EUR-to-USDC Settlement: KYC When the Counterparty Is a Wallet

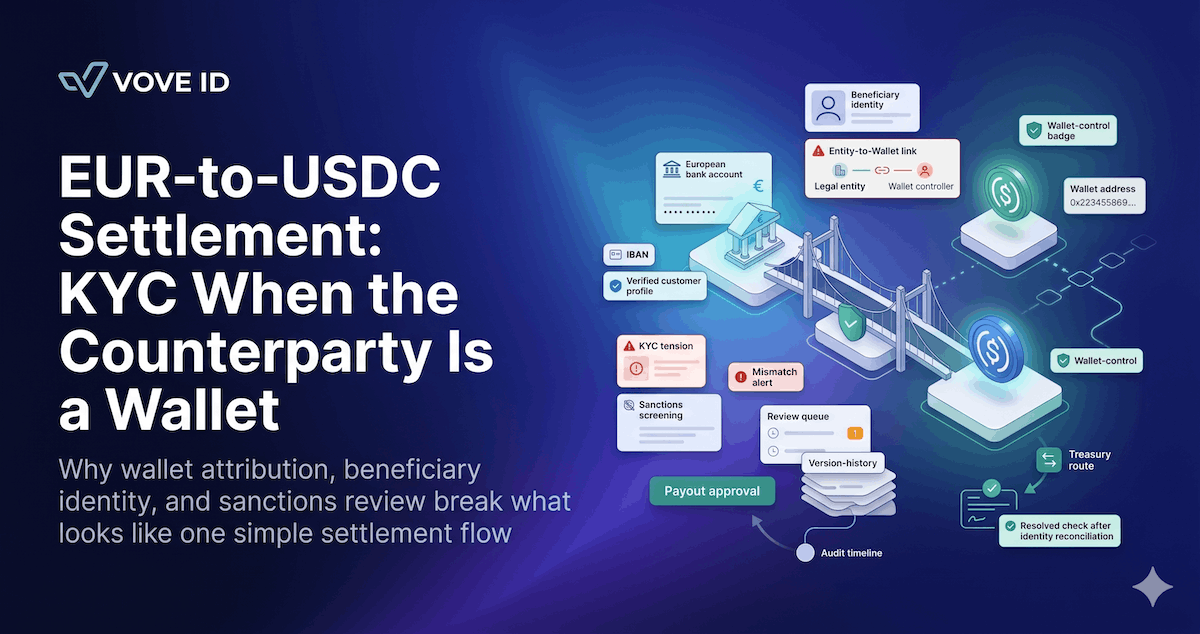

EUR-to-USDC settlement looks like one transfer. In practice it's two identity regimes meeting in one payout decision — and the wallet side doesn't prove identity the same way a bank account does.

EUR-to-USDC settlement looks simple when one side is a verified bank account and the other is just a blockchain address. In practice, that address creates a second identity problem that many fintech teams still treat like transfer metadata instead of customer risk.

Why is EUR-to-USDC settlement a KYC problem when the counterparty is a wallet? Because the fiat side and the wallet side do not prove identity in the same way. A bank account can be tied to a named customer record, but a wallet only becomes usable compliance evidence when the team can show who controls it, how it was screened, and whether that answer was still true when settlement happened.

VOVE ID helps fintechs run EUR-to-USDC settlement in markets where one leg of the transfer lives inside bank-grade onboarding and the other lives inside wallet attribution, sanctions logic, and corridor-specific review. On paper, the trade is one settlement event.

In practice, it is two identity regimes meeting in one payout decision.

This is where settlement teams lose control over risk.

Why this becomes a KYC problem before it becomes a settlement problem

Teams often focus first on price, treasury, and transfer speed.

Those matter.

But the operational break usually appears earlier, at the moment the team has to decide whether the wallet receiving USDC is actually linked to the person or business it thinks it is paying.

That is what makes EUR-to-USDC different from a normal bank transfer.

A bank account usually comes with:

- an account-holder name

- an institution in the payment chain

- a customer file already linked to onboarding records

- a familiar exception process when something does not match

A wallet address does not arrive with that context built in.

It has to be attached.

Under Regulation (EU) 2023/1113, which has applied since 30 December 2024, EU-facing crypto-asset transfer chains have to carry originator and beneficiary information, and transfers involving self-hosted addresses above EUR 1,000 trigger additional ownership-or-control assessment steps. That means one thing.

The wallet cannot stay a floating field inside the settlement flow.

The wallet side and the bank side age differently

This is the part many teams underestimate.

The bank-side customer record is often relatively stable. The name, account, and KYC file may be refreshed periodically, but the structure is familiar.

The wallet side moves faster.

A wallet may be:

- newly provided by the customer after onboarding

- controlled by a treasury desk rather than the legal entity named in the invoice

- replaced before payout because of custody or routing changes

- close to an exposure the sanctions engine did not flag at the first review

So while the EUR side looks complete, the USDC side may still be changing.

That is not a blockchain problem.

It is a record-governance problem.

If the team cannot show which wallet was approved, who or what it was tied to, and what screening result applied to that exact version of the record, the settlement file is weaker than it looks.

Self-hosted and omnibus wallet structures expose the real gap

The break point becomes visible as soon as a customer does not use a clean institutional destination.

Some fintech teams settle to:

- self-hosted wallets

- exchange deposit addresses

- treasury wallets shared across entities

- third-party payment or OTC counterparties acting on behalf of a business

Each one changes the KYC burden.

A self-hosted address raises the question of ownership or control. An exchange address raises the question of whether the receiving platform's identity information is strong enough to support the corridor. A shared treasury wallet raises the question of which legal entity in the group the payout actually belongs to.

On paper, all three may look like valid destination wallets.

In practice, they are different compliance cases.

This is why teams get into trouble when wallet collection happens too late. If the address is gathered right before payout, reviewers are forced to make an identity decision under time pressure, with weak evidence and a strong commercial incentive to let the transfer through.

Sanctions and monitoring decisions only work if they stay tied to the same wallet record

A lot of wallet-side failures are not failures to screen.

They are failures to keep the screen attached to the final record.

Consider what happens in a live EUR-to-USDC flow:

- the customer submits a wallet

- the wallet is screened

- treasury asks for a different destination

- operations updates the payout instructions

- the transfer is released

- a later review tries to determine which wallet was actually approved

Now ask the hard question.

Did the sanctions decision apply to the wallet that received the USDC, or to the wallet that was first entered into the case?

If the answer requires Slack messages, email chains, and separate blockchain logs, the control has already weakened.

This matters even more in 2026 because stablecoin settlement teams are operating in an environment where payment transparency expectations keep tightening. FATF updated Recommendation 16 in June 2025 to improve transparency and reduce fraud and error in cross-border payments. The direction of travel is clear even when the transfer does not look like a classic retail payment.

The compliance standard is moving toward cleaner identity continuity across the chain.

A realistic settlement failure: when the wallet belongs to the wrong entity

A Dutch payments fintech offers EUR-to-USDC settlement to import-export SMEs.

The workflow looks disciplined:

- the business client passes KYB

- the director is verified

- the EUR funding account is confirmed

- the invoice and beneficiary details are collected

- the destination wallet is screened before payout

Then the weak point appears.

The merchant says the USDC should go to a treasury wallet used by its group. The legal entity that signed the commercial agreement is one subsidiary. The wallet is actually administered by a group finance function tied to another entity. Operations receives the change in a support thread. Treasury updates the payout destination. The sanctions screen on the first wallet was clear. The second wallet sits near a cluster the blockchain tool rates as elevated risk.

Settlement is urgent.

The team pays anyway because the group relationship feels commercially obvious.

Months later, an internal review asks a basic question: which entity was actually the beneficiary of the USDC payout, and what screening result supported that conclusion?

The team now has to reconstruct:

- which wallet was first submitted

- which wallet was finally paid

- whether the legal beneficiary and wallet controller were the same entity

- whether the second wallet received a full review

- whether the transfer evidence still matches the case narrative

This is not a treasury failure.

It is a KYC and record-integrity failure inside a settlement workflow.

What strong EUR-to-USDC settlement operations look like

The best teams do not treat the wallet as an optional extension of the payout.

They treat it as part of the customer and counterparty identity model.

That means:

- collecting wallet information early enough for real review

- storing the reason the wallet is linked to the customer or beneficiary

- separating wallet collection from wallet approval

- logging every wallet change as a case event, not an ops shortcut

- keeping sanctions, screening, and payout approval tied to the final wallet version

The goal is not to slow settlement down.

It is to remove unresolved identity jumps before settlement happens.

That is what lets the business move quickly without turning every exception into manual reconstruction work.

How VOVE ID resolves identity on both sides of the settlement

VOVE ID helps teams handle the EUR side and the wallet side inside one operational record.

For EUR-to-USDC settlement, that means teams can:

- connect business or customer onboarding to the payout-side wallet record

- store wallet ownership or control evidence next to the case

- run screening and review on the exact destination that will receive value

- preserve a timeline when beneficiary or wallet details change mid-flow

- retrieve one explainable case when banking partners, auditors, or supervisors ask what happened

This is the difference between a settlement team that merely screens wallets and one that can defend why a specific wallet was paid.

Practical EUR-to-USDC settlement checklist

Identity

- Collect the destination wallet before the payout reaches treasury release.

- Record why that wallet belongs to the customer, beneficiary, or authorized treasury function.

- Separate legal beneficiary identity from wallet-controller identity when they are not the same.

Screening

- Re-screen any wallet that changes after the first approval step.

- Keep the screening result attached to the final wallet version, not just the first one submitted.

- Flag self-hosted and omnibus-style destinations for enhanced review logic.

Operations

- Treat wallet changes as case events with timestamp, owner, and rationale.

- Keep invoice, beneficiary, wallet, and payout approval in one timeline.

- Test whether a reviewer can reconstruct the final payout without opening chat tools.

Audit

- Store ownership-or-control evidence for self-hosted addresses above relevant thresholds.

- Keep a clear record of which entity received value when group treasury structures are used.

- Review whether settlement cases can be exported in a form a bank or regulator can understand quickly.

FAQ

Is a screened wallet enough to make EUR-to-USDC settlement compliant?

No. Screening is only one control. The team also needs a defensible link between the wallet, the beneficiary, the customer file, and the final settlement decision.

Why is a bank-verified customer still not enough?

Because the USDC leg introduces a second destination identity. The verified sender or funding account does not automatically prove who controls the receiving wallet.

Are self-hosted wallets the only difficult case?

No. Exchange deposit addresses, omnibus treasury wallets, and group-entity payout structures can all create the same problem if the record does not clearly show who the wallet belongs to.

What should teams fix first?

Fix wallet collection and change control first. Most settlement failures begin when the destination wallet enters the process too late or changes without a clean review trail.

Conclusion

EUR-to-USDC settlement is not only a payments workflow.

It is an identity workflow that crosses two different systems of proof.

Teams that want to scale this corridor in 2026 need more than a screened address and a fast treasury motion. They need one case record that keeps bank-side identity, wallet-side identity, screening decisions, and payout approval aligned from start to finish.

That is what turns wallet settlement from a compliance blind spot into an explainable operating model.

EUR-to-USDC settlement crosses two identity regimes in one payout decision. VOVE ID connects bank-side onboarding, wallet attribution, sanctions review, and audit evidence into one settlement record — so the team can defend which wallet was paid and why.