Dojah Alternative in Africa and Emerging Markets

A practical comparison for teams asking whether Dojah still fits once onboarding grows into KYB, monitoring, and regulator-facing evidence.

Dojah is a strong choice when a fintech mainly needs Africa-first identity verification and anti-fraud tooling. The problem starts when onboarding grows into a broader compliance workflow. That is usually the point where teams stop asking whether identity checks work and start asking whether the whole file is regulator-ready, auditable, and reusable across multiple products and markets.

VOVE ID helps fintechs in Africa and emerging markets when the requirement is no longer just to verify a person quickly. It helps when the business needs KYC, KYB, AML, monitoring, audit trails, and cross-border expansion to work as one operating layer instead of a chain of disconnected tools.

Direct Answer: Is VOVE ID a Good Dojah Alternative?

Yes, if the problem is bigger than identity verification.

If your product mostly needs fast onboarding checks inside African markets, Dojah can still be a good fit. If your team is expanding the compliance surface area across KYB, transaction monitoring, regulator-facing evidence, or multi-market operations, VOVE ID becomes the stronger alternative because it is designed around the full compliance workflow instead of a single onboarding step.

What Dojah Is Built For

Dojah is known for helping teams verify users and reduce onboarding fraud in African markets. That matters. For many early-stage fintechs, the first operational bottleneck is basic identity coverage, document verification, and fraud screening that works in the local context.

That means Dojah often fits well when:

- the company is Africa-first

- the immediate problem is identity verification speed

- the workflow is still concentrated around consumer onboarding

- the internal compliance team is small and the immediate need is execution, not system orchestration

Those are real strengths. The issue is not that Dojah is weak. The issue is that many fintechs eventually outgrow a tooling layer that is optimized around identity and fraud without also owning the broader compliance decision stack.

For a full breakdown of the identity verification framework this sits on top of, see our KYC Requirements Explained 2026.

Why Fintechs Start Looking For Alternatives

The search for a Dojah alternative usually begins when one of four things happens.

First, the onboarding file stops at KYC, while the regulator expects a broader record. A team can verify a user cleanly and still fail an audit because the decision trail, screening evidence, or operational logic cannot be reconstructed later.

Second, the business adds B2B onboarding. That introduces KYB, director verification, UBO checks, risk segmentation, and approval logic that consumer-first tools do not always cover cleanly.

Third, transaction monitoring and post-onboarding controls start mattering more than first-session verification. When a fintech grows, the risk story shifts from "can we onboard this user?" to "can we prove that onboarding, monitoring, and case handling form one coherent control system?"

Fourth, the company expands geographically or operationally. At that point, the question is no longer whether a vendor supports a market. The question becomes whether the same compliance infrastructure can support multiple markets, products, teams, and regulator conversations without turning into a patchwork.

For a full breakdown of business verification, UBO checks, and director review, see our KYB Requirements Explained 2026.

What A Better Alternative Actually Looks Like

A real alternative to Dojah should not just replicate identity checks. It should solve the next layer of operational pain:

- one system for KYC, KYB, AML, and monitoring

- a usable audit trail instead of scattered evidence

- support for business onboarding, not only individuals

- workflow logic that fits both African growth and cross-border expansion

- a decision layer that operations, risk, and compliance can all use

That is where VOVE ID is stronger. It is designed for fintechs that need compliance infrastructure, not just identity infrastructure.

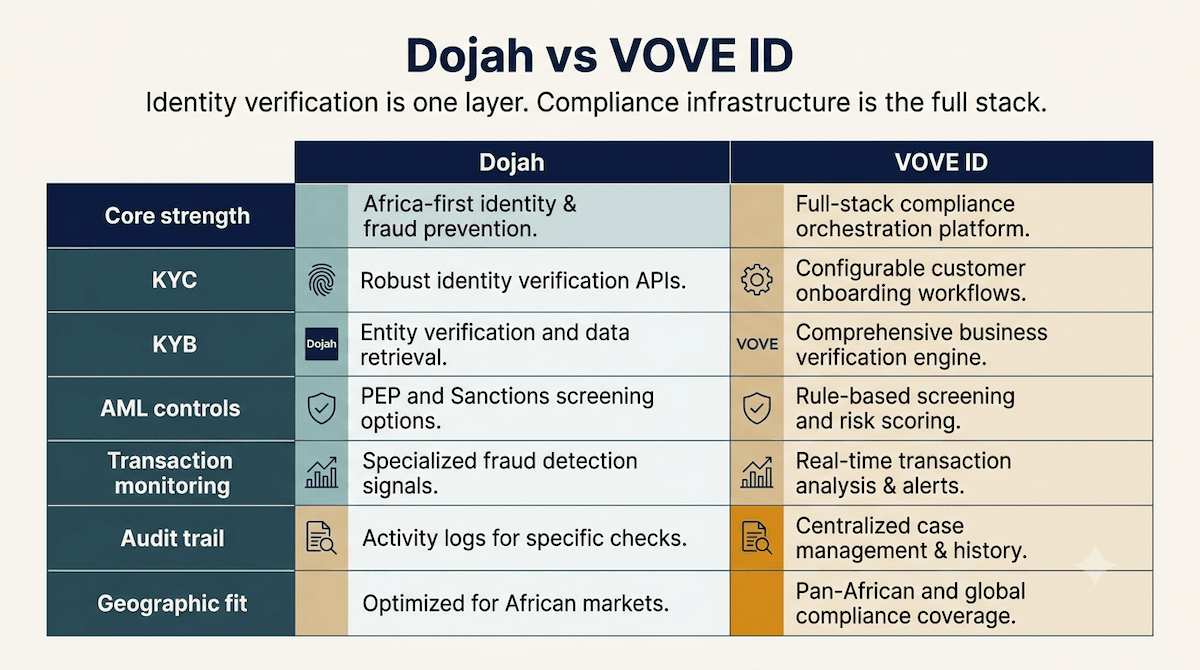

Dojah vs VOVE ID

| Area | Dojah | VOVE ID |

|---|---|---|

| Core strength | Africa-first identity verification and anti-fraud tooling | End-to-end compliance infrastructure for onboarding and ongoing controls |

| KYC | Strong for identity verification flows | Strong, with KYC embedded into a wider compliance decision layer |

| KYB | More limited if business onboarding becomes central | Built to support KYB, director checks, and broader business onboarding |

| AML controls | Can support front-end screening needs | Designed to connect onboarding, screening, monitoring, and case logic |

| Transaction monitoring | Not the main product center of gravity | Part of the broader compliance operating model |

| Audit trail | Depends on workflow design around the product | Emphasizes regulator-ready traceability and case reconstruction |

| Geographic fit | Excellent for Africa-first onboarding | Strong for African fintechs that also need broader operating coverage |

| Go-live posture | Fast for teams solving the first onboarding layer | Better when the team is solving for long-term compliance scale |

The practical difference is simple. Dojah helps prove who the user is. VOVE ID helps prove how the whole compliance decision was made and maintained.

When To Stay With Dojah

Staying with Dojah makes sense when your business is still centered on a narrow onboarding problem and that problem is being solved well.

That is especially true if:

- most onboarding is consumer KYC

- the company is operating mainly in African markets

- fraud prevention at sign-up is the main pressure point

- the compliance workflow outside onboarding is still relatively light

If those conditions still describe the business, replacing a working tool can create more noise than value.

When VOVE ID Is The Better Alternative

VOVE ID becomes the better alternative when compliance starts behaving like infrastructure instead of a feature.

That usually shows up when:

- business onboarding is becoming a revenue driver

- audits require a clearer decision trail

- multiple teams need the same compliance file

- onboarding and monitoring can no longer be run as separate systems

- expansion across Africa and Europe requires a more structured operating layer

In those cases, the real risk is not failed verification. The real risk is operational fragmentation. A fintech can pass onboarding and still lose time, revenue, and regulator confidence because the rest of the compliance stack is stitched together manually.

A Common Failure Pattern

Consider a growing cross-border fintech that started with a consumer wallet in one African market. Dojah handled identity verification well, so the team expanded into merchant onboarding and treasury flows. Six months later, a partner bank asked for clearer KYB records, a regulator asked how screening decisions were documented, and operations had to assemble evidence from multiple systems by hand.

Nothing failed in isolation. The identity checks worked. The business still slowed down because the compliance file was fragmented.

That is the kind of moment when teams start looking for an alternative. Not because the original product stopped working, but because the business now needs a compliance operating system, not just a verification endpoint.

How VOVE ID Changes The Operating Model

VOVE ID helps teams unify onboarding and ongoing controls into a single compliance motion.

Instead of treating KYC, KYB, screening, and monitoring as separate projects, the platform turns them into one operating layer with shared logic, shared evidence, and a cleaner path to auditability. That matters when a fintech has to move quickly without rebuilding its control environment every time a new market, product, or partner is added.

The benefit is not only risk reduction. It is operational leverage. Teams spend less time reconciling files, fewer decisions get trapped in inboxes and spreadsheets, and regulator-facing evidence is easier to produce when needed.

For a full breakdown of sanctions screening, monitoring, and audit-trail obligations, see our AML Requirements Explained 2026.

Checklist: What To Review Before Replacing Dojah

- Do we only need identity verification, or do we need a broader compliance workflow?

- Is KYB becoming a core onboarding requirement?

- Can we reconstruct a full compliance decision during an audit?

- Are onboarding and monitoring connected operationally?

- Are cross-border expansion plans exposing gaps in our current stack?

If most answers point beyond identity verification, the alternative you need is not just another verifier. It is a broader infrastructure layer.

Q&A

Is Dojah still a good tool for African fintechs?

Yes. It remains a strong option for Africa-first identity verification and anti-fraud use cases, especially when the main challenge is fast and localized onboarding.

What is the main reason teams switch away from Dojah?

Usually it is not because identity checks fail. It is because the compliance workflow expands into KYB, AML, monitoring, auditability, and cross-border operations.

Is VOVE ID only useful for Europe-facing teams?

No. It is useful for African and emerging-market fintechs that need broader compliance orchestration, including those expanding into multi-market or partner-heavy operating models.

What should a fintech compare first?

Compare the real operating need, not the feature list. If the need is identity verification alone, the answer may differ from a team that needs business onboarding, decision audit trails, and ongoing controls in one stack.

Conclusion

Dojah is a credible Africa-first verification product. But many fintechs outgrow verification as the center of the problem. Once compliance becomes a multi-step operational system, the better alternative is the one that can connect onboarding, risk, and auditability without forcing the team to assemble that architecture manually.

Curious whether VOVE ID is the right Dojah alternative for your onboarding and compliance stack?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.