Transaction Monitoring API: Real-Time AML Screening for Payment Providers and BaaS

Transaction monitoring APIs help payment providers detect suspicious behavior in real time, connect activity to the right customer or merchant, and route cases into review before risk escalates.

A transaction monitoring API helps payment providers and BaaS teams detect suspicious behavior as it happens, connect that behavior to the right customer or merchant, and route the case into review before risk turns into an operational failure. In 2026, that matters because payment volume scales faster than manual review, and regulators still expect suspicious activity monitoring, escalation, and evidence retention to stay attached to the live flow.

How does a transaction monitoring API work for payment providers?

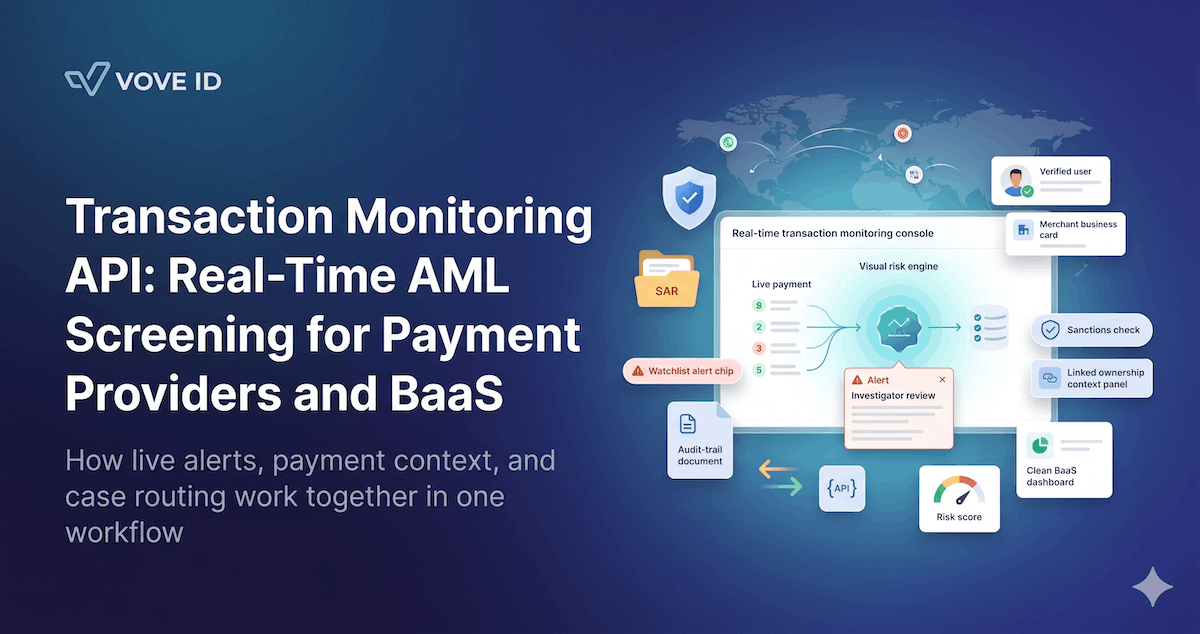

A transaction monitoring API ingests payment events, customer and merchant context, sanctions and watchlist signals, and rule logic in one workflow. It scores activity in real time or near real time, triggers alerts when behavior breaks expected patterns, and gives operations teams the case context they need to hold, review, escalate, or report suspicious activity.

Payment providers often think they already have monitoring because they can search transactions after the fact.

That is not the same thing.

The real test is whether the team can spot a risky payment pattern early enough to act, explain why it was flagged, and reconstruct the decision later without stitching together exports from five systems.

This is exactly where many payment and BaaS programs break.

Why payment monitoring fails when it sits outside the payment flow

On paper, transaction monitoring sounds straightforward.

The team defines a few rules, sends transactions into a review queue, and investigates whatever looks unusual.

In practice, weak monitoring usually fails in one of three places.

1. The system sees the transaction but not the relationship

An alert without context is noise.

Teams need to know which merchant, user, program, corridor, counterparty, or account relationship sits behind the payment. If the monitoring layer is detached from onboarding and merchant data, reviewers end up investigating blind.

2. The rules are too slow for the payment model

Some payment events need intervention before execution. Others need pattern detection across hours, days, or weeks.

If the stack only runs overnight batch review, it misses real-time control opportunities. If it only runs instant checks, it misses slower structuring and behavior drift.

3. The case file starts after the alert

This is where evidence quality collapses.

If the alert, transaction history, KYC or KYB record, sanctions results, and reviewer actions do not live in one chain, the team loses time every time it needs to explain what happened.

What a real transaction monitoring API should actually do

Payment monitoring is not a single model. It is a control surface.

A useful API usually needs five connected capabilities.

1. Ingest payment events in a structured way

The API should accept:

- transaction amount

- currency

- sender and recipient identifiers

- merchant or program relationship

- corridor or geography

- payment method or rail

- timestamps and velocity context

This means one thing: monitoring quality depends on the shape of the input.

If the payment event reaches the system as a flat amount plus account ID, the rules will stay shallow.

2. Run real-time checks before or during execution

For payment providers and BaaS teams, some risks should be caught immediately:

- sanctions or watchlist hits

- blocked countries or counterparties

- velocity spikes

- rapid repeat transactions

- behavior that falls outside the known customer or merchant profile

This is where an API matters more than a reporting dashboard.

The point is not only to detect. It is to give the product a way to pause, step up review, or reject a payment while the decision still matters.

3. Run batch or retrospective logic across patterns

Not every suspicious pattern is visible inside one payment.

Teams also need to detect:

- structuring over multiple transactions

- coordinated activity across related accounts

- unusual merchant return or chargeback patterns

- changes in corridor behavior

- activity that becomes suspicious only when viewed over time

That is especially important for BaaS models, where the real risk often sits at the program or platform level rather than in one isolated payment.

4. Tie monitoring back to onboarding and ownership data

A strong alert should inherit identity context.

For an individual, that may mean KYC profile, sanctions status, expected use case, and prior review history.

For a business, that may mean KYB record, beneficial-owner logic, merchant category, expected transaction behavior, and prior escalations.

Without that connection, alert triage becomes guesswork.

5. Produce an audit-ready case trail

Detection is only the first step.

Teams also need:

- alert reason

- transaction payload

- linked customer or merchant profile

- reviewer notes

- decision history

- escalation path

FinCEN's current MSB SAR guidance still makes the operational point clearly: suspicious activity reporting depends on recognizing suspicious behavior, documenting the facts, and filing on time when thresholds and circumstances require it.

Real-time and batch monitoring are not competitors

Teams often frame this as a choice.

It is the wrong choice.

Real-time monitoring and batch monitoring do different jobs.

Real-time checks help control what should not proceed untouched right now. Batch monitoring helps detect slower patterns, relationship abuse, and rule-evasion behavior that only becomes visible over time.

For payment providers, both matter.

For BaaS teams, both are mandatory if multiple merchants, programs, or end-user populations sit on the same rails.

A realistic failure case: what payment teams actually see

A BaaS platform launches a new program for a digital marketplace.

The first week looks healthy:

- onboarding checks pass

- merchants activate quickly

- payout volume rises

- support tickets stay low

Then the inconsistencies appear.

One merchant account starts sending repeated near-threshold payouts across linked beneficiaries. Another shows a sudden jump in velocity after weeks of low activity. A third begins generating return behavior and corridor patterns that do not match its original profile.

Nothing looks catastrophic in one transaction.

That is the problem.

If monitoring only reviews payments one by one, the pattern looks ordinary. If the review team has no merchant context, the cases look unrelated. If the platform cannot link the alert to onboarding and prior risk decisions, the team cannot explain why the merchant was allowed to scale in the first place.

This is not only a monitoring failure.

It is a workflow failure.

How VOVE ID approaches transaction monitoring for payment teams

VOVE ID is built to treat monitoring as part of the payment infrastructure, not as an isolated after-the-fact queue.

That means teams can structure the workflow around:

- real-time and batch transaction screening

- sanctions and watchlist logic tied to the live payment event

- merchant and customer context carried forward from KYC and KYB

- configurable rules for corridor, velocity, counterparty, and behavior risk

- case routing with evidence attached to the alert

For payment providers, the practical benefit is speed with control.

For BaaS teams, the practical benefit is segmentation. A strong API should let one platform monitor across many programs without flattening them into one noisy rule set.

It should also let cost follow transaction volume instead of forcing teams into a fixed monitoring model before the program shape is even stable.

Practical checklist for payment providers and BaaS teams

Before choosing a transaction monitoring API, ask:

Monitoring

- Ingest full payment context, not only amount and account ID.

- Support both real-time intervention and retrospective pattern detection.

- Tune rules by merchant, corridor, program, and customer risk.

Operations

- Attach alerts to KYC, KYB, sanctions, and prior review data.

- Route cases with evidence already assembled for investigators.

- Track reviewer actions, holds, escalations, and final outcomes in one place.

Governance

- Define which payment events trigger immediate review versus later analysis.

- Keep a clear audit trail for suspicious-activity decisions and filings.

- Review false positives, alert conversion, and investigation time continuously.

If those controls are weak, the problem is not only the rule set.

The operating model is too fragmented.

Conclusion

Transaction monitoring is not a dashboard that teams open after something goes wrong.

It is a live control system for payment behavior, merchant risk, and suspicious-activity escalation.

Payment providers and BaaS teams need monitoring that understands the payment itself, the relationship behind it, and the operational action that follows. Real-time checks, batch pattern detection, and case handling are one workflow.

That is what turns monitoring from a compliance obligation into usable infrastructure.

Need to turn transaction monitoring into a live control layer for payments and BaaS programs? Talk to the team.

FAQ

1. How does a transaction monitoring API differ from fraud rules?

Fraud rules usually focus on stopping unauthorized or abusive activity quickly. Transaction monitoring focuses on AML risk, suspicious patterns, escalation, and evidence quality across the full payment lifecycle.

2. Do payment providers need both real-time and batch monitoring?

Yes. Real-time checks help control immediate risk. Batch monitoring catches slower patterns such as structuring, behavior drift, and related-account activity.

3. What should an alert include for investigators?

At minimum, it should include the transaction facts, the customer or merchant context, the rule or signal that triggered the case, prior history, and the actions already taken.

4. Why is monitoring especially important for BaaS teams?

BaaS teams often carry risk across many programs, merchants, and end-user populations at once. Weak monitoring at the platform layer creates blind spots that do not stay contained to one client.