KYC

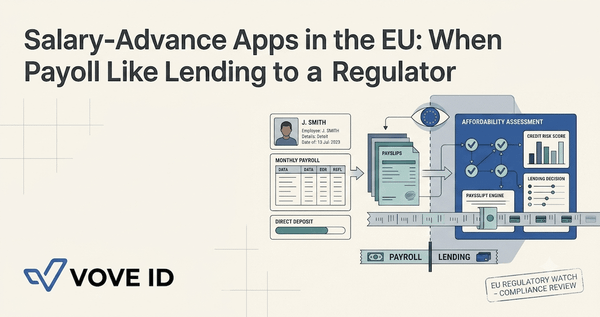

Salary-Advance Apps in the EU: When Payroll Looks Like Lending to a Regulator

Why earned-wage access products can't rely on the payroll label alone, and what affordability, disclosure, and audit trails CCD2 actually requires.

KYC

Why earned-wage access products can't rely on the payroll label alone, and what affordability, disclosure, and audit trails CCD2 actually requires.

AML

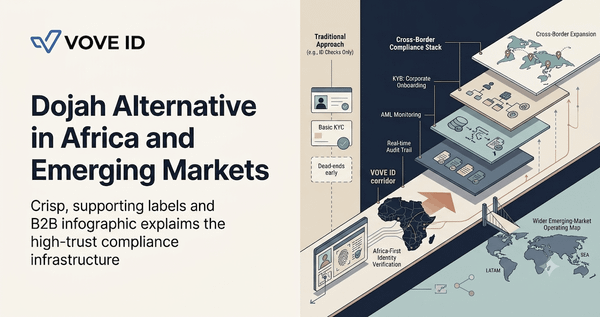

A practical comparison for teams asking whether Dojah still fits once onboarding grows into KYB, monitoring, and regulator-facing evidence.

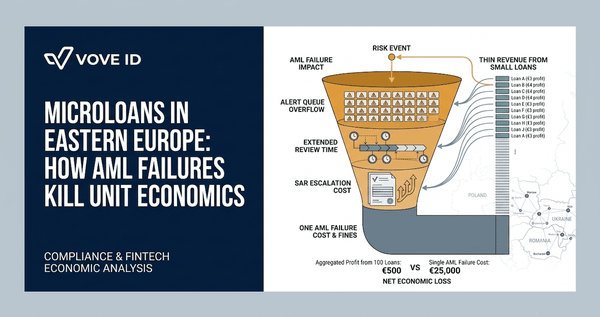

AML

Why a single manual AML review can cost more than a microloan's entire margin, and how Eastern European lenders fix tiering, escalation, and case handoffs.

KYC

The checkout can stay lightweight after CCD2. The affordability and disclosure evidence behind it cannot.

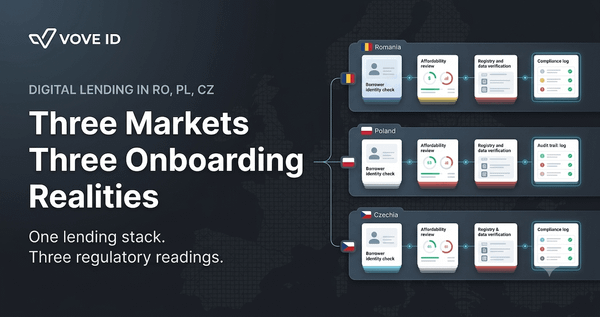

KYC

BNR, KNF, and CNB ask the same questions about a borrower in a different order, with different proof.

AML

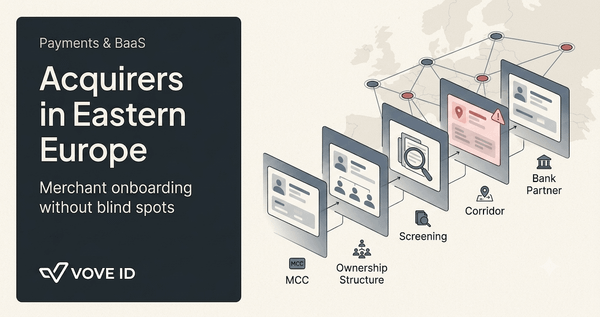

A clean registry extract and a plausible MCC code are the start of merchant risk review, not the end of it.

AML

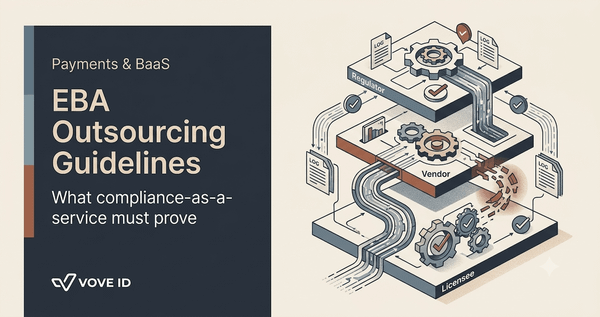

Outsourcing compliance work is allowed under EBA rules. Losing the ability to inspect and govern it is not.

AML

Adding USD or GBP to a EUR account isn't just an FX feature. It's a new corridor your bank partner will start watching.

AML

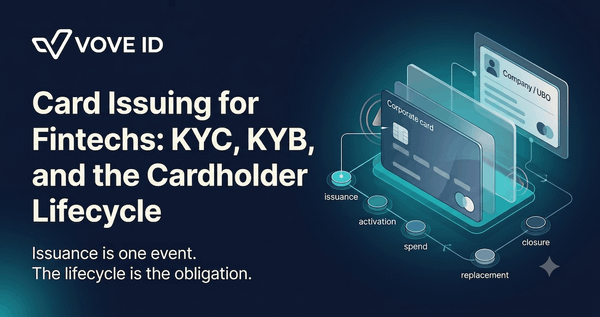

A card is issued once. The compliance obligation behind it does not end there — it follows the cardholder for years.

AML

Open banking firms can no longer treat AML as someone else's problem. If your AISP sees suspicious behavior or your PISP triggers payments, you need CDD, monitoring, and escalation paths.

Compliance

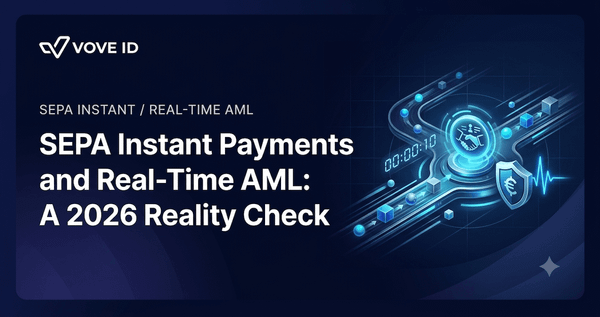

When a SEPA Instant payment settles in 10 seconds, AML controls that used to sit in review queues have to move before release. Here's what that control sequence needs to contain.

AML

A payment institution can passport into a new EU market in weeks and still fail in practice. The license travels. The disclosures and monitoring thresholds don't, unless you designed them to.