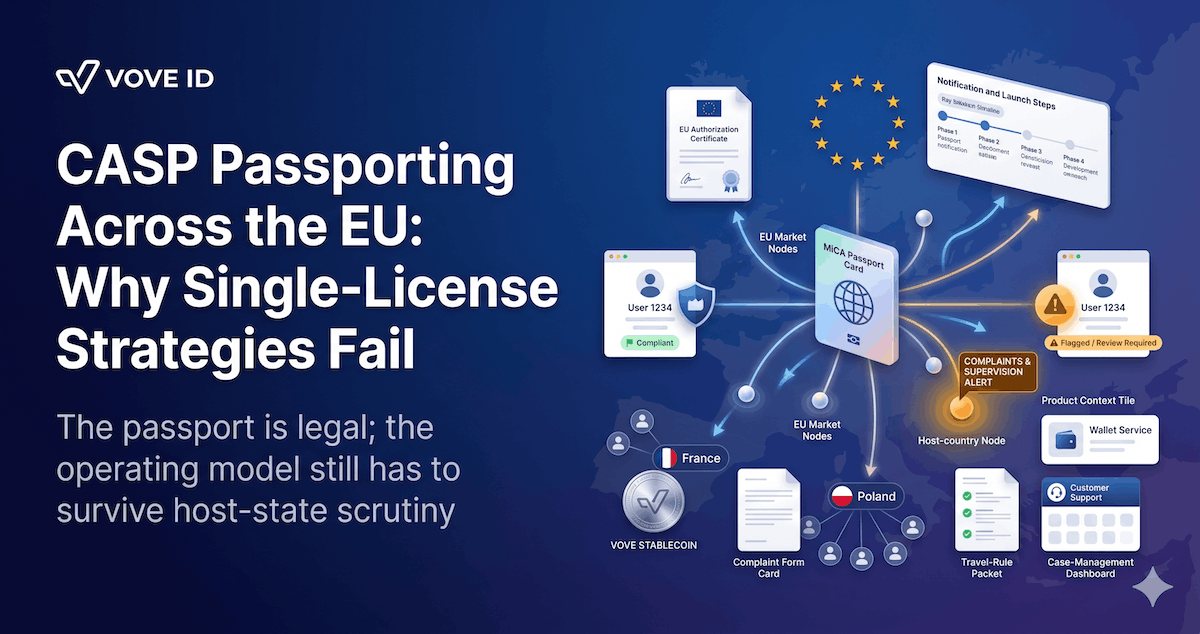

What a stronger cross-border CASP model looks like

The better model is not separate stacks for every country.

It is one core stack with explicit jurisdiction overlays.

Layer 1: one core MiCA authorisation and control framework

This includes:

- governance

- onboarding and identity verification

- custody or exchange controls

- monitoring

- complaints handling

- recordkeeping

Layer 2: host-state operating overlays

This includes:

- supported languages

- complaint-routing differences

- local user disclosures where relevant

- market-specific escalation patterns

- host-authority response readiness

Layer 3: cross-border risk thresholds

This includes:

- when a host market becomes "significant"

- when complaint volume triggers management attention

- when user concentration outside the home state changes supervisory risk

- when EMT or payment-service overlap requires extra coordination

That is how a CASP keeps one operating model without pretending every market behaves the same way.

How VOVE ID helps CASPs scale without forking the stack

VOVE ID helps cross-border fintech and stablecoin teams build one compliance operating layer with jurisdiction-aware controls.

That can include:

- onboarding and screening workflows that stay consistent across markets

- case management tied to the user, transfer, and complaint record

- travel-rule, wallet, and monitoring evidence in one file

- host-market escalation and review overlays without rebuilding the core workflow

- audit-ready records that hold up when home and host questions diverge

The value is not just scaling faster.

It is scaling without discovering too late that the licence travelled farther than the operating model.

Practical checklist for CASPs planning EU passporting

- Confirm whether the firm is fully MiCA-authorised or still relying on transitional logic.

- Map each host market before launch, not after the first complaint spike.

- Define what makes a host market operationally significant.

- Review complaints handling, language, and customer communication from a host-state perspective.

- Separate pure MiCA passport questions from AML/CFT and EMT-payment overlap questions.

- Build one evidence trail that can answer both home-state and host-state questions quickly.

- Treat cross-border growth thresholds as supervisory thresholds, not only growth metrics.

FAQ

Does MiCA give CASPs a real EU passport?

Yes. Article 65 gives authorised CASPs a cross-border notification route that allows them to provide services in other Member States after the required home-state communication process.

Does one MiCA licence mean one compliance model is enough everywhere?

No. The legal passport does not remove the need for complaints handling, AML/CFT records, travel-rule controls, and customer-facing operations that still work when host-state users or authorities become material.

Can grandfathered firms rely on MiCA passporting in 2026?

No. ESMA said grandfathered entities do not benefit from an EU passport. Cross-border activity during the transitional period depends on the relevant home and host national laws until a firm is fully MiCA-authorised.

What is the biggest cross-border mistake CASPs make?

They think authorisation and operating readiness are the same thing. The biggest failure is usually not the passport itself. It is the thinness of the cross-border operating model behind it.

Conclusion

CASP passporting across the EU works legally.

That is not the same thing as saying a single-license strategy works operationally.

By 2026, the EU framework is clear enough that the weakest firms are no longer the ones without a route to market. They are the ones that reached the market with one-country assumptions still embedded in a multi-country business.

The winning model is not twenty-seven separate stacks.

It is one serious stack that knows when a host market stops being "just another country" and starts becoming a real supervisory audience.

A MiCA passport opens markets. It doesn't build the operating model that survives them. VOVE ID helps cross-border CASP teams add jurisdiction-aware compliance overlays to one core stack — so the licence and the operating discipline travel together.