Sanctions Screening for SME Onboarding: What Sub-1% Match Rates Hide

A sub-1% sanctions match rate can look like efficiency. For EU fintechs onboarding SMEs, it can also mean the screening logic never found the sanctioned director hiding one layer inside an otherwise clean file.

A sub-1% sanctions match rate can look like proof that your SME onboarding stack is clean. In practice, it can also mean the stack is too narrow, too literal, or too shallow to see the risk that matters. For EU fintechs onboarding businesses in 2026, the better question is not whether the dashboard looks quiet. It is whether the screening logic would still catch a sanctioned director, beneficial owner, or control relationship hiding inside an otherwise ordinary SME file.

Why can a sub-1% sanctions match rate be a warning sign in SME onboarding? Because a very low hit rate is not automatically evidence of precision. It can also mean the screening logic is missing aliases, transliterations, beneficial owners, directors, or ownership links. In a business-onboarding context, the risk often sits around the company, not only in the company name itself.

Low match rates are easy to celebrate.

They make a compliance dashboard look efficient:

- few alerts

- fast onboarding

- low analyst workload

- less friction with sales and operations

That is why many teams start treating the match rate itself like a quality signal.

The problem is that sanctions screening is not a conversion metric. It is a control.

A control is only good if it catches the risk it is supposed to catch.

In the EU, that standard is getting harder to fake with tidy reporting alone. The European Banking Authority's final Guidelines on internal policies, procedures and controls for restrictive measures were published in November 2024 and apply from 30 December 2025. They explicitly focus on KYC, screening, and due diligence for firms handling transfers of funds and crypto-assets. At the same time, the European Commission's consolidated financial sanctions list is updated to reflect the official texts published in the Official Journal of the EU. That means the question is no longer whether sanctions screening exists. The question is whether it works against live, messy, multilingual business data.

For SME onboarding, that is where low match rates start to become suspicious.

Why a low match rate can be the wrong comfort signal

A low hit rate can mean one of two very different things.

It can mean:

- the customer base is genuinely low risk

- the screening model is calibrated well

- the business collects clean identity and entity data

- the review process resolves false positives efficiently

Or it can mean:

- the system screens only exact names

- directors and UBOs are not screened properly

- aliases and local spelling variants are ignored

- corporate ownership links are missing

- watchlist data is being matched too narrowly

Those are not the same operational reality.

The trouble is that both realities can produce the same neat dashboard.

A payment or B2B fintech onboarding SMEs across the EU will often face company records that are not uniform. The entity may be registered in one country, trade under another brand, bank through another jurisdiction, and include controllers whose names appear differently across registries, passports, and sanctions sources.

If the screening engine only checks the legal-entity name in a rigid way, the output can look impressively clean while the actual exposure stays hidden.

That is why a sub-1% rate should trigger a second question:

What exactly are we screening, and how exactly are we matching it?

Match logic: what "tight" and "loose" actually mean

Most teams talk about sanctions matching in vague terms.

They say the logic is:

- too strict

- too fuzzy

- over-alerting

- under-alerting

That language is not precise enough.

For SME onboarding, match quality depends on several layers at once.

1. Name normalization

The engine needs to handle:

- punctuation differences

- spacing differences

- legal-form noise like GmbH, SAS, BV, or sp. z o.o.

- abbreviated first names

- reordered surnames

If the system treats each variation as a different identity, it will miss obvious overlaps.

2. Transliteration and language variants

This is one of the most common blind spots in EU business onboarding.

A director or beneficial owner may appear with different Latin spellings depending on:

- passport format

- registry source

- local language conventions

- whether the source preserved diacritics

That means an apparently clean result can simply reflect weak transliteration logic.

3. Entity-only screening

Many teams still screen the company and assume that is enough.

For SME onboarding, it often is not.

The actual risk can sit in:

- directors

- beneficial owners

- controlling shareholders

- authorized signatories

- parent entities

A company can return a clean entity result while a sanctioned or high-risk controller sits one layer deeper in the file.

4. Ownership and control logic

Business sanctions risk is not only about direct name matches.

It is also about whether the onboarding team understands:

- who owns the company

- who controls it operationally

- whether that control is direct or indirect

- whether the ownership picture changed since the last review

If ownership screening is disconnected from entity onboarding, the result is false comfort.

5. Threshold setting and alert routing

Loose thresholds can drown a team in noise.

Over-tight thresholds can erase the very alerts the system is supposed to create.

Good tuning is not about chasing the lowest alert rate. It is about reaching a hit rate that is plausible for the customer base, the jurisdictions served, and the amount of ambiguity in the underlying data.

Why SME onboarding makes the problem harder

Retail screening is already imperfect.

SME screening is harder because one business file can contain multiple screening subjects at once:

- the legal entity

- one or more directors

- one or more UBOs

- signatories

- parent companies

- operating brands

That means the screening problem is not a single comparison. It is a small graph problem.

The more cross-border the business model, the more that graph expands.

An EU fintech onboarding merchants, SMB borrowers, or marketplace sellers may regularly see:

- local-language registry extracts

- ownership chains across several Member States

- directors with multiple spellings

- founders using personal bank accounts or nominee structures

- inconsistencies between registry, tax, and banking data

If the screening engine is not designed for that kind of data, a low alert rate can simply mean the graph never got built.

A realistic screening failure

Imagine an EMI onboarding an SME customer operating across Spain and Poland.

The file looks straightforward:

- the entity is incorporated and active

- the business purpose appears ordinary

- the company name screens clean

- the onboarding team moves fast

But one director's surname appears slightly differently across documents.

The registry uses a local spelling. The passport record uses a transliterated form. The sanctions data uses another Latinized variant. Because the firm's logic is too narrow, the director never triggers a meaningful review.

Months later, a spot check finds that the director should have been escalated.

Now the team has three problems:

- the original screening control did not work

- the onboarding decision is hard to defend

- the low historical hit rate looks less like efficiency and more like under-detection

This is the real danger of celebrating a sub-1% match rate too early.

The problem is not the number itself.

The problem is what the number may be hiding.

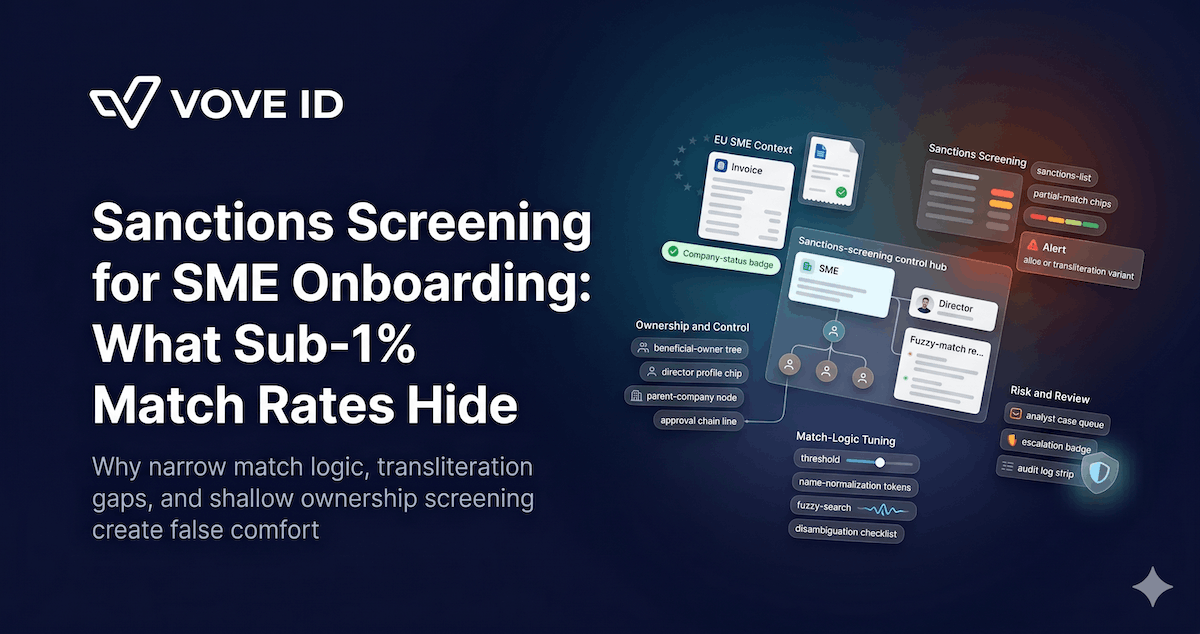

What stronger sanctions screening for SME onboarding looks like

A better model does not aim for maximum noise or minimum noise.

It aims for defensible signal quality.

That usually requires five things.

1. Screen the full business relationship, not only the entity

The file should cover:

- the company

- directors

- beneficial owners

- signatories

- relevant parent or control entities

Entity-only screening is too thin for serious KYB.

2. Tune matching for real EU name variation

That means supporting:

- transliteration variants

- diacritics and stripped diacritics

- legal-form removal

- token-order changes

- fuzzy thresholds that can distinguish between likely and weak matches

The point is not to make matching looser everywhere. It is to make it smarter where EU business data is predictably messy.

3. Connect screening to ownership resolution

If UBO mapping sits outside the screening workflow, the team will always miss part of the risk perimeter.

Screening should be able to move from:

- entity

- to director

- to owner

- to parent

- to related control relationships

That is how the team finds the risk inside a clean-looking company.

4. Use review queues that separate signal from noise

Not every partial match should block onboarding.

But every plausible match should land in a queue that shows:

- why it matched

- which fields matched

- how strong the match is

- what alternative spellings were involved

- which ownership or role link made the result relevant

That is how an analyst reviews faster without reviewing blindly.

5. Measure the right metrics

Match rate alone is too crude.

Teams should also watch:

- alert-to-case conversion

- true-positive rate

- false-positive rate

- average review time

- percentage of alerts tied to directors or UBOs

- percentage of escalations caused by alias or transliteration logic

Those numbers say more about control quality than a neat sub-1% headline ever will.

How VOVE ID calibrates sanctions logic to actual EU SME data

VOVE ID helps fintech teams treat sanctions screening as part of a real business-verification workflow instead of a standalone name check.

That includes:

- entity verification connected to screening

- director and UBO screening inside the same case flow

- ownership-aware review logic

- multi-locale name normalization and transliteration support

- risk-based thresholds that reduce noise without suppressing signal

- audit-ready records showing why a match was cleared, escalated, or rejected

The practical value is simple.

A team can move faster without pretending that a quiet dashboard means the risk disappeared.

That matters most for SME onboarding, where sanctions exposure is often indirect, multilingual, and easier to miss than the topline metric suggests.

The real goal is not a low match rate

The real goal is a sanctions control you can defend.

For EU SME onboarding, that means:

- screening the right people, not just the right company name

- matching across real-world spelling variation

- connecting sanctions checks to KYB and ownership data

- routing plausible matches into explainable review

A sub-1% rate may be good.

It may also be a warning.

What matters is whether the system can still find the sanctioned director hiding inside the apparently clean record.

If it cannot, the dashboard is not clean. It is incomplete.

Want to see how VOVE ID calibrates sanctions screening for EU SMEs?

Q&A

Is a low sanctions match rate always a bad sign?

No. A low rate can be perfectly reasonable for a low-risk customer base with strong data and well-calibrated screening. It becomes suspicious when the logic is too narrow, the file covers only the entity, or the team cannot explain how aliases, transliterations, and ownership links are handled.

Who should be screened in an SME onboarding file?

At a minimum, teams should think beyond the entity name and assess directors, beneficial owners, controlling persons, and other relevant parties tied to the business relationship.