Onboarding Retail Investors Across 10 EU Countries: One KYC Flow, Many Rules

One KYC flow can serve 10 EU markets — but only if it supports local overlays for suitability, disclosure, and source of funds. Here's where single-stack logic breaks.

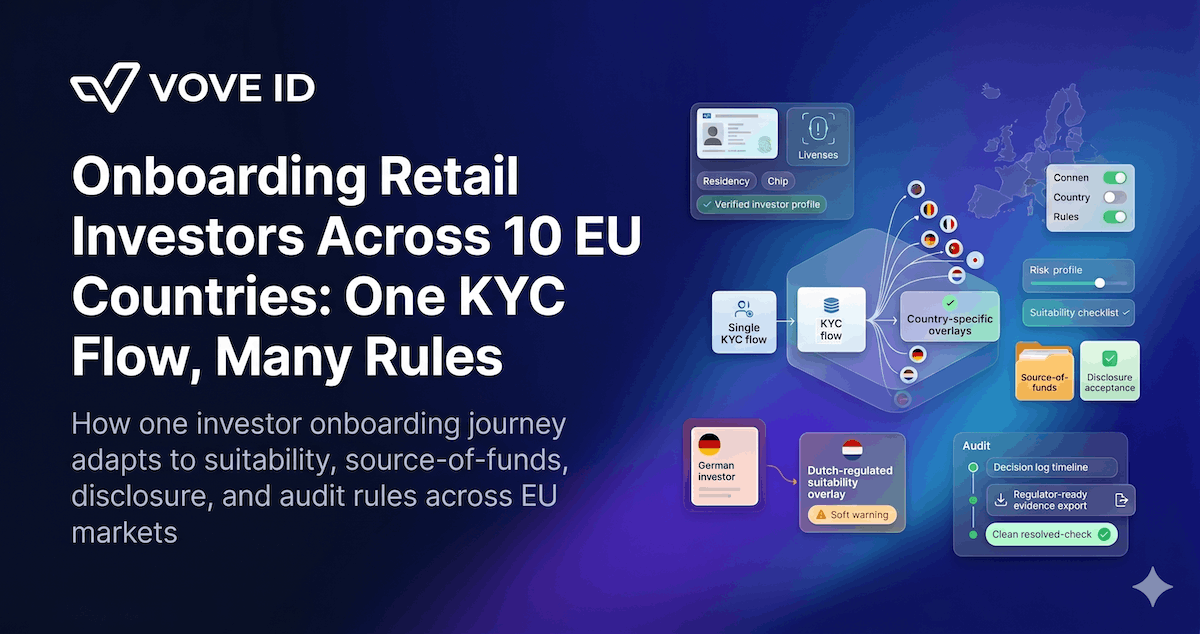

VOVE ID helps retail investment platforms onboard across the EU in markets where one country adds source-of-funds requirements and the next adds a suitability test. On paper, one stack scales. In practice, it has to bend.

This guide covers how to structure a scalable EU investor onboarding flow. For the underlying identity verification framework, see our KYC Requirements Explained 2026.

Direct answer

Retail investor onboarding across 10 EU countries can run through one KYC flow — but only if that flow supports local overlays for identity, suitability, source of funds, disclosures, and audit evidence. The mistake is treating EU-wide expansion as one static checklist instead of one core journey with country-specific steps that appear only when required.

Why retail investor KYC differs by EU country

EU rules create a common floor, but retail investment onboarding is still interpreted through national regulators, local product wrappers, and the platform's operating entity.

A retail investor might need the same identity check in every country, but the surrounding obligations can shift quickly:

- suitability or appropriateness checks for certain investment products

- source-of-funds collection at different thresholds

- country-specific disclosure language

- local complaint handling expectations

- different audit evidence for the same onboarding decision

That is where a hard-coded single flow starts to break. It either under-checks users in stricter markets or over-checks everyone else.

The four countries that move the floor

For many EU investment platforms, Germany, France, the Netherlands, and Spain tend to move the practical floor — not because the rest of the EU is simple, but because these markets expose the gap between legal alignment and operational reality.

Germany may ask whether the onboarding file supports the product's risk profile. France may scrutinize disclosure and suitability evidence. The Netherlands may focus on the logic behind the investor decision. Spain may require documentation the platform can retrieve and explain on short notice.

The same user journey has to produce evidence that each regulator can read.

When a German user trips a Dutch rule

Consider a fractional investment platform that operates through a Dutch entity and starts onboarding German retail users.

The product team assumes the German user only needs the German identity path. But because the platform uses the Dutch entity, the Dutch suitability step fires. The investor is rejected after answering questions that don't match the expectation set in the German onboarding copy.

The user complains. BaFin asks what happened. The platform now has to explain why a German retail investor failed a Dutch suitability decision inside a journey that never made that rule visible.

The problem isn't that one country was stricter. The problem is that the stack couldn't show why the extra step appeared.

How VOVE ID bends one flow to ten countries

VOVE ID keeps the investor journey as one flow, then adds jurisdiction-specific overlays at the points where the regulator actually cares.

The core sequence stays stable:

- Identify the investor

- Verify document and liveness

- Screen for sanctions, PEP status, and adverse media

- Collect suitability or source-of-funds evidence when required

- Store the decision and audit trail

Country, product type, operating entity, and investor risk profile decide which overlays appear.

If a German user enters through a Dutch-regulated product, the platform can show exactly why the Dutch suitability module ran. If a French user accesses a higher-risk product, the disclosure and evidence capture adjusts without routing that user into a separate stack.

For a full breakdown of AML screening requirements — including sanctions, PEP, and adverse media — see our AML Requirements Explained 2026.

What one scalable EU investor onboarding flow needs

A practical EU-wide flow needs more than document verification. It needs decision logic that regulators can inspect after the fact.

The minimum stack should include:

- country detection based on residency, document, and product entity

- identity verification with document and liveness checks

- sanctions, PEP, and adverse media screening

- suitability or appropriateness checks where the product requires them

- source-of-funds triggers for higher-risk or higher-value users

- localized disclosure capture

- a single audit trail per investor decision

The audit trail matters because expansion risk rarely appears on day one. It shows up months later when a regulator asks why a specific investor was accepted, rejected, or moved into enhanced review.

Checklist: Identity, suitability, source of funds

Use this checklist before expanding a retail investment platform across EU markets:

- Identity: Can the platform verify the investor with documents and liveness in every target country?

- Jurisdiction: Can the stack determine which regulator, entity, and product rules apply?

- Suitability: Can the platform show how the investor's knowledge, experience, and risk profile were assessed?

- Source of funds: Are SoF requests triggered by the right thresholds and risk signals?

- Disclosure: Are required disclosures captured in the right language and at the right moment?

- Audit: Can the team reconstruct the decision without searching across multiple tools?

- Review: Are exceptions routed to a reviewer before the investor can proceed?

Q&A

Can one KYC flow serve 10 EU countries?

Yes, if it is one configurable journey with local overlays — not one identical checklist for every user. The core identity flow stays consistent while country-specific suitability, disclosure, and source-of-funds steps appear only when required.

Why do investment platforms need more than identity checks?

Retail investment onboarding often includes suitability, appropriateness, source-of-funds, and disclosure obligations. Identity proves who the investor is. The rest proves whether the platform made a defensible onboarding decision.

What breaks when each country gets its own onboarding stack?

Separate stacks create inconsistent UX, duplicated compliance logic, and fragmented audit evidence. When the business expands, teams struggle to explain why two similar investors were treated differently.

How does VOVE ID help?

VOVE ID lets platforms keep one investor onboarding journey while applying jurisdiction-specific steps based on country, product, entity, and risk. The result is a cleaner user experience and an audit trail that holds up.

Conclusion

EU retail investor onboarding doesn't scale by copying one checklist into 10 markets. It scales when the platform keeps one core flow and lets local requirements appear at the right gate.

That is the difference between a stack that merely verifies users and a stack that can explain its decisions after launch.

Running retail investment onboarding across the EU and need a flow that can explain itself to regulators?

This article is for informational purposes only and does not constitute legal or regulatory advice. Compliance requirements vary by jurisdiction, product type, and operating entity. Consult qualified legal counsel for guidance specific to your situation.