SME Lending in 2026: KYB, Director Verification, and Credit Decisioning as One Flow

Why treating entity checks, director verification, and credit approval as a relay creates gaps that surface exactly when a regulator asks for evidence.

VOVE ID helps SME lenders in markets where the three steps cannot keep adding up. On paper they are sequential. In practice they have to be one decision.

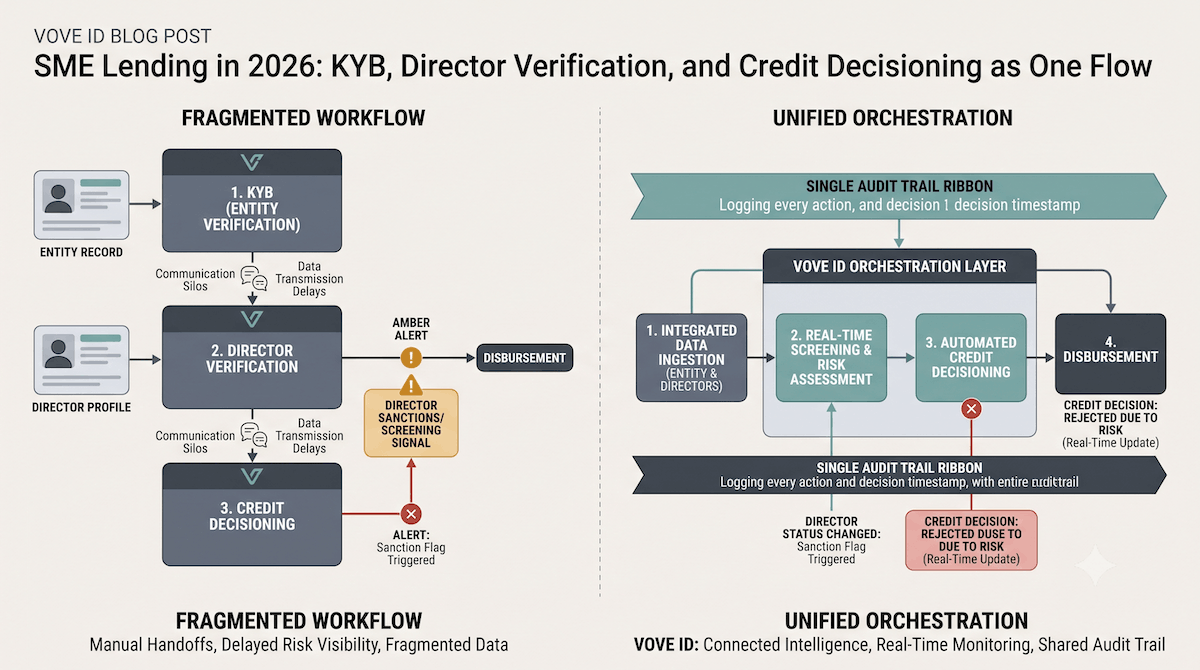

For years, SME lending stacks were built as a relay. First the entity passes KYB. Then the director or beneficial owner goes through KYC. Then the credit team or model makes the lending decision. That structure made sense when each step lived in its own system and the pace of decisioning allowed for handoffs.

In 2026, that separation is becoming the problem. Risk signals move too quickly, cross-border files are too messy, and the operational cost of stitching together three partial answers is too high. SME lenders now need one flow that can decide on the entity, the humans behind it, and the lending outcome together.

The question is no longer whether each control exists somewhere in the business. The question is whether the lender can show that the three controls were run in the right sequence, with the right dependencies, and with one audit trail strong enough to defend the final approval.

Why three steps cannot stay three in 2026

The traditional split between KYB, director verification, and credit decisioning creates dead space in the workflow. Information passes between teams, but responsibility does not always pass with it. That is how an entity can clear KYB while the director review is still incomplete, or a credit decision can move forward before the latest sanctions or adverse-media result is incorporated into the file.

This problem gets worse in SME lending because the company and the controller are not independent compliance objects. The credit case often depends on both at once. Ownership complexity, delegated authority, directorship changes, and cross-border entity structures mean the lender cannot safely pretend the entity decision is finished before the human decision is finished.

What used to be acceptable as a sequence of tasks now looks like fragmentation. The more systems involved, the harder it becomes to answer a simple audit question: why was this company approved at this moment, by this workflow, with these exact risk checks?

For a full breakdown of entity verification and UBO checks, see our KYB Requirements Explained 2026.

Director verification: the step most stacks treat as optional

Many SME lending stacks still behave as if director verification is a secondary check that can be cleaned up later. That is the wrong assumption. Director identity, authority, sanctions exposure, and relationship to the entity can all change the risk posture of the loan. If the director check is weak, the KYB result is incomplete by definition.

The operational issue is that director verification is often treated as a manual bridge between systems. One tool handles the entity. Another handles the person. A spreadsheet or queue handles the linkage. When volume rises, that bridge becomes the failure point. Cases sit waiting for handoff, reviewers duplicate work, and the final decision ends up relying on stale snapshots.

In other words, the optional-looking step is often the one that determines whether the entire file is trustworthy.

For a full breakdown of individual identity verification requirements, see our KYC Requirements Explained 2026.

A realistic SME lending failure: when KYB passes and the director fails sanctions

Imagine a German SME lender reviewing a 200,000 EUR loan request from a clean-looking operating company. The entity clears KYB quickly. Registry data is present, incorporation details line up, and the business profile fits policy. The file moves forward.

What the lender misses is timing. The director was screened separately and later. Between the initial entity review and the pre-disbursement step, the director hit a sanctions list. Because the workflows were not unified, the credit decision was already treated internally as complete. Now the team has to halt the file, re-open the approval chain, and explain why a company-level pass was allowed to outrun the human-level controls that were material to the decision.

This is not a corner case. It is the predictable outcome of disconnected compliance steps. When the entity, the director, and the credit logic do not share one control surface, the lender creates room for contradictions inside the same file.

For a full breakdown of sanctions screening obligations, see our AML Requirements Explained 2026.

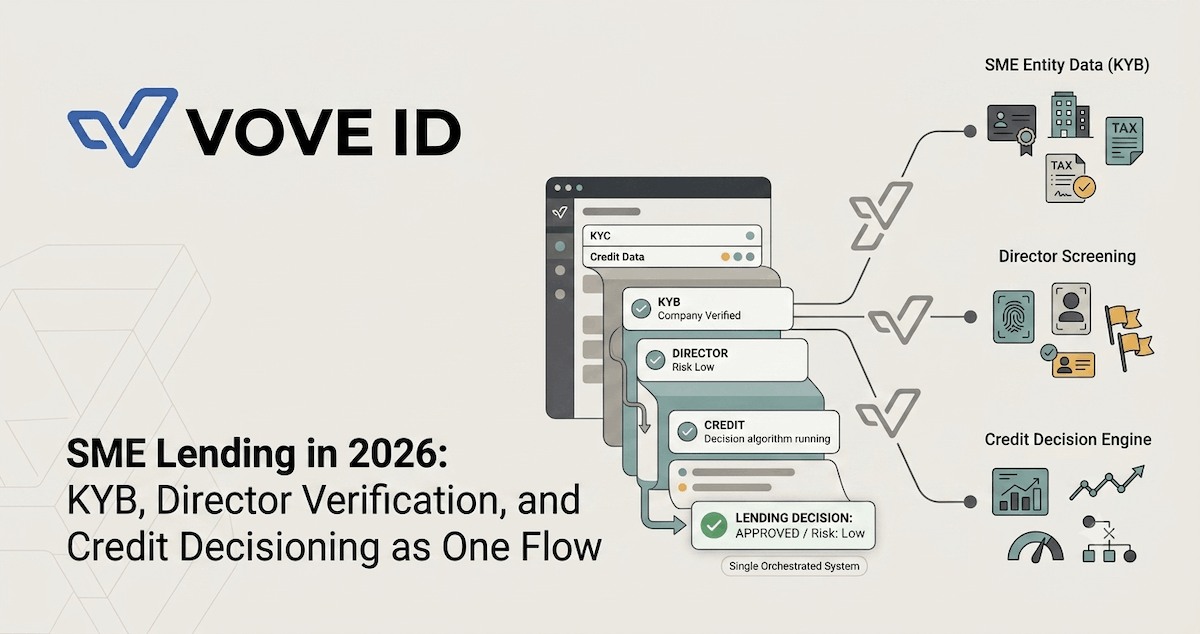

How VOVE ID collapses KYB, director KYC and credit into one decision

VOVE ID lets SME lenders orchestrate entity verification, director checks, screening, and decision evidence inside one flow. That means the case does not move forward as if it were complete while a material human review is still pending or stale. The lender can define dependencies between controls, trigger screening at the right points, and ensure the final credit outcome reflects the latest combined state of the file.

This is the difference between having all the right components and actually running them as one system. For SME lenders, the control win is not merely automation. It is coherence. One workflow means one version of the file, one place to inspect why a case was approved or blocked, and one audit trail that shows how entity, director, and credit logic came together.

That is what 2026 demands. Not more disconnected checks, but fewer gaps between them.

Checklist

- Entity verification tied directly to the decision flow

- Director identity and screening treated as mandatory decision inputs

- Credit approval blocked until the combined file state is complete and current

Q&A

Why is director verification such a big issue in SME lending?

Because the company cannot be assessed in isolation. Director identity, authority, and sanctions exposure can materially change whether the lender should approve the file at all.

Isn't KYB enough if the company itself looks clean?

No. A clean entity record does not resolve who controls the company, who signs on its behalf, or whether a human risk signal undermines the approval.

What does "one flow" actually change operationally?

It removes the gap between separate tasks. Instead of KYB, KYC, and credit each progressing on their own timeline, the lender can enforce dependencies and keep one defensible audit trail from intake to decision.

Conclusion

SME lending workflows break when they confuse sequential tasks with a complete decision system. In 2026, KYB, director verification, and credit logic need to operate as one flow because the audit question is always about the whole file, not the fragments. Lenders that still separate them will keep discovering the same problem at the worst possible moment.

Want to see how VOVE ID makes SME lending one decision, not three?

This article is intended for general informational purposes only and does not constitute legal, financial, or regulatory advice. KYC/KYB/AML requirements may vary depending on jurisdiction, industry, and specific business circumstances. For up-to-date and binding compliance obligations, readers should refer to the relevant regulatory authorities or consult qualified professionals.